Oil markets are falling today, following the stock market. Yesterday, the stock market posted its heftiest loss since June, with ebullient tech stocks finally handing back some gains. The Dow Jones Industrial Average dropped 2.78%, the S&P 500 fell 3.51%, and the Nasdaq fell 4.96%. Crude oil futures dropped sharply, threatening to fall below $40 a barrel. Today, there are indications that stocks will have a mixed day, and that the overall rout will stabilize. Some of the tech stocks had posted such astounding gains that a downward correction may have been expected, especially with pre-Labor Day profit-taking. The just-released August jobs report was very encouraging, however. The unemployment rate fell to 8.4%, beating expectations. Oil prices are stabilizing, and West Texas Intermediate (WTI) crude oil futures appear to be maintaining their hold in the vicinity of $40.50 to $41.00 a barrel. Crude and product prices appear to be heading for a finish in the red this week.

Initial weekly unemployment claims at last dropped decisively below the one-million mark, coming in at 881,000 during the week ended August 29. Claims dropped by 130,000 from last week’s upward-revised level of 1,011,000 during the week ended August 22. According to data collected by the Department of Labor, during the week of March 28, initial jobless claims hit a peak of 6,867,000. From that peak, initial jobless claims fell for 15 weeks. July brought a setback, and claims rose again. Three weeks ago, claims finally fell below one million, but they were not able to sustain the downward trend. During the 24 weeks since U.S. states began to issue shelter-in-place orders, 59.3 million Americans have filed initial jobless claims.

The Bureau of Labor Statistics (BLS) released the more definitive jobs report for August this morning, and it also held good news for the economy: The unemployment rate finally fell below 10%, as economists had predicted. At 8.4%, it fell even further than expected. According to the BLS: “These improvements in the labor market reflect the continued resumption of economic activity that had been curtailed due to the coronavirus (COVID-19) pandemic and efforts to contain it. In August, an increase in government employment largely reflected temporary hiring for the 2020 Census. Notable job gains also occurred in retail trade, in professional and business services, in leisure and hospitality, and in education and health services.”

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have reached 26,344,473, with 869,569 deaths. Confirmed cases in the U.S. have risen to 6,151,391. U.S. deaths attributed to the disease have reached 186,806.

WTI crude futures prices opened at $41.25 a barrel today, down by $1.75 a barrel (4.0%) from last Friday’s open of $42.98 a barrel. Last week, Hurricane Laura stimulated buying interest, and prices surged. Prices had been easing already, but the collapse of the stock market yesterday dragged oil prices down more sharply. Today, prices are weak, and WTI futures prices are hovering around $41 a barrel. Prices appear to be heading for a finish in the red. Our weekly price review covers hourly forward prices from Friday, August 28 through Friday, September 4. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

Source: Prices as reported by DTN Instant Market

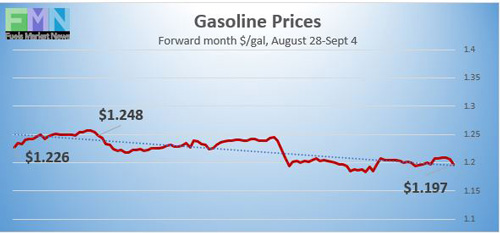

Gasoline Prices

Gasoline futures prices opened at $1.2049 a gallon today on the NYMEX, compared with $1.21 a gallon on Friday, August 28. This was a decline of 0.51 cents (0.4%). March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April and May. U.S. average retail prices for gasoline rose 4.0 cents to average $2.222/gallon during the week ended August 31. Retail prices reclaimed the territory above $2 per gallon during the first week of June. Last week, gasoline futures prices spiked midweek in response to the impending hurricane and a significant draw from inventories, hitting highs of $1.434 a gallon. But prices retreated thereafter. A holiday weekend such as Labor Day often strengthens gasoline prices, but today’s trading is not showing this. Gasoline futures are trading in the range of $1.18/gallon to $1.21/gallon. The week appears to be heading for a finish in the red. The latest price is $1.1835/gallon.

Source: Prices as reported by DTN Instant Market

Diesel Prices

Diesel opened on the NYMEX today at $1.1644/gallon, down significantly by 6.52 cents, or 5.3%, from last Friday’s open of $1.2296/gallon. U.S. average retail prices for diesel rose by 1.5 cents per gallon during the week ended August 31 to average $2.441/gallon. Diesel prices generally have weakened this year, missing some of the price recovery seen in crude and gasoline markets. Diesel futures prices spiked midweek in advance of Hurricane Laura, reaching highs of $1.27 a gallon, but prices retreated thereafter. Prices dropped sharply yesterday and today after the stock market drop. The week appears to be heading for a finish in the red. Currently, diesel is trading mainly in the range of $1.15-$1.185/gallon. The latest price is $1.1668/gallon.

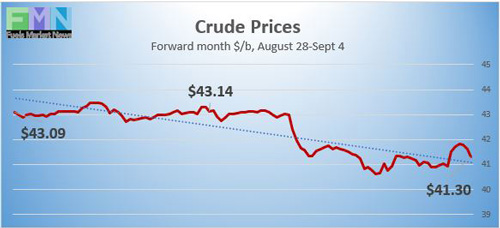

WTI Crude Prices

Source: Prices as reported by DTN Instant Market

WTI crude forward prices opened on the NYMEX today at $41.25 a barrel, compared with $42.98 a barrel last Friday. This was a loss of $1.73 a barrel (4.0%.) Last week, prices strengthened in the lead up to Hurricane Laura. The storm caused massive damage but less than was feared. Prices began to ease. This week, however, the stock market lost its luster, and oil prices are heading down. Until this week, WTI crude futures prices had risen for four weeks, capturing the territory above $41 a barrel and even rising above $43 a barrel, which had not happened for five months. Prices are now retreating, and WTI futures prices are under $41 a barrel. The week appears to be heading for a finish in the red. WTI crude is trading mainly in the $40.60–$41.75 a barrel range currently. The latest price is $40.71 a barrel.

PRICE MOVERS THIS WEEK: BRIEFING

Oil markets are falling today, following the stock market. Yesterday, the stock market posted its heftiest loss since June, with ebullient tech stocks finally handing back some gains. The Dow Jones Industrial Average dropped 2.78%, the S&P 500 fell 3.51%, and the Nasdaq fell 4.96%. Crude oil futures dropped sharply, threatening to fall below $40 a barrel. Today, there are indications that stocks will have a mixed day, and that the overall rout will stabilize. Some of the tech stocks had posted such astounding gains that a downward correction may have been expected, especially with pre-Labor Day profit-taking. The just-released August jobs report was very encouraging. Oil prices are stabilizing, and WTI crude oil futures appear to be maintaining their hold in the vicinity of $41 a barrel. Crude and product prices appear to be heading for a finish in the red this week.

Initial weekly unemployment claims at last dropped decisively below the one-million mark, coming in at 881,000 during the week ended August 29. Claims dropped by 130,000 from last week’s upward-revised level of 1,011,000 during the week ended August 22. According to data collected by the Department of Labor, during the week of March 28, initial jobless claims hit a peak of 6,867,000. From that peak, initial jobless claims fell for 15 weeks. July brought a setback, and claims rose again. Three weeks ago, claims finally fell below one million, but they were not able to sustain the downward trend. During the 24 weeks since U.S. states began to issue shelter-in-place orders, 59.3 million Americans have filed initial jobless claims.

The Bureau of Labor Statistics (BLS) released the more definitive jobs report for August this morning, and it also held good news for the economy: The unemployment rate finally fell below 10%, as economists had predicted. At 8.4%, it fell even further than expected. According to the BLS: “These improvements in the labor market reflect the continued resumption of economic activity that had been curtailed due to the coronavirus (COVID-19) pandemic and efforts to contain it. In August, an increase in government employment largely reflected temporary hiring for the 2020 Census. Notable job gains also occurred in retail trade, in professional and business services, in leisure and hospitality, and in education and health services.”

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have reached 26,344,473, with 869,569 deaths. Confirmed cases in the U.S. have risen to 6,151,391. U.S. deaths attributed to the disease have reached 186,806.

Weekly data on supply, demand and inventory are complicated because of Hurricane Laura. This week’s major drain on crude and product stockpiles ordinarily would have been bullish for prices, but the drawdowns are considered a function of the hurricane, and prices did not rise significantly.

The American Petroleum Institute (API) released information on Tuesday showing a major, across-the-board drawdown from crude oil and gasoline inventories. According to the API, 6.36 mmbbls of crude were drawn from stockpiles, along with 5.761 mmbbls from gasoline stockpiles and 1.424 mmbbls from diesel inventories. The API’s net drain on inventories was a huge 13.545 mmbbls. Market analysts had predicted across-the-board drawdowns from crude and product inventories, but at significantly smaller volumes.

The U.S. Energy Information Administration (EIA) published official inventory data on Wednesday, reporting an even larger drain on inventories. EIA statistics showed drawdowns of 9.362 mmbbls from crude oil inventories, 4.32 mmbbls from gasoline inventories, and 1.675 mmbbls from diesel inventories. The EIA net result was a massive inventory drawdown of 15.357 mmbbls. However, these changes were attributed largely to Hurricane Laura.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks fell to 45,582 mmbbls during the week ended June 26. However, the downward trend was reversed in July through early August, sending Cushing stocks back up to 53,289 mmbbls during the week ended August 7. The current week ended August 21 brought Cushing stocks down to 52,403 mmbbls.

During the week ended August 14, U.S. crude production rose by 0.1 mmbpd to reach an average of 10.8 mmbpd. According to the EIA, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd in April, 11.52 mmbpd in May, and 10.9 mmbpd in June. Production in July rose to an average of 11.04 mmbpd. The decline to 10.7 mmbpd during the first half of August may signal the coming of a more serious decline, which could cause higher prices. The EIA reported that U.S. crude production fell 21.9% between December 2019 and May 2020.