A rapidly changing supply and demand environment challenges market participants

- Drastic changes in supply and demand for refined products

- Refiners reacting by significantly changing their output mix

- Natural gas inventories continue to build at a higher than average rate

The Matrix

Since the end of April, the refined products complex has been a tale of two markets. Using the week ended April 24 as a marker, the August RBOB contract has rallied 52.16 cents per gallon or 68.49% as of Friday’s close on July 10. The August HO contract has rallied 37.63 cents per gallon or a 43.50% increase over the same time period.

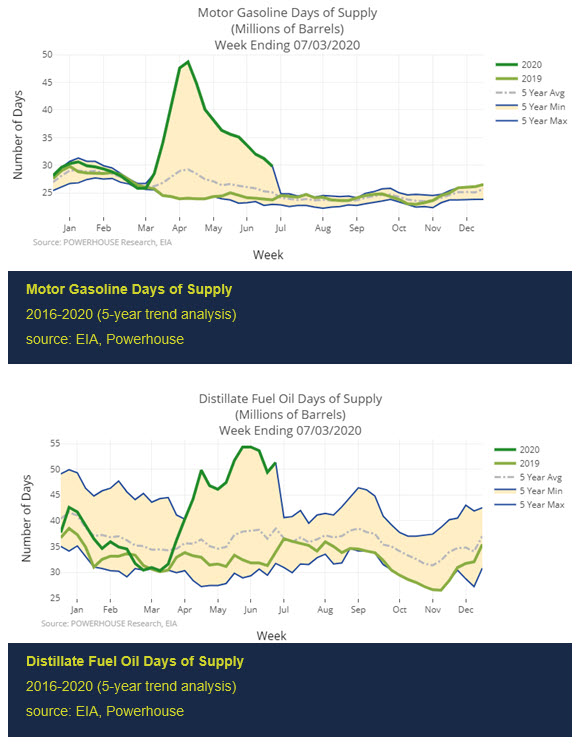

Gasoline’s price strength has been a driven in large part by improving fundamentals. Gasoline days of supply (inventory/demand) reached a high of 48.7 days for the week ended April 24. Last week it stood at 29.8 days of supply.

Distillate fuel (excluding jet fuel) by comparison hit a high of 54.3 days of supply for the week ended June 5, and last week stood at 51.3 days of supply. Please see the attached graphs below that are updated weekly on the POWERHOUSE website.

At the onset of the widespread economic shutdowns, refiners reduced gasoline and jet fuel output as much as possible. This led to an increase in distillate fuel production. Despite anecdotal evidence of strong demand from the trucking sector, the oversupply of distillate fuel remains.

Refiners have continued to adapt to changing circumstances. As states re-opened and retail gasoline demand picked back up, they once again adjusted their output ratios. In the last week of April refiners made 6.735 million barrels of gasoline per day and 4.982 million barrels of distillate. As of last week, those output totals stood at 9.045 million barrels of gasoline and 4.756 million barrels of distillate.

One big question facing market participants is whether the refiners’ shift back to gasoline production will enable distillate days of supply to decline and follow the path set earlier by gasoline. If this dynamic kicks in—and is not interrupted by widespread economic re-closings—this could offer bullish boost to distillate prices. However, this remains a very large “if” at present.

Supply/Demand Balances

Supply/demand data in the United States for the week ended July 3, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose by 9.8 million barrels during the week ended July 3, 2020.

Commercial crude oil supplies in the United States increased by 5.7 million barrels from the previous report week to 539.2 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 0.4 million barrels from previous report week to 12.1 million barrels

PADD 2: Down 0.5 million barrels to 136.3 million barrels

PADD 3: Plus 5.0 million barrels to 309.0 million barrels

PADD 4: UNCH from the previous report week at 25.6 million barrels

PADD 5: Plus 2.4 million barrels to 56.2 million barrels

Cushing, Oklahoma inventories were up 2.2 million barrels from the previous report week to 47.8 million barrels.

Domestic crude oil production was unchanged from the previous report week at 11.0 million barrels daily.

Crude oil imports averaged 7.394 million barrels per day, a daily increase of 1.425 million barrels. Exports fell 705,000 barrels daily to 2.387 million barrels per day.

Refineries used 77.5% of capacity, plus 2.0% from the previous report week.

Crude oil inputs to refineries increased 314,000 barrels daily; there were 14.347 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 378,000 barrels daily to reach 14.698 million barrels daily.

Total petroleum product inventories fell 4.1 million barrels from the previous report week.

Gasoline stocks decreased 4.8 million barrels daily from the previous report week; total stocks are 251.7 million barrels.

Demand for gasoline rose 205,000 barrels per day to 8.766 million barrels per day.

Total product demand increased 766,000 barrels daily to 18.120 million barrels per day.

Distillate fuel oil stocks increased 3.1 million barrels from the previous report week; distillate stocks are at 177.3 million barrels. EIA reported national distillate demand at 3.019 million barrels per day during the report week, a decrease of 758,000 barrels daily.

Propane stocks increased 2.2 million barrels from the previous report week; propane stocks are 76.8 million barrels. The report estimated current demand at 647,000 barrels per day, a decrease of 48,000 barrels daily from the previous report week.

Natural Gas

Stocks for the beginning-of-withdrawal season for natural gas (Nov. 1, 2020) are shaping up to be much higher than the average of the past five years. (See below.) Nearby futures prices reached $1.89 on July 7, the top of the extended range in which natural gas has been trading and started another move lower. Support continues at $1.43.

According to EIA:

The net injections [of natural gas] into storage totaled 56 Bcf for the week ending July 3, compared with the five-year (2015–19) average net injections of 68 Bcf and last year’s net injections of 83 Bcf during the same week. Working natural gas stocks totaled 3,133 Bcf, which is 454 Bcf more than the five-year average and 685 Bcf more than last year at this time.

The average rate of injections into storage is 15% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 8.7 Bcf/d for the remainder of the refill season, the total inventory would be 4,177 Bcf on October 31, which is 454 Bcf higher than the five-year average of 3,723 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright © 2020 Powerhouse, All rights reserved.