Oil Prices Remain Directionless

- Brent crude oil volume cut by pipeline break

- U.S. production approached ten million barrels daily

- Spring gasoline crack spread breaks resistance

- Natural gas prices challenging support

The Matrix

The tension between U.S. crude oil production growth and an uncertain foreign geopolitical climate has brought trading in WTI crude oil futures to a narrow, largely directionless, range.

The increasingly untenable overseas benchmark crude oil, Brent, (Brent’s value as a price marker is increasingly at question as more and more crude oil streams are needed to fill out the Brent stream’s composition) has been supported by a pipeline break. The line carried 450,000 barrels of crude oil that supported the Brent price. And Nigerian labor unrest, an old story in the region, cost a day’s production. The union returned to work but observers noted that strikes could resume in January.

U.S. production has renewed its upward trajectory, as noted here before. And as production approaches ten million barrels daily, the effect of plentiful supply muting international events becomes more obvious.

Even though global geopolitics may be having less impact on U.S. price activity, prices will still react to seasonal influences. Gasoline’s seasonal autumn sell-off has been cut short by the effect of H. Harvey. This has created uncertainty about the strength of a spring gasoline rally among traders. Typically, gasoline prices have rallied consistently, starting around year-end.

Prices tend to be supported by refinery maintenance and resulting tighter gasoline supply which begins at this time too. An analysis of total planned refinery turnarounds in the United States indicates refinery shutdowns moving toward 1.4 million barrels daily by February. This is somewhat fewer barrels off-line than refiners’ experience in 2017 and could mute a rally that reflects tight gasoline supply. On the other hand, global turnaround plans are approaching 6.5 million barrels daily offline, near the upper end of recent experience. Global refining slowdowns peak early in March.

Prices: May 2018 Crack Spread July 2017 – Dec 2017

One analyst notes that a significant rally is more likely when prices start from a very low level. That is not the case just now. Gasoline trading around $1.70 is priced in the middle of the range starting in October, 2017, not nearly low enough to be considered to be oversold.

Supply/Demand Balances

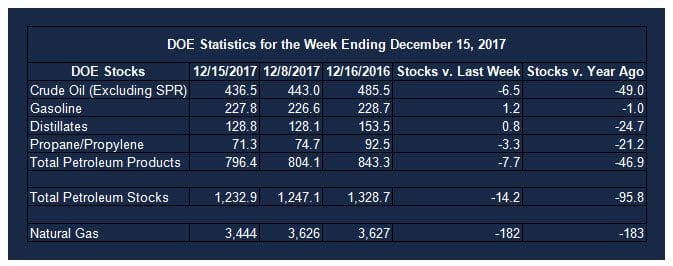

Supply/demand data in the United States for the week ending December 15, 2017 were released by the Energy Information Administration.

Total commercial stocks of petroleum fell 14.2 million barrels during the week ending December 15, 2017.

Draws were reported in stocks of fuel ethanol, K-jet fuel, residual fuel oil, propane, and other oils. Builds were reported in stocks of gasoline and distillates.

Commercial crude oil supplies in the United States decreased to 436.5 million barrels, a draw of 6.5 million barrels.

Crude oil supplies decreased in four of the five PAD Districts. PAD District 1 (East Coast) crude oil stocks fell 1.3 million barrels, PADD 2 (Midwest) crude stocks declined 1.4 million barrels, PADD 3 (Gulf Coast) stocks retreated 3.6 million barrels, and PADD 5 (West Coast) stocks decreased 0.6 million barrels. PAD District 4 (Rockies) crude oil stocks rose 0.5 million barrels.

Cushing, Oklahoma inventories increased 0.8 million barrels from the previous report week to 53.0 million barrels.

Domestic crude oil production increased 9,000 barrels daily to 9.789 million barrels per day from the previous report week.

Crude oil imports averaged 7.834 million barrels per day, a daily increase of 471,000 barrels. Exports rose 772,000 barrels daily to 1.858 million barrels per day.

Refineries used 94.1 per cent of capacity, an increase of 0.7 percentage points from the previous report week.

Crude oil inputs to refineries increased 111,000 barrels daily; there were 17.063 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 125,000 barrels daily to 17.404 million barrels daily.

Total petroleum product inventories saw a decrease of 7.7 million barrels from the previous report week.

Gasoline stocks rose 1.2 million barrels from the previous report week; total stocks are 227.8 million barrels.

Demand for gasoline increased 336,000 barrels per day to 9.426 million barrels daily.

Total product demand increased 640,000 barrels daily to 21.111 million barrels per day.

Distillate fuel oil supply rose 0.8 million barrels from the previous report week to 128.8 million barrels. National distillate demand was reported at 3.926 million barrels per day during the report week. This was a weekly decrease of 454,000 barrels daily.

Propane stocks decreased 3.3 million barrels from the previous report week to 71.3 million barrels. Current demand is estimated at 1.324 million barrels per day, a decrease of 64,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Higher-than-normal withdrawals result in larger five-year average deficit levels. Net withdrawals from storage totaled 182 Bcf for the week ending December 15, compared with the five-year (2012–16) average net withdrawal of 125 Bcf and last year’s net withdrawals of 200 Bcf during the same week. Working gas stocks totaled 3,444 Bcf, which is 84 Bcf less than the five-year average and 183 Bcf less than last year at this time.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright © 2017 Powerhouse, All rights reserved.