Higher Prices Possible despite Bloated Distillate Inventories?

- Distillate fuel oil stocks near 38-year high

- The market environment differs from 1982

- Crude oil output falls

- Natural gas storage 11% higher than 5-year average

The Matrix

Inventories of distillate fuel oils are only now starting to retreat from the highest level recorded since December 1982. Distillate fuel oil stocks reached 186 million barrels 38 years ago, reflecting falling demand and rising production on world markets.

Stocks of distillate fuel oil in the United States were put at 178 million barrels on Aug. 7, 2020, slightly below the previous week’s estimate of 180 million barrels.

The situation today has much in common with what was happening in 1982, but there are differences that could lead to a more bullish price for distillate fuels. These include improving demand for petroleum products in the U.S.

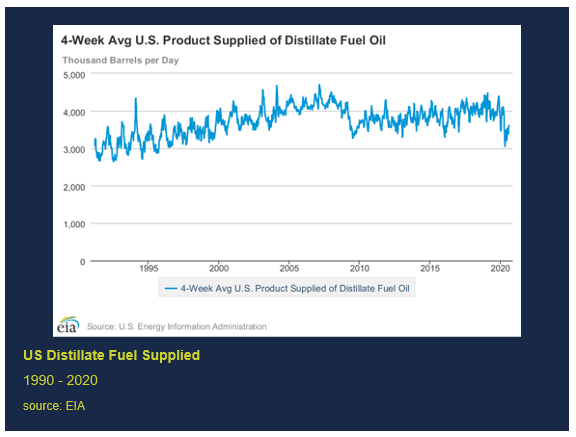

The chart of product supplied (a surrogate for demand) shows that distillate demand, lags last year-to-date by 10%.

Within that statistic, however, distillate fuel oil demand has been recovering from this year’s low of 3.0 million barrels daily, recorded during the week ending May 1, 2020. This is an 18% improvement, at a time when distillate prices are typically in a pre-winter rally.

U.S. crude oil production has fallen during this Covid-influenced period. Output fell to 10.7 million barrels daily during the week ending August 7.

The Energy Information Administration has reflected lower production in its most recent projections. EIA now expects U.S. crude oil production to average 11.26 million barrels per day for 2020. This is a decline of nearly one million barrels daily from last year. EIA’s last estimate for production showed a decline of 600 thousand barrels per day.

An additional potentially bullish price factor is the return of inflation. One non-governmental forecaster expects inflation in the United States to be 2.5% in the next 12 months.

Prices for ULSD today are well above recent lows. Many potential buyers have looked on those prices and are stuck with the idea that they “missed” the move. For reference, Powerhouse offers the thought that the distillate fuel oil price over the past ten years has averaged around $2.22 cents. Markets are well below that number.

Supply/Demand Balances

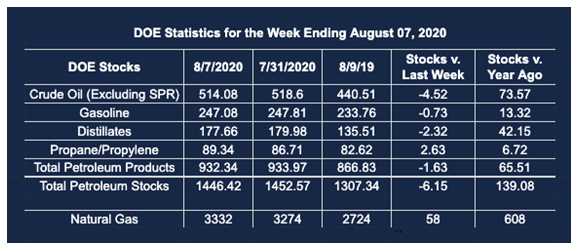

Supply/demand data in the United States for the week ending Aug. 7, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell by 6.2 million barrels during the week ending August 2020.

Commercial crude oil supplies in the United States decreased by 4.5 million barrels from the previous report week to 514.1 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 1.0 million barrels from previous report week to 11.0 million barrels

PADD 2: Plus 2.2 million barrels to 142.4 million barrels

PADD 3: Down 6.7 million barrels to 281.4 million barrels

PADD 4: Plus 0.4 million barrels to 25.4 million barrels

PADD 5: Plus 0.6 million barrels to 53.9 million barrels

Cushing, Oklahoma inventories were up 1.3 million barrels from the previous report week to 53.3 million barrels.

Domestic crude oil production was fell 300,000 barrels per day from the previous report week to 10.7 million barrels daily.

Crude oil imports averaged 5.621 million barrels per day, a daily decrease of 389,000 barrels. Exports increased 324,000 barrels daily to 3.143 million barrels per day.

Refineries used 81.0% of capacity, up 1.4% from the previous report week.

Crude oil inputs to refineries increased 21,000 barrels daily; there were 14.658 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 4,000 barrels daily to reach 15.104 million barrels daily.

Total petroleum product inventories fell 1.7 million barrels from the previous report week.

Gasoline stocks decreased 0.7 million barrels daily from the previous report week; total stocks are 247.1 million barrels.

Demand for gasoline rose 266,000 barrels per day to 8.883 million barrels per day.

Total product demand increased 1.457 million barrels daily to 19.369 million barrels per day.

Distillate fuel oil stocks decreased 2.3 million barrels from the previous report week; distillate stocks are at 177.7 million barrels. EIA reported national distillate demand at 3.862 million barrels per day during the report week, an increase of 162,000 barrels daily.

Propane stocks increased 2.6 million barrels from the previous report week; propane stocks are 89.3 million barrels. The report estimated current demand at 1.119 million barrels per day, an increase of 333,000 barrels daily from the previous report week.

Natural Gas

Production of dry natural gas rose during the week ending August 12. Over a longer time frame, EIA expects production to “remain lower than the 98.3 billion cubic feet per day (Bcf/d) production level reached in the first quarter of 2020. Final quarter 2021 production is forecast at 89.3 Bcf/d. This could support price. The next major resistance is at $2.90, the high seen last November.

According to the EIA:

The net injections [of natural gas] into storage totaled 58 Bcf for the week ending August 7, compared with the five-year (2015–19) average net injections of 44 Bcf and last year’s net injections of 51 Bcf during the same week. Working natural gas stocks totaled 3,332 Bcf, which is 443 Bcf more than the five-year average and 608 Bcf more than last year at this time.

The average rate of injections into storage is 11% higher than the five-year average so far in the refill season (April through October). Working gas stocks exceeded the 5-year max. If the rate of injections into storage matched the five-year average of 9.8 Bcf/d for the remainder of the refill season, the total inventory would be 4,166 Bcf on October 31, which is 443 Bcf higher than the five-year average of 3,723 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2020 Powerhouse, All rights reserved.