Oil Price Outlook Turns Bearish

- Demand takes control of oil price outlook

- Global trade stalling

- PMI falls below 50, the first time since 2012

- Higher than average injections pressure natural gas prices

The Matrix

Petroleum demand has taken center stage among analysts. Availability of supply has generally led thinking about oil balances. The apparent success of OPEC+ crude oil restraint and dramatic growth in U.S. crude oil production and exports has pushed supply issues out of the analytical spotlight at least for now.

Concern over the state of the global economy has become central to thinking about oil demand as represented by price. Tensions have been heightened by U.S./China economic conflict. Apparent success in tariff discussions between the United States and Mexico comes with its own caveats.

These geopolitical issues are only current examples of expanding uncertainty about global trade and economics. Data measuring trade and investment in the global economy have fallen sharply in the first five months of 2019.

The World Bank has reduced its estimate of growth to 2.6 percent from 3.6 percent. The bank notes that this would be the world’s slowest growth since 2016. The bank projects a 2019 growth for the U.S. of 2.5 percent, down from 2.9 percent in 2018. China is expected to have growth of 6.2 percent from 2018’s 6.6 percent.

These data don’t include the impact of U.S. threats to impose 25 percent tariffs on $300 billion of Chinese goods. A similar imposition on Mexico could reach $350 billion.

Other economic statistics support this negative analysis. Factory activity globally fell to its lowest level since October 2016. The Purchasing Manager’s Index fell below 50, the lowest since 2012.

WTI Crude Oil Daily Price Chart Aug 2017 – June 2019 source: eSignal.com

WTI Crude Oil Daily Price Chart Aug 2017 – June 2019 source: eSignal.com

The effect of these negative statistics can be seen on energy price charts. WTI prices are under pressure and could move to $50 or even lower. Elliott Wave analysis suggests that such a move might not complete the down wave now under way. One possible objective is $46.50.

Supply/Demand Balances

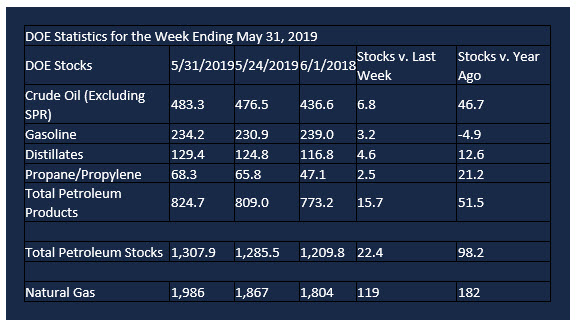

Supply/demand data in the United States for the week ending May 31, 2019, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose 22.4 million barrels during the week ending May 31, 2019.

There were builds in stocks of gasoline, K-jet fuel, distillates, residual fuel, propane, and other oils. There was a draw in stocks of fuel ethanol.

Commercial crude oil supplies in the United States rose 6.8 million barrels from the previous report week to 483.3 million barrels.

Crude oil supplies increased in four of the five PAD Districts. PADD 1 (East Coast) crude oil stocks rose 0.9 million barrels, PADD 2 (Midwest) stocks advanced 1.3 million barrels, PADD 3 (Gulf Coast) stocks rose 3.4 million barrels, and PADD 5 (West Coast) stocks increased 1.2 million barrels. Crude oil stocks in PADD 4 (Rockies) were unchanged from the previous report week.

Cushing, Oklahoma inventories were up 1.7 million barrels from the previous report week to 50.8 million barrels.

Domestic crude oil production rose 100,000 barrels per day from the previous report week to 12.4 million barrels daily.

Crude oil imports averaged 7.927 million barrels per day, a daily increase of 1.065 million barrels. Exports decreased 19,000 barrels daily to 3.298 million barrels per day.

Refineries used 91.8 percent of capacity, an increase of 0.6 percentage points from the previous report week.

Crude oil inputs to refineries increased 171,000 barrels daily; there were 16.938 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 119,000 barrels daily to 17.227 million barrels daily.

Total petroleum product inventories rose 15.6 million barrels from the previous report week.

Gasoline stocks increased 3.2 million barrels daily from the previous report week; total stocks are 234.1 million barrels.

Demand for gasoline rose 48,000 barrels per day to 9.441 million barrels per day.

Total product demand decreased 2.009 million barrels daily to 19.449 million barrels per day.

Distillate fuel oil stocks increased 4.6 million barrels from the previous report week; distillate stocks are at 129.4 million barrels. National distillate demand was reported at 3.387 million barrels per day during the report week. This was a weekly decrease of 895,000 barrels daily.

Propane stocks increased 2.5 million barrels from the previous report week; propane stocks are 68.3 million barrels. Current demand is estimated at 818,000 barrels per day, a decrease of 103,000 barrels daily from the previous report week.

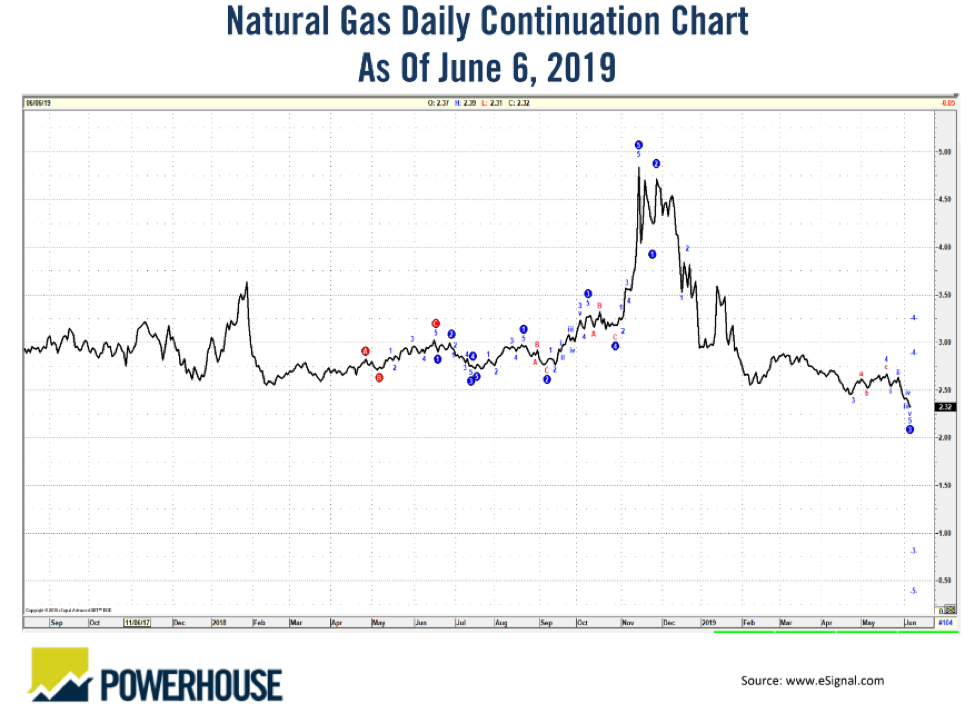

Natural Gas

According to the Energy Information Administration:

Net injections into storage totaled 119 Bcf for the week ending May 31, compared with the five-year (2014–18) average net injections of 102 Bcf and last year’s net injections of 93 Bcf during the same week. Working gas stocks totaled 1,986 Bcf, which is 240 Bcf lower than the five-year average and 182 Bcf more than last year at this time.

The average rate of net injections into storage is 44% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 9.6 Bcf/d for the remainder of the refill season, total inventories would be 3,452 Bcf on October 31, which is 240 Bcf lower than the five-year average of 3,692 Bcf for that time of year.

Natural Gas Daily Price Chart Aug 2017 – June 2019 source: eSignal.com

Above average injections are contributing to weakness in natural gas prices. Technical charts suggest continued weakness and a possible break of $2.00 for spot futures.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.