The oil complex maintained last week’s gains, with midweek reductions in inventory bolstering prices. Prices are tapering down gently today, but West Texas Intermediate (WTI) crude oil futures appear to be cleaving to the $42 a barrel level, which will afford another finish in the black this week. Gasoline and diesel prices also are declining this morning, though gasoline prices appear to be holding on for a finish in the black, while diesel prices are heading for a finish in the red. Oil prices are receiving support from the inventory drawdowns, declining unemployment, and news of an increase in retail sales. U.S. crude production also fell, which supports prices, though it also signals difficult times for the U.S. industry. These bullish price factors are moderated by the relentless increase in coronavirus infections and the concern that recent demand growth was made possible by government stimulus payments, which now have expired. The next phase of economic stimulus remains under debate.

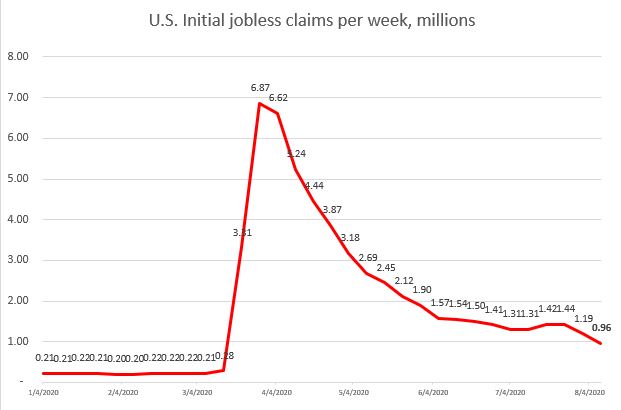

A long-awaited milestone came this week when initial unemployment claims finally fell below one million. Economists had expected much more rapid progress toward this goal, but the relentless increase in COVID-19 infections continues to restrict economic activity. The Department of Labor reported that 963,000 people filed initial unemployment claims during the week ended August 8, a decrease of 228,000 from the prior week’s upward-revised level of 1,191,000. During the week of March 28, initial jobless claims hit a peak of 6,867,000. From that peak, initial jobless claims fell for 15 weeks. July brought a setback, and claims rose again. This week’s data brings some optimism, though the number of people still unemployed is daunting. During the 20 weeks since U.S. states began to issue shelter-in-place orders, 56.3 million Americans have filed initial jobless claims. The DOL reports that 15.5 million people claim ongoing benefits.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have reached 20,956,158, with 760,318 deaths. Confirmed cases in the U.S. have risen to 5,255,234. U.S. deaths attributed to the disease have reached 167,277.

WTI crude futures prices opened at $42.33 a barrel today, up by $0.36 a barrel (0.9%) from last Friday’s open of $41.97 a barrel. Prices were strengthened midweek by across-the-board inventory draws and progress in reducing unemployment. Today, prices are weakening, but they appear to be clinging to the territory above $42 a barrel, which will ensure another weekly finish in the black. Our weekly price review covers hourly forward prices from Friday, August 7 through Friday, August 14. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

Source: Prices as reported by DTN Instant Market

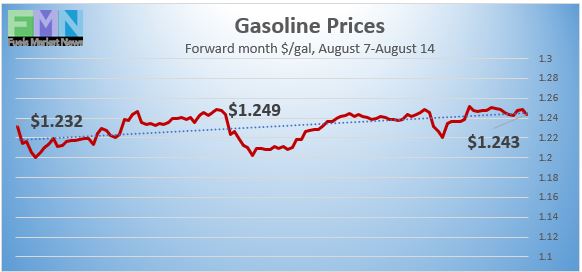

Gasoline Prices

Gasoline futures prices opened at $1.2364 per gallon today on the NYMEX, compared with $1.2315/gallon on Friday, August 7. This was a gain of 0.49 cents (0.4%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April and May. U.S. average retail prices for gasoline fell by one cent/gallon during the week ended August 10. Nine weeks ago, retail prices reclaimed the territory above $2 per gallon. Retail prices averaged $2.166/gallon at the national level. Gasoline futures prices have been stable this week, trading small gains with small losses each day. Currently, gasoline futures are trading in the range of $1.235/gallon to $1.253/gallon. The week appears to be heading for a finish slightly in the black. The latest price is $1.2419/gallon.

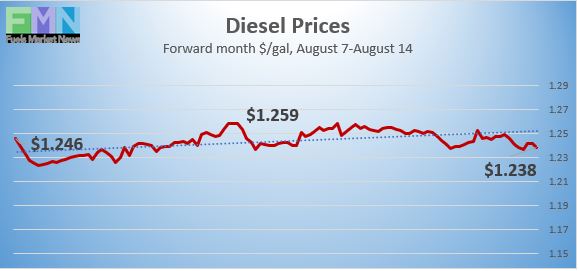

Diesel Prices

Source: Prices as reported by DTN Instant Market

Diesel opened on the NYMEX today at $1.2425/gallon, down by 0.91 cents, or 0.7%, from last Friday’s open of $1.2516/gallon. U.S. average retail prices for diesel rose by 0.4 cents per gallon during the week ended August 10 to average $2.428/gallon. Diesel prices generally have weakened this year, missing some of the price recovery see in crude and gasoline markets. Diesel futures prices rose midweek when inventory draws were announced, but prices have moved little on a weekly basis. Today, prices are heading down, but the downward price trend is slowing. Prices may finish the week in the red. Currently, diesel is trading mainly in the range of $1.232-$1.254/gallon. The latest price is $1.2429/gallon.

WTI Crude Prices

Source: Prices as reported by DTN Instant Market

WTI crude forward prices opened on the NYMEX today at $42.33 a barrel, compared with $41.97 a barrel last Friday. This was a gain of $0.36 a barrel (0.9%.) Prices have been steady this week, supported by crude and product inventory draws, and by an encouraging drop in initial unemployment claims. Over the past two weeks, WTI crude futures prices have solidified above $41 a barrel and even touched $43 a barrel, which has not happened for five months. Prices are trending down today, though if the $42 a barrel level is maintained, the week will finish with prices slightly in the black. WTI crude is trading mainly in the $41.80–$42.50 a barrel range currently. The latest price is $42.23 a barrel.

PRICE MOVERS THIS WEEK: BRIEFING

The oil complex maintained last week’s gains, with midweek reductions in inventory bolstering prices. Prices are tapering down gently today, but WTI crude oil futures appear to cleaving to the $42 a barrel level, which will afford another finish in the black this week. Gasoline and diesel prices also are declining this morning, though gasoline prices appear to be holding on for a finish in the black, while diesel prices are heading for a finish in the red. Oil prices are receiving support from the inventory drawdowns, declining unemployment, and news of an increase in retail sales. These bullish price factors are moderated by the relentless increase in coronavirus infections and the concern that recent demand growth was made possible by government stimulus payments, which now have expired. The next phase of economic stimulus remains under debate.

A long-awaited milestone came this week when initial unemployment claims finally fell below one million. Economists had expected much more rapid progress toward this goal, but the relentless increase in COVID-19 infections continues to restrict economic activity. The Department of Labor reported that 963,000 people filed initial unemployment claims during the week ended August 8, a decrease of 228,000 from the prior week’s upward-revised level of 1,191,000. During the week of March 28, initial jobless claims hit a peak of 6,867,000. From that peak, initial jobless claims fell for 15 weeks. July brought a setback, and claims rose again. This week’s data brings some optimism, though the number of people still unemployed is daunting. During the 20 weeks since U.S. states began to issue shelter-in-place orders, 56.3 million Americans have filed initial jobless claims. The DOL reports that 15.5 million people claim ongoing benefits.

A long-awaited milestone came this week when initial unemployment claims finally fell below one million. Economists had expected much more rapid progress toward this goal, but the relentless increase in COVID-19 infections continues to restrict economic activity. The Department of Labor reported that 963,000 people filed initial unemployment claims during the week ended August 8, a decrease of 228,000 from the prior week’s upward-revised level of 1,191,000. During the week of March 28, initial jobless claims hit a peak of 6,867,000. From that peak, initial jobless claims fell for 15 weeks. July brought a setback, and claims rose again. This week’s data brings some optimism, though the number of people still unemployed is daunting. During the 20 weeks since U.S. states began to issue shelter-in-place orders, 56.3 million Americans have filed initial jobless claims. The DOL reports that 15.5 million people claim ongoing benefits.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have reached 20,956,158, with 760,318 deaths. Confirmed cases in the U.S. have risen to 5,255,234. U.S. deaths attributed to the disease have reached 167,277.

Oil markets were strengthened this week when the American Petroleum Institute (API) released information on Tuesday showing across-the-board drawdowns from crude oil, gasoline and diesel inventories. According to the API, 4.401 mmbbls of crude was drawn from stockpiles. Gasoline inventories fell by 1.31 mmbbls. Diesel inventories were drawn down by 2.949 mmbbls. The API’s net drain on inventories was 8.66 mmbbls. Market analysts had predicted small drawdowns from crude and gasoline inventories plus an addition to diesel inventories.

The U.S. Energy Information Administration (EIA) published official inventory data on Wednesday. The data closely matched the API numbers. EIA statistics showed drawdowns of 4.512 mmbbls from crude oil inventories, 0.722 mmbbls from gasoline inventories, and 2.322 mmbbls from diesel inventories. The EIA net result was a significant inventory drawdown of 7.556 mmbbls. Crude oil inventories have expanded in 21 of the 31 weeks since the first week of January, sending a total of 87.12 mmbbls of crude oil into storage.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks fell to 45,582 mmbbls during the week ended June 26. However, the downward trend was reversed during the past six weeks, and Cushing stocks are back up to 53,289 mmbbls.

The pandemic has had a dramatic impact on U.S. crude production, though the downward movement has lagged the collapse in demand. Oil producing companies have struggled to stay afloat, but the second quarter brought a wave of bankruptcies. During the week ended August 7, U.S. crude production declined significantly by 0.3 mmbpd to an average of 10.7 mmbpd. According to the EIA, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd in April, 11.52 mmbpd in May, and 10.9 mmbpd in June. Production in July rose to an average of 11.04 mmbpd. Now, the decline to 10.7 mmbpd during the first week of August may signal the coming of a more serious decline, which could cause higher prices. The EIA reported that crude production in North Dakota dropped by 41.6% between December 2019 and May 2020. Production in the rest of the lower 48 states fell by 19.4% during the same period. Alaskan output fell by 16%. Production in the Federal Offshore Gulf of Mexico declined by 18.2%. In total, U.S. production fell 21.9% between December 2019 and May 2020.