Oil Price Volatility Returns

- WTI crude oil support holds $50.50

- Global economy under stress

- Crude oil stocks increase

- Natural gas prices inch higher

The Matrix

Weeks of indecisive trading came to a halt last week. Anxiety over the implications of a trade war between the United States and China caused energy prices to plunge. WTI crude oil lost five dollars, breaking support at $50.52.

The crude oil conversation during the week turned on tensions in the Persian Gulf and concerns over a softening global economy. Then, Saudi Arabia announced it would balance global oil markets. Saudi’s statement was seen as bullish by futures markets. Prices recovered, nearly eliminating the whole weekly decline in price.

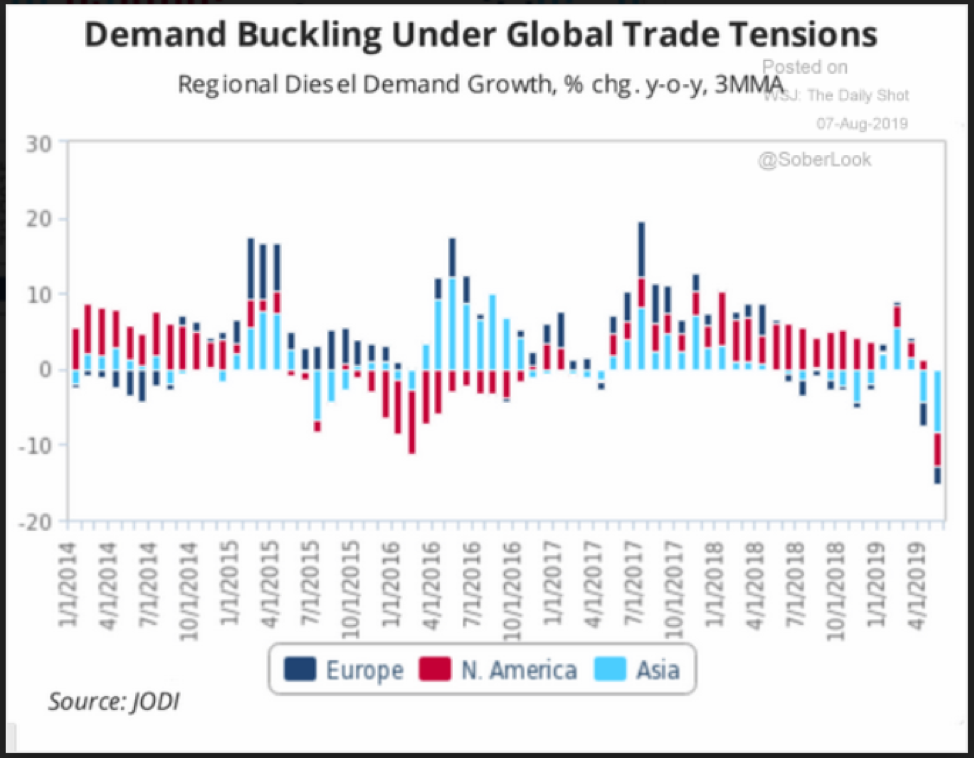

Germany has reported an important indication of global economic weakness. Industrial output in Germany fell by 1.5 percent in June, far more than had been forecast. The U.S./China trade war figures into this drop because both are important off-takers of German manufactured goods. Declines in metal production, machinery and auto manufacturing contributed to the lower level. Analysts are now anticipating a “technical” recession – two consecutive quarters of lower activity.

Such volatility has injected significant uncertainty into the price outlook. Fundamental data have largely supported the short side of pricing. The International Energy Agency (IEA) reported that global demand fell 160,000 barrels daily in May and year-to-date demand growth of 520,000 barrels daily was the lowest since 2008. IEA also lowered demand projections for 2019 and 2020.

Diesel Demand (Demand Growth year-over-year) Jan. 2014 – Jun. 2019 Source: Joint Oil Data Initiative

Crude oil supplies have continued to grow. Non-OPEC crude oil is expected to grow 1.9 million barrels daily despite softening demand. The United States has recovered from the impact of Hurricane Barry. Production in the U.S. reached 12.3 million barrels per day in DOE’s most recent release.

Persian Gulf events are potentially bullish. They could easily offset otherwise bearish fundamentals. Iran has reportedly been distorting GPS data on its tankers. Military support from the U.S., the UK and other nations has helped avoid problems in ship movement. The situation could change, initiating conflict in the area with bullish price effect.

Supply/Demand Balances

Supply/demand data in the United States for the week ending August 2, 2019, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell 10.4 million barrels during the week ending August 2, 2019.

There were builds in stocks of gasoline, K-jet fuel, distillate fuel, residual fuel, and propane. There were draws in stocks of fuel ethanol and other oils.

Commercial crude oil supplies in the United States rose 2.4 million barrels from the previous report week to 438.9 million barrels.

Crude oil supplies decreased in two of the five PAD Districts. PAD District 1 (East Coast) crude oil stocks declined 1.7 million barrels and PADD 2 (Midwest) stocks fell 2.4 million barrels. PAD District 3 (Gulf Coast) crude stocks rose 5.5 million barrels, PADD 4 (Rockies) stocks increased 0.2 million barrels, and PADD 5 (West Coast) stocks grew 0.8 million barrels.

Cushing, Oklahoma inventories fell 1.5 million barrels from the previous report week to 47.4 million barrels.

Domestic crude oil production rose 100,000 barrels per day from the previous report week to 12.3 million barrels daily.

Crude oil imports averaged 7.148 million barrels per day, a daily increase of 485,000 barrels. Exports declined 709,000 barrels daily to 1.865 million barrels per day.

Refineries used 96.4 percent of capacity, up 3.4% from the previous report week.

Crude oil inputs to refineries increased 786,000 barrels daily; there were 17.777 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, 633,000 barrels daily to 18.117 million barrels daily.

Total petroleum product inventories rose 8.0 million barrels from the previous report week.

Gasoline stocks increased 4.4 million barrels daily from the previous report week; total stocks are 235.2 million barrels.

Demand for gasoline rose 92,000 barrels per day to 9.651 million barrels per day.

Total product demand increased 185,000 barrels daily to 21.481 million barrels per day.

Distillate fuel oil stocks increased 1.5 million barrels from the previous report week; distillate stocks are at 137.5 million barrels. EIA reported national distillate demand at 3.886 million barrels per day during the report week, an increase of 1,000 barrels daily.

Propane stocks increased 2.9 million barrels from the previous report week; propane stocks are 83.3 million barrels. The report estimated current demand at 762,000 barrels per day, a decrease of 379,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Net injections into storage totaled 55 Bcf for the week ending August 2, compared with the five-year (2014–18) average net injections of 43 Bcf and last year’s net injections of 46 Bcf during the same week. Working gas stocks totaled 2,689 Bcf, which is 111 Bcf lower than the five-year average and 343 Bcf more than last year at this time.

The average rate of net injections into storage is 33% higher than the five-year average so far in the refill season (April through October.) If the rate of injections into storage matched the five-year average of 9.9 Bcf/d for the remainder of the refill season, total inventories would be 3,581 Bcf on October 31, which is 111 Bcf lower than the five-year average of 3,692 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.