MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

Oil prices fell midweek, with supplies rising despite expected declines in demand, and the U.S.-China trade war heightening worries over global economic growth. U.S. oil production rose again, and inventories rose, contradicting industry expectations of another stock drawdown. The International Energy Agency revised downward its forecast of global oil demand. Today, prices bounced back. Buying interest is being stimulated by Saudi Arabian announcements signaling possible cuts in production. The uptick in prices may have hit a technical level setting off buy signals among traders. Crude prices may still end the week in the red, depending on whether the Saudi announcements are strengthened today. Our weekly price review covers hourly forward prices from 9AM EST Friday August 2nd through Friday August 9th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

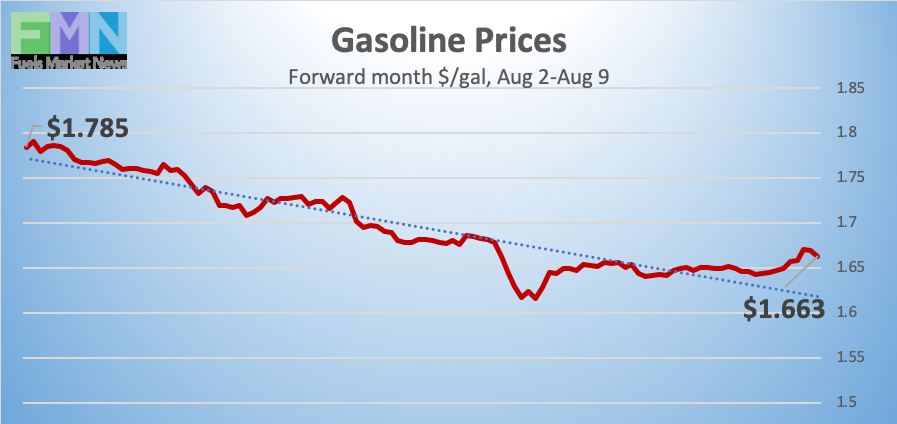

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.755/gallon on Friday August 2nd, and they opened at $1.6505/gallon on Friday, August 9th. This was a sharp drop of 10.45 cents (6%,) continued to add to losses from last week’s drop of 12.53 cents (6.7%.) U.S. average retail prices also fell during the week ended August 5th. This week brought a significant addition to inventories, contrary to industry expectations. Gasoline prices ticked up this morning, following crude oil’s recovery, though the week still appears to be heading for an end in the red. Trades are occurring mainly in the range of $1.66-$1.69/gallon. The latest price is $1.6806/gallon.

DIESEL PRICES

Diesel opened on the NYMEX at $1.8709/gallon on Friday August 2nd and opened on Friday August 9th at $1.7846/gallon, a significant weekly decline of 8.63 cents (4.6%), adding to last week’s loss of 3.61 cents (1.9%.) Diesel prices ticked up this morning alongside crude and gasoline, though weekly prices remain in the red. Contracts currently are trading in the $1.79-$1.82/gallon range. The latest price is $1.8123/gallon.

WEST TEXAS INTERMEDIATE PRICES

PRICE MOVERS THIS WEEK : BRIEFING

Oil prices fell this week, as supplies rose. Industry experts had expected another drawdown of oil inventories, but the actual buildup sent prices down. Global worries over the economic outlook are rising. Last week’s announcement of a 25 basis point rate cut by the Fed was followed by currency movements in other countries. On Monday, China let the Yuan fall below its typical 7-to-1 ration with the U.S. Dollar for the first time in a decade, causing U.S. President Donald Trump to accuse China of currency manipulation. The move was interpreted as retaliation for the additional 10% tariff placed on $300 billion worth of additional Chinese goods.

China halted the downslide of its currency overnight, and the government appeared to be working to calm global markets by fixing the Yuan slightly higher than expected. Nonetheless, a variety of other countries have taken monetary action, including India, Thailand, and New Zealand, which all cut interest rates.

Today, oil prices have bounced back up, though they appear to be flattening at under $54.50/b. Saudi Arabia announced that it was contacting other oil producers to discuss the price drop, apparently signaling that it would cut its own production even deeper than planned in order to support prices. The uptick in prices sent buy signals to the market, but no actual plans have been set. The week still could end in the red.

The U.S. Energy Information Administration (EIA) reported that U.S. crude oil production rose to 12.3 million barrels per day (mmbpd) during the week ended August 2nd. The weekly record-high was 12.4 mmbpd reported for the week ended May 31st.

On Tuesday, the American Petroleum Institute (API) reported a drawdown of 3.4 million barrels (mmbbls) from crude oil inventories, plus a draw of 1.1 mmbbls from gasoline inventories, and an addition of 1.2 mmbbls to diesel inventories. Prices fell sharply when official statistics contradicted this and showed across-the-board additions to inventory. EIA reported a crude stock build of 2.385 mmbbls, plus additions of 4.437 mmbbls to gasoline inventories and 1.529 mmbbls to diesel inventories. The net stock build was 8.351 mmbbls, a stark contrast to the 3.3-mmbbl drawdown anticipated by industry experts.