OPEC+ Production Agreement is in Question

- Tension grows between OPEC supply cuts and member market share

- Agreement contributed to 30 per cent price rise

- Russian affiliation with OPEC could change traditional relationships

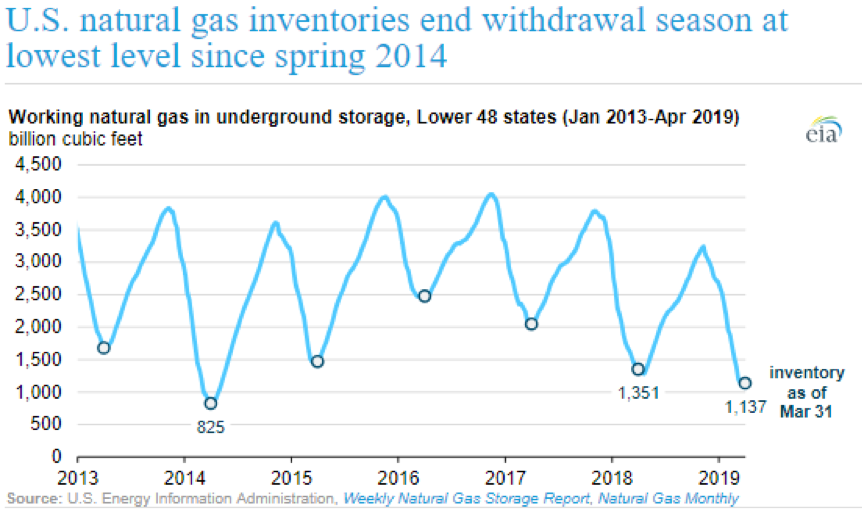

- US natural gas stocks at lowest level since 2014

The Matrix

The tension between supporting the crude oil price in global markets and competing for market share has emerged to threaten cooperation among the producers of OPEC and the “plus” — non-OPEC producers that are participating in global producer plans to limit output. Russia is the most important non-OPEC-agreement supplier.

The agreement to cut output by 1.2 million barrels daily was reached in January and runs for six months. These cuts and sanction-imposed reductions in output from Iran and Venezuela have raised prices by about 32 per cent.

Members of the new “plus” producers group are becoming restive at their loss of market share. Additional interruptions in global supply could provide the rationale for expanded output among the OPEC + group.

Russia has identified the problem: a rise in production could bring prices down to $40 per barrel. Such a situation could seriously damage the OPEC + deal. In its view, lower price would lead to

lower new investment.

The appearance of Russia on the global petroleum stage has added a new dimension to traditional oil producer relationships. As 2019 opened, OPEC was facing several challenges. Prices had fallen and some members were unwilling to reduce output. Qatar had quit the group and President Trump was pushing for lower prices.

Russia came into this chaotic situation reportedly agreeing to cut its own national output. One condition was imposed: Iran was allowed to continue producing. OPEC moved through a series of problems. These included falling prices, regime changes, internal quarreling and pressure from the United States. Russia has taken on the role of balance wheel for OPEC production – a job held by Saudi Arabia in previous years. Now, Russian and Saudi officials are to discuss formalizing the arrangements now taking place informally.

The long-standing relationship between the United States and Saudi Arabia contributed stable oil prices to global balances. With Russia in the picture, relationships are shifting. New faces are in the mix. How OPEC will react to world events is very much in question.

Supply/Demand Balances

Supply/demand data in the United States for the week ending April 12, 2019 were released by the Energy Information Administration.

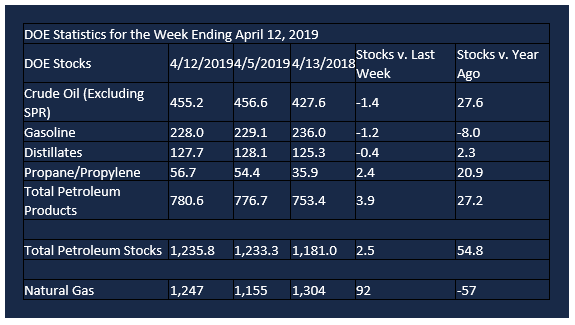

Total commercial stocks of petroleum increased 2.5 million barrels during the week ending April 12, 2019.

There were draws in stocks of gasoline, fuel ethanol, distillates, and residual fuel. There were builds in stocks of K-jet fuel, propane, and other oils.

Commercial crude oil supplies in the United States decreased 1.4 million barrels from the previous report week to 455.2 million barrels.

Crude oil supplies decreased in three of the five PAD Districts. PADD 1 (East Coast) crude oil stock fell 0.8 million barrels, PADD 2 (Midwest) stocks declined 2.4 million barrels, and PADD 5 (West Coast) stocks retreated by 0.2 million barrels. PADD 3 (Gulf Coast) stocks grew 1.5 million barrels and PADD 4 (Rockies) stocks increased 0.5 million barrels.

Cushing, Oklahoma inventories decreased 1.6 million barrels from the previous report week to 44.4 million barrels.

Domestic crude oil production was fell 100,000 barrels be day from the previous report week to 12.1 million barrels daily.

Crude oil imports averaged 5.992 million barrels per day, a daily decrease of 607,000 barrels. Exports increased 52,000 barrels daily to 2.401 million barrels per day.

Refineries used 87.7 per cent of capacity, an increase of 0.2 percentage points from the previous report week.

Crude oil inputs to refineries decreased 22,000 barrels daily; there were 16.078 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 39,000 barrels daily to 16.446 million barrels daily.

Total petroleum product inventories rose 3.9 million barrels from the previous report week.

Gasoline stocks decreased 1.2 million barrels daily from the previous report week; total stocks are 228.0 million barrels.

Demand for gasoline decreased 386,000 barrels per day to 9.420 million barrels per day.

Total product demand decreased 422,000 barrels daily to 19.893 million barrels per day.

Distillate fuel oil stocks decreased 0.4 barrels from the previous report week; distillate stocks are at 127.7 million barrels. National distillate demand was reported at 3.353 million barrels per day during the report week. This was a weekly decrease of 426,000 barrels daily.

Propane stocks increased 2.4 million barrels from the previous report week; propane stock are 56.7 million barrels. Current demand is estimated at 620,000 barrels per day, a decrease of 322,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Net injections into storage totaled 92 Bcf for the week ending April 12, compared with the five-year (2014–18) average net injections of 21 Bcf and last year’s net withdrawals of 34 Bcf during the same week. Working gas stocks totaled 1,247 Bcf, which is 414 Bcf lower than the five-year average and 57 Bcf lower than last year at this time.

Net injections into storage totaled 92 Bcf for the week ending April 12, compared with the five-year (2014–18) average net injections of 21 Bcf and last year’s net withdrawals of 34 Bcf during the same week. Working gas stocks totaled 1,247 Bcf, which is 414 Bcf lower than the five-year average and 57 Bcf lower than last year at this time.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this memo helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.