ULSD Eases To New Price Support

- Winter ULSD $0.79 lower than last year

- January HO price action less volatile than spot futures

- Loss of global demand could lead to lower refinery production

- Natural gas price breaks support back to 1990’s

The Matrix

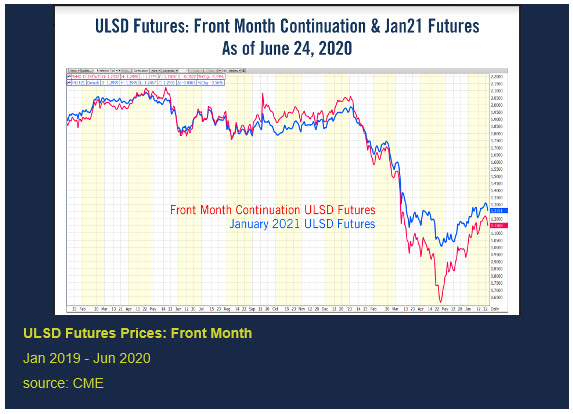

The price of ULSD futures broke a long-standing uptrend during the week ended June 26, 2020. Spot futures bottomed at $0.58 on April 28. Prices reached $1.2425 on Tuesday, June 23, more than doubling in value. The break that has followed has not had much follow through, giving back about eleven cents as the week drew to a close.

The minimal setback has raised concerns among those who have not yet established winter ULSD programs. Dealers are caught up in regret over their failure to buy earlier. Procuring winter ULSD programs is still a good deal. Last year at this time, ULSD was trading around $1.9450, $0.79 cents higher than now. (RBOB’s situation is similar. Current futures prices are trading about $0.57 lower than last June.)

The ULSD chart above is a good illustration of incomplete information available to dealers. Public petroleum information tends to focus on price activity in the nearest month. Futures markets are just that: they provide data on where traders expect prices to be at some time in the future.

ULSD prices bottomed on April 28, 2020. Spot futures (basis May) reached $0.58 at that time. At the same time, January, 2021 priced at $1.03, fully $0.45 higher than spot futures. Buyers of winter fuel oil did not enjoy any price bargains like those of buyers of spot, May HO.

ULSD prices, as noted, then doubled. Spot futures, basis July, printed $1.15 during the week ended June 26. January futures were worth $1.2550—a difference of about $0.1050.

Deferring purchase of winter ULSD cost buyers about $0.2235, substantially less than what might be implied by focusing on front-month prices. This suggests that winter oil may still be attractive.

Refining overcapacity may support this idea. Refiners in the United States and Europe are experiencing competition from state-supported facilities in the Middle East and Asia. They are also operating in a time of reduced demand increasing the possibility of tighter product availability.

Supply/Demand Balances

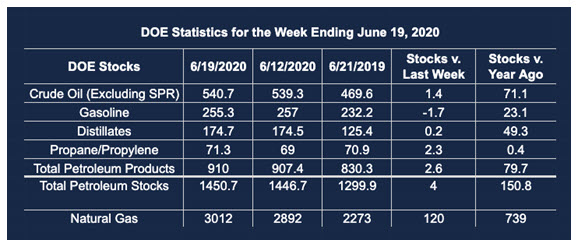

Supply/demand data in the United States for the week ended June 19, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose by 5.9 million barrels during the week ended June 19, 2020.

Commercial crude oil supplies in the United States increased by 1.4 million barrels from the previous report week to 540.7 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.1 million barrels to 12.5 million barrels

PADD 2: Down 0.1 million barrels to 137.9 million barrels

PADD 3: Plus 0.5 million barrels to 308.0 million barrels

PADD 4: Down 0.1 from the previous report week to 25.5 million barrels

PADD 5: Plus 1.0 million barrels to 56.8 million barrels

Cushing, Oklahoma inventories were down 1.0 million barrels from the previous report week to 45.8 million barrels.

Domestic crude oil production rose 0.5 million barrels per day from the previous report week to 11.0 million barrels daily.

Crude oil imports averaged 6.540 million barrels per day, a daily decrease of 102,000 barrels. Exports rose 695,000 barrels daily to 3.157 million barrels per day.

Refineries used 74.6 percent of capacity, plus 0.8% from the previous report week.

Crude oil inputs to refineries increased 240,000 barrels daily; there were 13.840 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 163,000 barrels daily to reach 14.162 million barrels daily.

Total petroleum product inventories rose 2.5 million barrels from the previous report week.

Gasoline stocks decreased 1.7 million barrels daily from the previous report week; total stocks are 255.3 million barrels.

Demand for gasoline rose 738,000 barrels per day to 8.608 million barrels per day.

Total product demand increased 1.058 million barrels daily to 18.348 million barrels per day.

Distillate fuel oil stocks increased 0.2 million barrels from the previous report week; distillate stocks are at 174.7 million barrels. EIA reported national distillate demand at 3.466 million barrels per day during the report week, a decrease of 89,000 barrels daily.

Propane stocks increased 2.4 million barrels from the previous report week; propane stocks are 71.3 million barrels. The report estimated current demand at 701,000 barrels per day, a decrease of 372,000 barrels daily from the previous report week.

Natural Gas

Support for natural gas futures broke last week. Prices fell sharply through $1.52 on release of the EIA’s Weekly Natural Gas Storage Report. These levels have not been seen since the early 1990’s. The loss of value continues to reflect high storage levels and erosion of domestic demand as well as fewer LNG exports. Terminal receipts of LNG are reportedly averaging 4.0 Bcf per day in June, 1.4 Bcf/d lower than last year.

According to EIA:

The net injections into storage totaled 120 Bcf for the week ending June 19, compared with the five-year (2015–19) average net injections of 73 Bcf and last year’s net injections of 103 Bcf during the same week. Working natural gas stocks totaled 3,012 Bcf, which is 466 Bcf more than the five-year average and 739 Bcf more than last year at this time.

The average rate of injections into storage is 18% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 8.8 Bcf/d for the remainder of the refill season, the total inventory would be 4,189 Bcf on October 31, which is 466 Bcf higher than the five-year average of 3,723 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2020 Powerhouse, All rights reserved.