The U.S. Achieves Net Oil Exporter Status

- Exports of all oils are geopolitically significant

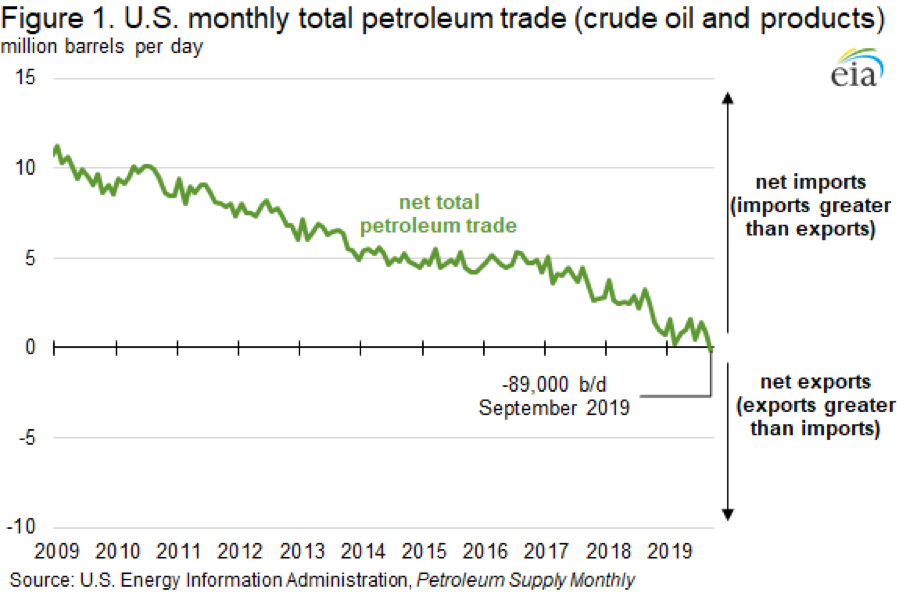

- Net oil movements favored exports in September 2019

- Crude oil is still a net import

- Natural gas nearly 600 Bcf more in storage than last year

The Matrix

Changes in the organization of the petroleum industry have been far-reaching. Methods of production, pipeline distribution, and product specification are examples of those changes.

Perhaps no change has been as dramatic and geopolitically significant as the United States emerging as a net exporter of crude oil. The U.S. enacted limits on the export of crude oil in 1975. These export constraints were a response to price and supply volatility developing as OPEC expanded its market power.

The United States was in a period of declining domestic production in the 1970s. By the mid-2000s, however, fracturing technology became significant, and U.S. crude oil production started to rise.

The pressure to allow exports grew, especially as pipeline distribution patterns did not fully reflect U.S. refinery requirements. Domestic crude oil exports started in December 2015 for the first time in many years.

U.S. Petroleum Trade – 4-week average 2009 – 2019 Source: EIA

In September 2019, exports of crude oil and products exceeded comparable imports by 89,000 barrels per day. The United States became a net exporter for the first time since monthly record-keeping began in 1973. (See Figure 1.)

The fact of net export status for the United States is more than a matter of statistical interest. The country is still a net importer of crude oil. It imports heavy high-sulfur crude oils that are well-configured for domestic refineries. Most of U.S. crude oil imports come from Canada or Mexico, limiting our exposure to political uncertainty overseas.

The Energy Information Administration anticipates the net export position will grow. EIA projects net petroleum exports to average 751,000 barrels per day in 2020. The United States would be a net petroleum exporter on an annual basis for the first time.

A net petroleum export position has several benefits for the broader economy. Net exports help lower the trade deficit. Net petroleum exports also support U.S. energy security and allow for strategic positioning on international energy issues.

Supply/Demand Balances

Supply/demand data in the United States for the week ending Nov. 29, 2019, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell by 4.9 million barrels during the week ending Nov. 29, 2019.

Commercial crude oil supplies in the United States decreased by 4.9 million barrels from the previous report week to 447.1 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: fell 0.3 million barrels to 11.0 million barrels

PADD 2: Plus 0.3 million barrels to 131.2 million barrels

PADD 3: Fell 2.8 million barrels to 229.8 million barrels

PADD 4: Down 0.6 million barrels to 23.8 million barrels

PADD 5: Down 1.5 million barrels to 51.2 million barrels

Cushing, Oklahoma inventories fell 0.3 million barrels from the previous report week to 43.8 million barrels.

Domestic crude oil production was unchanged from the previous report week at 12.9 million barrels daily.

Crude oil imports averaged 5.989 million barrels per day, a daily decrease of 201,000 barrels. Exports fell 345,000 barrels daily to 3.135 million barrels per day.

Refineries used 91.9 percent of capacity, up 1.6% from the previous report week.

Crude oil inputs to refineries increased 464,000 barrels daily; there were 16.798 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 487,000 barrels daily to reach 17.284 million barrels daily.

Total petroleum product inventories were unchanged from the previous report week.

Gasoline stocks increased 3.4 million barrels daily from the previous report week; total stocks are 229.4 million barrels.

Demand for gasoline fell 172,000 barrels per day to 9.032 million barrels per day.

Total product demand decreased 17,000 barrels daily to 21.089 million barrels per day.

Distillate fuel oil stocks increased 3.1 million barrels from the previous report week; distillate stocks are at 119.5 million barrels. EIA reported national distillate demand at 3.556 million barrels per day during the report week, a decrease of 837,000 barrels daily.

Propane stocks decreased 1.7 million barrels from the previous report week; propane stocks are 91.8 million barrels. The report estimated current demand at 1.773 barrels per day, an increase of 534,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

The net withdrawal from storage totaled 19 Bcf for the week ending November 29, compared with the five-year (2014–18) average net withdrawal of 41 Bcf and last year’s net withdrawal of 62 Bcf during the same week. Working natural gas stocks totaled 3,591 Bcf, which is 9 Bcf lower than the five-year average and 591 Bcf more than last year at this time.

Expectations for December weather have turned bearish. NOAA’s weather model moved lower. Thirty HDDs were taken from its forecast and natural gas futures fell nearly 12 cents as markets opened on December 9th.

The most recent decline in natural gas futures began on November 5th. Natural gas futures reached $2.905. It was the subject of David Thompson’s Technical Analysis Update of November 7, 2019. (If you missed David’s work, send us a note at [email protected])

The technical analysis identified an island top reversal formation. The reversal is initially created by a bullish price gap. The market then stalls and eventually a bearish price gap occurs reversing most, if not all, of the previous advance in price. Powerhouse’s objectives of $2.70 and then $2.64 have been achieved.

The new gap approaches support at $2.187. The character of the gap is unclear. Nonetheless, the symmetry of price gaps at the top and now near support should not be ignored. Natural gas may be near a significant price point.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.