Global Supply of Crude Oil Set to Expand

- OPEC+ supply cut agreement ended Aug. 1, 2020

- U.S. SPR space rented for private company storage

- U.S. crude oil production picking up

- Natural gas stocks could reach 4.2 Bcf as withdrawal season begins

The Matrix

The beginning of August appears to be the start of a new phase in petroleum supply and demand. It marks the end of OPEC+ formal supply restraint. Crude oil supply could be expected to grow without a new agreement.

OPEC members increased production by more than one million barrels daily in July in anticipation of the agreement’s conclusion. The group’s output reached 23.3 million barrels per day, not much above the 1991 low reported by OPEC.

Crude oil availability has grown, apart from OPEC’s efforts. The U.S. Strategic Petroleum Reserve has been renting space to private companies for which other storage options were becoming tight. Moreover, the U.S. will provide space in the SPR for 1.5 million barrels of crude oil owned by Australia. A similar arrangement is in the works for India.

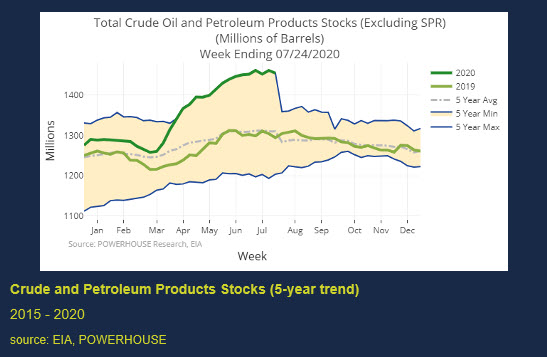

Since April, stocks in the Gulf Coast underground caverns have grown 21.2 million barrels. SPR inventories reached 656.1 million barrels as of July 24, 2020, reported in EIA’s weekly U.S. Petroleum Balance Sheet. The SPR has room for another 56 million barrels not including the Australian supply. (Data from the SPR is reported separately from “Commercial” inventories.)

The United States itself is experiencing renewed growth in production. Fracking has started to re-open as reported in data on working oil wells. The number of wells operating in the Permian was 15 to 20 in May and June. Most recently, 40 to 45 wells are now running.

Lower crude oil prices have not followed these increases. They have traded in a remarkably tight range centered around $40 per barrel for WTI crude oil futures since mid-June. WTI’s lowest close was $38.38 on June 16; the highest close since then was $41.07, seen on July 23.

Growth in overseas crude oil supply and in the SPR comes while domestic economic news turns grim. The economy showed the steepest drop ever recorded in Gross Domestic Product. GDP fell 32.9% (seasonally adjusted and annualized) during the second quarter. This, of course, reflects the pandemic with its shelter-in-place orders. It’s hard to explain why such bearish data has not resulted in a bearish crude oil price reaction. A break of $38.38 support opens the way to $34.25.

Supply/Demand Balances

Supply/demand data in the United States for the week ended July 24, 2020, were released by the Energy Information Administration.

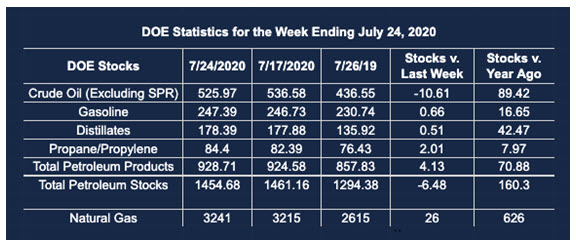

Total commercial stocks of petroleum fell by 6.5 million barrels during the week ended July 24, 2020.

Commercial crude oil supplies in the United States decreased by 10.6 million barrels from the previous report week to 526.0 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 0.5 million barrels to 12.7 million barrels

PADD 2: Plus 2.2 million barrels to 139.7 million barrels

PADD 3: Down 10.5 million barrels to 295.5 million barrels

PADD 4: Down 0.1 million barrels to 25.3 million barrels

PADD 5: Down 1.7 million barrels to 52.8 million barrels

Cushing, Oklahoma inventories were up 1.3 million barrels from the previous report week to 50.1 million barrels.

Domestic crude oil production was unchanged from the previous report week at 11.1 million barrels daily.

Crude oil imports averaged 5.146 million barrels per day, a daily decrease of 794,000 barrels. Exports rose 218,000 barrels daily to 3.211 million barrels per day.

Commercial crude oil supplies in the United States decreased by 10.6 million barrels from the previous report week to 526.0 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 0.5 million barrels to 12.7 million barrels

PADD 2: Plus 2.2 million barrels to 139.7 million barrels

PADD 3: Down 10.5 million barrels to 295.5 million barrels

PADD 4: Down 0.1 million barrels to 25.3 million barrels

PADD 5: Down 1.7 million barrels to 52.8 million barrels

Cushing, Oklahoma inventories were up 1.3 million barrels from the previous report week to 50.1 million barrels.

Domestic crude oil production was unchanged from the previous report week at 11.1 million barrels daily.

Crude oil imports averaged 5.146 million barrels per day, a daily decrease of 794,000 barrels. Exports rose 218,000 barrels daily to 3.211 million barrels per day.

Total petroleum product inventories rose 4.1 million barrels from the previous report week.

Gasoline stocks increased 0.7 million barrels daily from the previous report week; total stocks are 247.4 million barrels.

Demand for gasoline rose 259,000 barrels per day to 8.809 million barrels per day.

Total product demand increased 1.440 million barrels daily to 19.094 million barrels per day.

Distillate fuel oil stocks increased 0.5 million barrels from the previous report week; distillate stocks are at 178.4 million barrels. EIA reported national distillate demand at 3.635 million barrels per day during the report week, a increase of 412,000 barrels daily.

Propane stocks increased 2.0 million barrels from the previous report week; propane stocks are 84.4 million barrels. The report estimated current demand at 1.429 million barrels per day, an increase of 428,000 barrels daily from the previous report week.

Natural Gas

Natural gas futures prices rose nearly 17% on the first day of trading in August. A market that had been trading in a tight range since early May broke to the upside despite a raft of bearish expectations.

EIA suggested end-of-injection period storage could reach a record 4.2 Bcf next October (see below). Analysts called for Henry Hub prices to drop to $1.99 for 2020. This would be a 25-year low, reflecting high production and storage taking the edge off supply concerns.

Exports of LNG are expected to rise in August, the first increase in six months. Continued heat through August is another potentially bullish price feature.

Overlooked in these stories is the fact that August is typically when natural prices tend to bottom seasonally. This may be the most important reason natural gas performed so strongly as August trading opened. Traders should be careful; the daily high of $2.154, as bullish as it was, did not exceed the longer-term high of $2.162. This was seen on May 5.

According to the EIA:

The net injections into [natural gas] storage totaled 26 Bcf for the week ending July 24, compared with the five-year (2015–19) average net injections of 33 Bcf and last year’s net injections of 56 Bcf during the same week. Working natural gas stocks totaled 3,241 Bcf, which is 429 Bcf more than the five-year average and 626 Bcf more than last year at this time.

The average rate of injections into storage is 11% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 9.2 Bcf/d for the remainder of the refill season, the total inventory would be 4,152 Bcf on October 31, which is 429 Bcf higher than the five-year average of 3,723 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright © 2020 Powerhouse, All rights reserved.