Energy Information Administration Lowers Crude Oil Forecast

- Retail transportation fuel prices well below last year’s levels

- Broad economic indicators turning bearish

- EIA lowers WTI forecast through 2024

- Natural gas futures prices pointing lower

Sincerely,

Alan Levine, Chairman

Powerhouse

(202) 333-5380

The Matrix

Memorial Day is seen as the start of the summer driving season. The situation facing drivers is much better than last year at this time. RBOB prices topped on June 10, 2022, at $4.3250. The settle for spot RBOB futures last Friday was $2.7034.

The difference was $1.61, a loss in value of nearly 37.5 percent. This is good news for consumers. The news is even better for gasoline retailers whose prices are reportedly $1.20 lower than last year, implying a large increase in margins. Similar observations have been made for diesel fuel, where prices are down $1.65 per gallon at retail. This sharper decline is attributed to a “freight recession” impacting demand.

This is one reason that diesel prices have fallen so dramatically. It is part of a larger picture developing with potentially disconcerting implications for global economic health.

Between April 12 and May 4, price of WTI crude oil fell nearly $20, bottoming at $63.64. The spot futures price has since recovered to $72.67 with Friday’s close. In the larger picture, however, this recovery will not be enough to reconsider EIA’s most recent Short-Term Energy Outlook (STEO.) The Agency has lowered its price expectations for the balance of 2023 and for 2024.

China’s recovery from its self-imposed COVID isolation has been halting. The nation’s Purchasing Managers’ Index has been declining. This implies a reluctance to make new investments to keep up with manufacturing growth requirements.

Economic conditions in the United States are also in flux. The banking sector has been under pressure as various banks have been mismanaging rate differentials for investment and for depositors.

Crude oil supply is dealing with a variety of pressures. Russia has redirected oils to new customers in response to efforts to sanction it behavior in Ukraine. OPEC has announced cuts for the rest of the year. EIA now expects OPEC output of liquids to decline from 34.0 million barrels per day, averaging 33.7 million daily barrels for the balance of 2023.

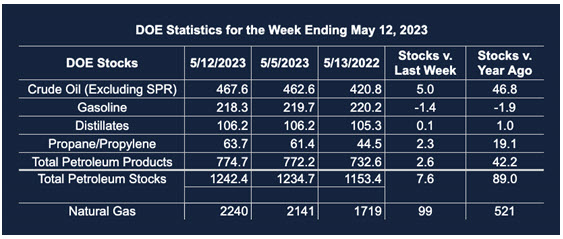

Supply/Demand Balances

Supply/demand data in the United States for the week ended May 19, 2023, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell (⬇) 10.8 million barrels to 1.2316 billion barrels during the week ended May 19, 2023.

Commercial crude oil supplies in the United States were lower (⬇) by 12.5 million barrels from the previous report week to 455.2 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Up (⬆) 0.6 million barrels at 9.3 million barrels

PADD 2: Down (⬇) .3 million barrels to 122.4 million barrels

PADD 3: Down (⬇) 11.5 million barrels to 244.7 million barrels

PADD 4: Down (⬇) 0.6 million barrels to 26.8 million barrels

PADD 5: Down (⬇) 0.7 million barrels to 51.9 million barrels

Cushing, Oklahoma inventories were up (⬆) 1.7 million barrels from the previous report week to 37.2 million barrels.

Domestic crude oil production was up (⬆) 100,000 barrels at 12.3 million barrels daily.

Crude oil imports averaged 5.850 million barrels per day, a daily decrease (⬇) of 1.010 million barrels. Exports increase (⬆) 239,000 barrels daily to 4.549 million barrels per day.

Refineries used 91.7 percent of capacity; 0.3 percentage points lower (⬇) than the previous report week.

Crude oil inputs to refineries increased (⬆) 79,000 barrels daily; there were 16.069 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, decreased (⬇) 54,000 barrels daily to 16.540 million barrels daily.

Total petroleum product inventories increased (⬆) by 1.6 million barrels from the previous report week, up to 776.4 million barrels.

Total product demand increased (⬆) 1.143 million barrels daily to 20.701 million barrels per day.

Gasoline stocks decreased (⬇) 2.1 million barrels from the previous report week; total stocks are 216.3 million barrels.

Demand for gasoline increased (⬆) 529,000 barrels per day to 9.437 million barrels per day.

Distillate fuel oil stocks decreased (⬇) 0.6 million barrels from the previous report week; distillate stocks are at 105.7 million barrels. EIA reported national distillate demand at 4.198 million barrels per day during the report week, a increased (⬆) of 462,000 barrels daily.

Propane stocks increased (⬆) by 3.1 million barrels from the previous report week to 66.7 million barrels. The report estimated current demand at 818,000 barrels per day, an increase (⬆) of 201,000 barrels daily from the previous report week.

Natural Gas

Natural gas prices ended the week of May 26 on a down note, settling at $2.181. The week before reached a new $2.685 high before settling at $2.585. The forty-cent drop in prices during the week came about despite a marginally bullish injection report. Industry sources expected natural gas to add 98Bcf to storage; the reality was 96Bcf more.

Underground storage now stands 29 percent higher than last year at this time. This is certainly no surprise in view of the poor showing for Cooling Degree Days. NOAA reported generation of CDDs for the most recently available week ended May 18 to be 9 CDDs fewer than last year. The Pacific region had the largest positive deviation from last year, a trivial eight CDDs.

Prices were also depressed by gains in supply and declining demand for the week. EIA reported a gain in supply of 200,000 Bcf/d. Notably, dry natural gas production increased 400,000 Bcf/d. Imports from Canada fell 200,000 Bcf/d.

Demand for natural gas fell 1.2 Bcf/d. Power generation fell 1.9 Bcf/d, reflecting the failure of CDDs, offset by modest gains elsewhere in the natural gas economy.

The decline in Henry Hub futures prices erased gains of the previous ten trading sessions, putting the market on track to test $2.00 and an April 4 low of $1.946.

The Atlantic Basin is now in Hurricane Season. Predictions of a “near normal” period do not suggest rally conditions. And an El Nino could offset warm water temperatures in the Atlantic. The possibility of a test below $2.00 cannot be dismissed.

According to the EIA:

Net [natural gas] injections into storage totaled 96 Bcf for the week ended May 19, compared with the five-year (2018–2022) average net injections of 96 Bcf and last year’s net injections of 88 Bcf during the same week. Working natural gas stocks totaled 2,336 Bcf, which is 340 Bcf (17%) more than the five-year average and 529 Bcf (29%) more than last year at this time.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2023 Powerhouse Brokerage, LLC, All rights reserved