WTI Price Forecasts Shaped by Contradictory Actions

- EIA projects WTI crude oil at $62 in 2021

- China economy outpacing expectations

- Trade accord reveals unrealistic objectives

- LNG exports aiming at 8.9 Bcf.

The Matrix

Events that would have roiled oil markets in the past are not affecting oil prices as intensely as in the past. An attack on Saudi producing assets and follow-through from the killing of an Iranian general produced price spikes that quickly retreated. Powerhouse noted last week that the availability of crude oil from the United States to global markets is remaking the global oil industry.

The Energy Information Administration (EIA) dealt with these events in the most recent Short-Term Energy Outlook (STEO.) EIA now projects a lower crude oil price early in 2020 followed by higher prices in the second half of 2020 and in 2021. The higher price reflects the view that “recent geopolitical events” could bring WTI to a spot price of $59 in 2020. EIA expects that “market fundamentals” will pressure prices towards $62 in 2021 even as political effects recede.

Some of EIA’s more bullish thinking may have developed from expectations for China’s economy and the implications of the first-phase of the U.S./China trade deal. Data about the economy have turned firmer than expected. Chinese GDP showed a six percent fourth quarter gain over the comparable period the prior year. Retail sales rose eight percent over June and higher investment as well.

These bullish data, when joined with the implications of the trade accord, could wind up with untenable results. The terms of the deal suggest a very large – some say massive – increase in Chinese intake of U.S. energy. If this were to happen, the disruptive impact on global balances could be very serious. China has signed on to 2020 energy imports of $ 27.6 billion, doubling recent record months.

If this were to happen, China would account for about a third of U.S. crude exports, according to press reports. Such a happening would mean that U.S. exporters would become reliant on a single customer for a large amount of exports.

It also raises the question of competitive reaction. Other national suppliers could react to an attack on their market shares, expanding the trade wars now operating.

Supply/Demand Balances

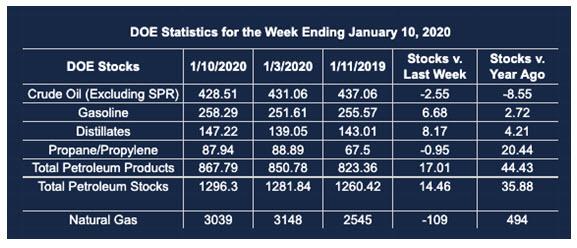

Supply/demand data in the United States for the week ending Jan. 10, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose by 14.5 million barrels during the week ending Jan. 10, 2020.

Commercial crude oil supplies in the United States decreased by 2.5 million barrels from the previous report week to 428.5 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.6 million barrels to 9.9 million barrels

PADD 2: Down 0.3 million barrels to 126.2 million barrels

PADD 3: Down 3.0 million barrels to 218.4 million barrels

PADD 4: Down 0.9 million barrels to 21.9 million barrels

PADD 5: Plus 1.1 million barrels to 52.1 million barrels

Cushing, Oklahoma inventories rose 0.3 million barrels from the previous report week to 35.8 million barrels.

Domestic crude oil production rose 100,000 barrels per day from the previous report week t0 13.0 million barrels daily.

Crude oil imports averaged 6.730 million barrels per day, a daily increase of 379,000 barrels. Exports fell 1.398 million barrels daily to 3.064 million barrels per day.

Refineries used 93.0 percent of capacity, down 1.5% from the previous report week.

Crude oil inputs to refineries decreased 386,000 barrels daily; there were 16.897 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 284,000 barrels daily to reach 17.484 million barrels daily.

Total petroleum product inventories rose 13.6 million barrels from the previous report week.

Gasoline stocks increased 9.1 million barrels daily from the previous report week; total stocks are 251.6 million barrels.

Demand for gasoline fell 828,000 barrels per day to 8.133 million barrels per day.

Total product demand decreased 571,000 barrels daily to 19.351 million barrels per day.

Distillate fuel oil stocks increased 5.3 million barrels from the previous report week; distillate stocks are at 139.1 million barrels. EIA reported national distillate demand at 3.373 million barrels per day during the report week, an increase of 318,000 barrels daily.

Propane stocks increased 0.7 million barrels from the previous report week; propane stocks are 88.9 million barrels. The report estimated current demand at 1.514 million barrels per day, an increase of 229,000 barrels daily from the previous report week.

Natural Gas

The STEO also offered a forecast for natural gas exports. EIA expects the United States to continue to be a net exporter into 2021. LNG exports rose as new facilities came on line. Net exports are expected to be 7.3 Bcf in 2020, rising to 8.9 Bcf in the following year.

According to EIA:

The net withdrawal from storage totaled 109 Bcf for the week ending January 10, compared with the five-year (2015–19) average net withdrawal of 184 Bcf and last year’s net withdrawal of 82 Bcf during the same week. Working natural gas stocks totaled 3,039 Bcf, which is 149 Bcf more than the five-year average and 494 Bcf more than last year at this time.

The average rate of withdrawal from storage is 15% lower than the five-year average so far in the withdrawal season (November through March). If the rate of withdrawal from storage matched the five-year average of 14.7 Bcf/d for the remainder of the withdrawal season, the total inventory would be 1,846 Bcf on March 31, which is 149 Bcf higher than the five-year average of 1,697 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2020 Powerhouse, All rights reserved.