Off-spec Oil Can Affect Global Prices

- Region-wide problems can influence global crude oil prices

- Contamination of Russian oil creates supply concerns

- Iranian sanctions re-imposed

- 2019 hurricane season likely to be quiet after three active years

The Matrix

Commentary on the situation in global oil markets tends to focus on broad overarching themes. What could be more interesting than a larger-than-expected shut down in refinery use? Or the emerging relationship between OPEC and non-OPEC oil producers like Russia? Or the continuing record highs in North American production and the resulting expansion of a U.S. crude oil export trade? These things matter deeply for the expected economic health of the international energy community.

Underlying these major considerations, however, are a plethora of other factors that can influence price and availability. One such factor is the quality of crude oil for sale. Observers generally assume that oil in commerce is up to specification.

A recent departure from that assumption has been reported. Belarus’ state pipeline company notified offtakers that Russian crude oil in the 3,400 mile Druzhba pipeline was “heavily contaminated.” Following this notice,” refiners and oil firms in Europe cut purchases of Russian oil by up to a million barrels a day – or 10 percent of European oil imports – in a major disruption to supply from the world’s second largest oil exporter.

Prices shot up. Brent climbed over $75. Confidence in Russian exports fell. Contamination is a factor in pricing oils. Other examples have occurred in the United States, Germany and Ukraine among others. Russia is seeking to determine if sabotage had been involved.

Oil demand has been strong globally and uncertainty about the quality of supply will appear in markets in the form of higher prices. This will only exacerbate concerns about supply availability.

Tighter sanctions on Iran add to market concerns. No waivers have yet been granted unlike the situation when sanctions were first imposed. Price forecasts have reflected a “no waiver” situation. Projections for WTI crude oil have been raised to $61.50 for 2019 by some financial houses. Last month, projections stood at $61.

Propane stocks are becoming abundant. Higher output of oil and natural gas has translated into higher inventories. Gulf Coast stocks are almost twice as “high as last year.” One analysis estimates that propane supplies could hit 100 million barrels by mid-October.

Supply/Demand Balances

Supply/demand data in the United States for the week ending April 26, 2019 were released by the Energy Information Administration.

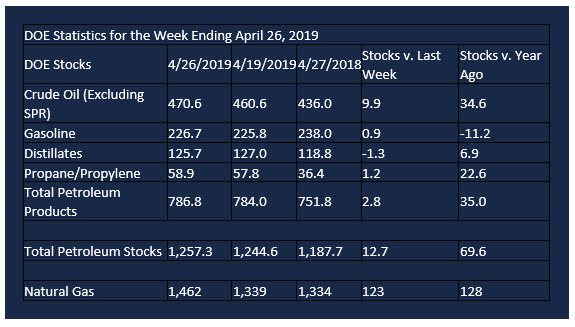

Total commercial stocks of petroleum increased 12.7 million barrels during the week ending April 26, 2019.

There were draws in stocks of fuel ethanol, K-jet fuel, distillates, and residual fuel.

There were builds in stock of gasoline, propane, and other oils.

Commercial crude oil supplies in the United States increased 9.9 million barrels from the previous report week to 470.6 million barrels.

Crude oil supplies increased in three of the five PAD Districts. PADD 2 (Midwest) crude oil stocks rose 0.4 million barrels, PADD 3 (Gulf Coast) stocks increased 9.2 million barrels, and PADD 5 (West Coast) stocks advanced 1.2 million barrels. PADD 1 (East Coast) stocks fell 0.6 million barrels and PADD 4 (Rockies) stocks declined 0.2 million barrels.

Cushing, Oklahoma inventories increased 0.3 million barrels from the previous report week to 45.2 million barrels.

Domestic crude oil production rose 100,000 barrels be day from the previous report week to 12.3 million barrels daily.

Crude oil imports averaged 7.414 million barrels per day, a daily increase of 265,000 barrels. Exports decreased 70,000 barrels daily to 2.611 million barrels per day.

Refineries used 89.2 per cent of capacity, a decrease of 0.9 percentage points from the previous report week.

Crude oil inputs to refineries decreased 137,000 barrels daily; there were 16.446 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 169,000 barrels daily to 16.741 million barrels daily.

Total petroleum product inventories rose 2.8 million barrels from the previous report week.

Gasoline stocks increased 0.9 million barrels daily from the previous report week; total stocks are 226.7 million barrels.

Demand for gasoline decreased 181,000 barrels per day to 9.228 million barrels per day.

Total product demand decreased 296,000 barrels daily to 20.152 million barrels per day.

Distillate fuel oil stocks decreased 1.3 barrels from the previous report week; distillate stocks are at 125.7 million barrels. National distillate demand was reported at 4.215 million barrels per day during the report week. This was a weekly increase of 419,000 barrels daily.

Propane stocks increased 1.2 million barrels from the previous report week; propane stock are 58.9 million barrels. Current demand is estimated at 673,000 barrels per day, a decrease of 39,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Net injections into storage totaled 123 Bcf for the week ending April 26, compared with the five-year (2014–18) average net injections of 70 Bcf and last year’s net injections of 50 Bcf during the same week. Working gas stocks totaled 1,462 Bcf, which is 316 Bcf lower than the five-year average and 128 Bcf more than last year at this time.

The 2019 hurricane season is right around the corner. (The season will officially begin on June 1, 2019, and end on November 30, 2019.) Early expectations are for the quietest season in four years, “despite a forecasted near normal year with respect to total storm number, hurricanes and major hurricanes.” One analyst suggests a “lower-than-normal risk for Gulf of Mexico landfalls.” Higher risks exist for the U.S. East Coast. 2018 was the third consecutive active year with two impactful land-falling storms in the U.S. (Florence and Michael.)

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.