Oil Prices Weaken

- Equity markets lose ground

- Oil supply recovering in Libya, Nigeria

- Governments mandate production cuts to support price

- Natural gas stocks fall 6.3 Bcf

The Matrix

Oil markets have been tracking bearishly since early October, when WTI crude oil futures topped around $77. Prices have since eased back, but continuing strength in the economy contributed to the prospect of higher oil prices. Equity markets appear to have a different view of the economic outlook. Three days during the week ending December 7, 2018 saw the S&P index fall sharply. Even the recovery that followed may not have been enough to alter the growing belief that a weaker market lies ahead in 2019.

Crude oil supply has advanced steadily in 2018. Production in the United States reached 11.7 million barrels daily about a month ago and has held that level. EIA expects output to exceed 12 million barrels per day early in 2019.

Perhaps more significant, however, is the generally unexpected recovery in supply by producers like Libya and Nigeria. The Saudis, Russia and the United States are contesting for recognition as the lead global oil producer. The U.S. does not face constraints from government and the large number of industry participants.

Concerns for oversupply came from an unexpected place. The Canadian province of Alberta has imposed a production cut of 325,000 barrels per day. This cut takes effect in January, 2019. It is set to run for the first three months of the year, with monthly reviews thereafter. Alberta faces the problem of inadequate takeaway capability. These cuts are an attempt to balance stocks as added rail capacity becomes available.

Another cut in supply could come from a 1.2-million-barrel daily production reduction announced by OPEC and Russian-led oil producers. This reduction will remain in effect for six months. If history is any guide, Saudi Arabia will bear the bulk of the cuts. Pressure from the United States to encourage lower prices could limit the effect of the agreement.

Supply/Demand Balances

Supply/demand data in the United States for the week ending November 30, 2018 were released by the Energy Information Administration.

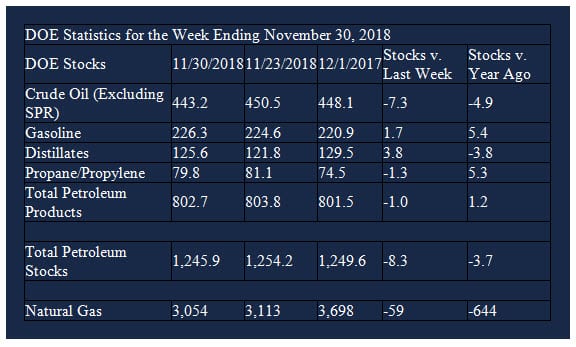

Total commercial stocks of petroleum decreased 8.3 million barrels during the week ending November 30, 2018.

There were builds in stocks of gasoline, fuel ethanol, and distillates. There weres draws in stocks of K-jet fuel, propane, and other oils. Stocks of residual fuel were unchanged from the previous report week.

Commercial crude oil supplies in the United States decreased to 443.2 million barrels, a draw of 7.3 million barrels.

Crude oil supplies decreased in two of the five PAD Districts. PADD 1 (East Coast) crude oil stocks declined 0.4 million barrels and PADD 3 (Gulf Coast) stocks fell 9.1 million barrels. PAD District 2 (Midwest) stocks rose 1.2 million barrels, PADD 4 (Rockies) stocks increased 0.5 million barrels, and PADD 5 (West Coast) were up 0.6 million barrels.

Cushing, Oklahoma inventories increased 1.8 million barrels from the previous report week to 38.3 million barrels.

Domestic crude oil production was unchanged from the previous report week at 11.7 million barrels per day.

Crude oil imports averaged 7.219 million barrels per day, a daily decrease of 943,000 barrels per day. Exports rose 761,000 barrels daily to 3.203 million barrels per day.

Refineries used 95.5 per cent of capacity, a decrease of 0.1 percentage points from the previous report week.

Crude oil inputs to refineries decreased 66,000 barrels daily; there were 17.487 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, decreased 19,000 barrels daily to 17.770 million barrels daily.

Total petroleum product inventories fell 1.0 million barrels from the previous report week.

Gasoline stocks increased 1.7 million barrels from the previous report week; total stocks are 226.3 million barrels.

Demand for gasoline decreased 311,000 barrels per day to 8.877 million barrels per day.

Total product demand increased 45,000 barrels daily to 20.530 million barrels per day.

Distillate fuel oil stocks increased 3.8 million barrels from the previous report week; distillate stocks are 125.6 million barrels. National distillate demand was reported at 4.037 million barrels per day during the report week. This was a weekly increase of 467,000 barrels daily.

Propane stocks decreased 1.3 million barrels from the previous report week; propane stock are 79.8 million barrels. Current demand is estimated at 1.321 million barrels per day, an increase of 152,000 barrels daily from the previous report week.

Natural Gas

According to the EIA:

Working gas in storage was 2,991 Bcf as of Friday, November 30, 2018, according to EIA estimates. This represents a net decrease of 63 Bcf from the previous week. Stocks were 704 Bcf less than last year at this time and 725 Bcf below the five-year average of 3,716 Bcf. At 2,991 Bcf, total working gas is below the five-year historical range.

Some analysts see high volatility in natural gas prices for 2019. This reflects expectations for new volumes of natural gas produced in association with shale oil. Falling oil prices could constrain output and induce volatility. Volumes of natural gas associated would take on that volatility too.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2018 Powerhouse, All rights reserved.