Winter Weather Forecasts

- Old Farmer’s Almanac looks for heavy snows

- Farmer’s Almanac forecasts freeze and frigid

- Weather hedging instruments available for protection (if 1 and 2 are wrong)

- EIA calls for strong propane demand.

The Matrix

This is the time of year when forecasts of winter weather come into fashion. One of the standard sources of long-term winter expectations is the Old Farmer’s Almanac (OFA.) OFA and its immediate competitor, the Farmer’s Almanac (FA,) have each been published for over 200 years. Their forecasts are often treated with the solicitous good humor afforded an elderly uncle. They claim high levels of accuracy (FA says it is 80 per cent accurate; OFA, much the same.) In any case, no winter forecast for the United States would be complete without some recognition of these long-lived contributors.

OFA expects heavy snows to be the main weather feature of the 2019-2020 season. It will have lots of “rain, sleet and plenty of snow.” OFA may be best remembered for featuring the word, “snow-verload.” OFA is predicting no less than seven big snowstorms over the country. OFA expects a long-lasting winter too, hanging on late into March particularly in the Midwest to the Appalachians.

The Farmer’s Almanac is calling for a “freezing, frigid and frosty” season. It’s expecting a “Polar Coaster,” a winter with many ups and downs on the thermometer. FA predicts heavy snows for the Great Plains in January.

Many weather watchers grant the Almanacs about the same level of deference as afforded Punxatawney Phil, Pennsylvania’s premier projector of spring – very little. Nonetheless, the uncertain impact of winter weather raises the question of protecting against the negative effects of weather. A warmer winter, for example, can reduce revenues or have negative impact on the value of inventories.

Weather hedging instruments are available for protection against the adverse financial impact of several weather phenomena. These include temperature, snow, and rain. Powerhouse can tell you more about weather hedging as part of a suite of protective financial instruments.

Speaking of weather, “demand for heating fuels during the 2019 grain drying season may rise higher than the five-year average for the first time since 2013. Although crops are still about two months away from harvest, the combination of expected wet, late corn crops; relatively high grain prices; and relatively low propane prices suggest strong propane demand during this year’s grain drying season,” according to the DOE.

The National Weather Service projects September weather cooler and wetter than normal. This adds to requirements for crop drying.

Supply/Demand Balances

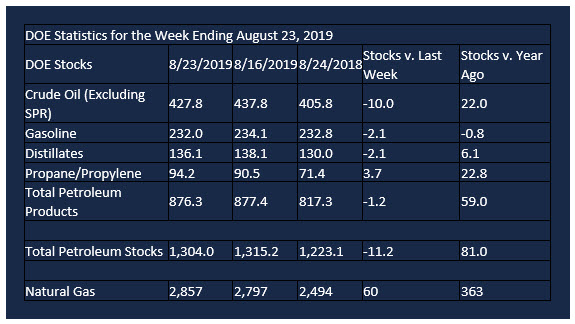

Supply/demand data in the United States for the week ending August 23, 2019, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell by 11.2 million barrels during the week ending August 23, 2019.

There were builds in stocks of K-jet fuel, residual fuel oil, and propane. Stock reductions were seen in gasoline, fuel ethanol, distillate fuels, and other oils.

Commercial crude oil supplies in the United States declined 10.0 million barrels from the previous report week to 427.8 million barrels.

Crude oil supplies decreased in all five PAD Districts. PAD District 1 (East Coast) crude oil stocks declined 1.3 million barrels, PADD 2 (Midwest) crude stocks fell 4.9 million barrels, PAD District 3 (Gulf Coast) crude stocks retreated 1.1 million barrels, PADD 4 (Rockies) stocks decreased 0.1 million barrels, and PADD 5 (West Coast) stocks declined 2.7 million barrels.

Cushing, Oklahoma inventories fell 1.9 million barrels from the previous report week to 40.4 million barrels.

Domestic crude oil production rose 200,000 barrels daily to 12.5 million barrels per day.

Crude oil imports averaged 5.928 million barrels per day, a daily decrease of 1.290 million barrels. Exports rose 216,000 barrels daily to 3.019 million barrels per day.

Refineries used 95.2 percent of capacity, down 0.7% from the previous report week.

Crude oil inputs to refineries decreased 294,000 barrels daily; there were 17.408 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, declined 132,000 barrels daily to reach 17.906 million barrels daily.

Total petroleum product inventories fell 1.2 million barrels from the previous report week.

Gasoline stocks decreased 2.1 million barrels daily from the previous report week; total stocks are 232.0 million barrels.

Demand for gasoline rose 274,000 barrels per day to 9.900 million barrels per day.

Total product demand increased 1.222 million barrels daily to 22.209 million barrels per day.

Distillate fuel oil stocks decreased 2.1 million barrels from the previous report week; distillate stocks are at 136.1 million barrels. EIA reported national distillate demand at 4.048 million barrels per day during the report week, an increase of 290,000 barrels daily.

Propane stocks increased 3.7 million barrels from the previous report week; propane stocks are 94.2 million barrels. The report estimated current demand at 820,000 barrels per day, a decrease of 118,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Net injections into storage totaled 60 Bcf for the week ending August 23, compared with the five-year (2014–18) average net injections of 57 Bcf and last year’s net injections of 66 Bcf during the same week. Working gas stocks totaled 2,857 Bcf, which is 100 Bcf lower than the five-year average and 363 Bcf more than last year at this time.

The average rate of net injections into storage is 30% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 10.7 Bcf/d for the remainder of the refill season, total inventories would be 3,592 Bcf on October 31, which is 100 Bcf lower than the five-year average of 3,692 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.