Exclusive Analysis by Dr. Nancy Yamaguchi

Oil prices dropped sharply on Thursday and are climbing back today, seeking to reclaim the territory above the $40 a barrel line. Markets retreated as the U.S. reeled from a relentless increase in COVID-19 infections. The U.S. set a new world record on July 8 with 62,147 new cases. Markets are partly mollified by news from Gilead Sciences that the drug remdesivir is reducing the risk of mortality among the sick. However, it seems a poor strategy to pin hopes on a scientific or technological breakthrough rather than working to control the rate of infection. West Texas Intermediate (WTI) crude prices are working to regain the $40 a barrel level. This may be possible if stock markets climb and carry oil prices up alongside. Crude and refined product prices are regaining lost ground, and the week appears to be headed for a finish in the black.

The Department of Labor reported that another 1.31 million people filed initial unemployment claims during the week ended July 4, down from 1.41 million the prior week. Although the numbers are trailing down, they lead to the conclusion that economic recovery is still far away. Over the 16 weeks since U.S. states began to issue shelter-in-place orders, 52.4 million Americans have filed initial jobless claims. The Fed noted nervousness among business executives and a concern that the recovery seemed to start quickly in May then stall as COVID-19 infections began to rise.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have passed the 12 million mark, and deaths have surpassed the half-a-million mark. Global cases have risen to 12,292,678, with 555,493 deaths. Confirmed cases in the U.S. have surpassed three million, rising to 3,118,168. U.S. deaths attributed to the disease have reached 133,291. Cases in the Sunbelt states are rising sharply, and some hospitals are at or nearing capacity—exactly the situation that the stay-at-home orders were intended to forestall.

Three major pipeline projects were set back this week. The natural gas Atlantic Coast Pipeline was cancelled entirely on July 5, citing legal uncertainty, ongoing delays and increasing cost uncertainty. The next day, July 6, the U.S. District Court for the District of Columbia ordered that the Dakota Access Pipeline halt operations and empty the line by August. On the same day, the U.S. Supreme Court upheld a decision to suspend construction on portions of the Keystone XL Pipeline. In the near term, the loss of this pipeline capacity may not be felt, since demand has fallen. In the longer term, however, the contraction in investment could cause prices to rise.

WTI crude futures prices opened at $39.58 a barrel today, down by 20 cents a barrel (0.5%) from last Thursday’s open of $39.78 a barrel. Prices today are working to recoup yesterday’s losses, and WTI is trying to regain the $40 a barrel level. This may be possible if stock markets rise and pull oil prices up alongside. Otherwise, oil prices may end the week flat or slightly in the red. Our weekly price review covers hourly forward prices from Friday, July 3 through Friday, July 10. Trading hours on July 3 were curtailed in observance of the Independence Day holiday. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

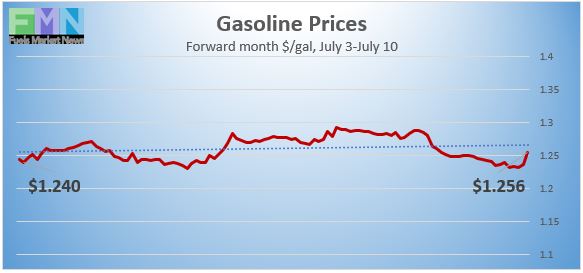

Gasoline Prices

Gasoline futures prices opened at $1.2484 per gallon today on the NYMEX, compared with $1.2222/gallon on Thursday, July 2. This was an increase of 2.62 cents (2.1%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April and May. U.S. average retail prices for gasoline rose slightly by 0.3 cents/gallon during the week ended July 6. Four weeks ago, retail prices reclaimed the territory above $2 per gallon. Retail prices averaged $2.177/gallon at the national level. Gasoline futures prices are rebounding today, trading in the range of $1.23/gallon to $1.27/gallon. The week appears to be rallying for a finish in the black. The latest price is $1.2615/gallon.

Gasoline futures prices opened at $1.2484 per gallon today on the NYMEX, compared with $1.2222/gallon on Thursday, July 2. This was an increase of 2.62 cents (2.1%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April and May. U.S. average retail prices for gasoline rose slightly by 0.3 cents/gallon during the week ended July 6. Four weeks ago, retail prices reclaimed the territory above $2 per gallon. Retail prices averaged $2.177/gallon at the national level. Gasoline futures prices are rebounding today, trading in the range of $1.23/gallon to $1.27/gallon. The week appears to be rallying for a finish in the black. The latest price is $1.2615/gallon.

Source: Prices as reported by DTN Instant Market

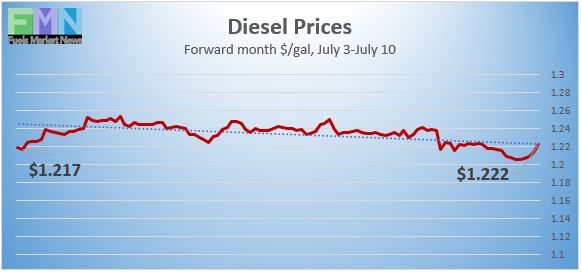

Diesel Prices

Diesel opened on the NYMEX today at $1.2239/gallon, a gain of 2.27 cents, or 1.9%, from last Thursday’s open of $1.2012/gallon. (Markets were closed on Friday in observance of the Independence Day holiday.) U.S. average retail prices for diesel rose by 0.7 cents per gallon during the week ended July 6 to average $2.437/gallon. Diesel prices have weakened more or less steadily this year, missing some of the price recovery see in crude and gasoline markets. Diesel futures prices today are bouncing back after yesterday’s fall, and the week appears to be headed for a finish in the black. Currently, diesel is trading in the range of $1.20-$1.231/gallon. The latest price is $1.2257/gallon.

Diesel opened on the NYMEX today at $1.2239/gallon, a gain of 2.27 cents, or 1.9%, from last Thursday’s open of $1.2012/gallon. (Markets were closed on Friday in observance of the Independence Day holiday.) U.S. average retail prices for diesel rose by 0.7 cents per gallon during the week ended July 6 to average $2.437/gallon. Diesel prices have weakened more or less steadily this year, missing some of the price recovery see in crude and gasoline markets. Diesel futures prices today are bouncing back after yesterday’s fall, and the week appears to be headed for a finish in the black. Currently, diesel is trading in the range of $1.20-$1.231/gallon. The latest price is $1.2257/gallon.

Source: Prices as reported by DTN Instant Market

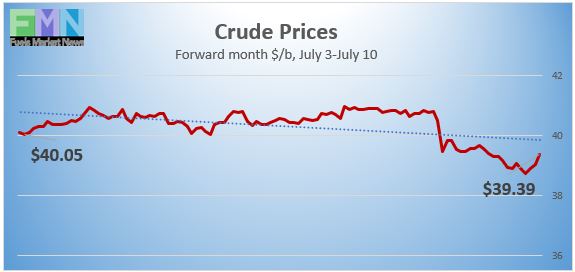

WTI Crude Prices

WTI crude forward prices opened on the NYMEX today at $39.58 a barrel, compared with $39.78 a barrel last Thursday (markets were closed on Friday in observance of the Independence Day holiday.) This was a small decrease of $0.20 a barrel (0.5%.) Prices had opened above the $40 a barrel level Monday through Thursday this week, but they dropped by close of market on Thursday. The increase of COVID-19 infections and fatalities caused a pullback. Today, markets are working to recoup yesterday’s loss, and oil prices may achieve a finish in the black. WTI prices are trading in the $38.50–$40 a barrel range currently. The latest price is $39.71 a barrel.

WTI crude forward prices opened on the NYMEX today at $39.58 a barrel, compared with $39.78 a barrel last Thursday (markets were closed on Friday in observance of the Independence Day holiday.) This was a small decrease of $0.20 a barrel (0.5%.) Prices had opened above the $40 a barrel level Monday through Thursday this week, but they dropped by close of market on Thursday. The increase of COVID-19 infections and fatalities caused a pullback. Today, markets are working to recoup yesterday’s loss, and oil prices may achieve a finish in the black. WTI prices are trading in the $38.50–$40 a barrel range currently. The latest price is $39.71 a barrel.

Source: Prices as reported by DTN Instant Market

PRICE MOVERS THIS WEEK: BRIEFING

WTI crude oil prices dropped sharply on Thursday and are climbing back today, seeking to reclaim the territory above the $40 a barrel line. Markets retreated as the U.S. reeled from a relentless increase in COVID-19 infections. The first eight days of July have had four record-setting days in terms of new cases, with July 8’s record at 62,147 new cases. This was the largest daily total ever reported in any country worldwide during the pandemic. Florida reported a record rise in hospitalizations. Markets are partly mollified by news from Gilead Sciences that the drug remdesivir is reducing the risk of mortality among the sick. West Texas Intermediate (WTI) crude prices are working to regain the $40 a barrel level. This may be possible if stock markets climb and carry oil prices up alongside. Crude and refined product prices are regaining lost ground, and the week may achieve a finish in the black.

The Department of Labor reported that another 1.31 million people filed initial unemployment claims during the week ended July 4, down from 1.41 million the prior week. Although the numbers are trailing down, they lead to the conclusion that economic recovery is still far away. Over the 16 weeks since U.S. states began to issue shelter-in-place orders, 52.4 million Americans have filed initial jobless claims. The Fed noted nervousness among business executives and a concern that the recovery seemed to start quickly in May then stall as COVID-19 infections began to rise.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have passed the 12 million mark, and deaths have surpassed the half-a-million mark. Global cases have risen to 12,292,678, with 555,493 deaths. Confirmed cases in the U.S. have surpassed three million, rising to 3,118,168. U.S. deaths attributed to the disease have reached 133,291. By now, so many U.S. states are reporting increases in COVID-19 infections that listing them is pointless. There are few states that are clearly in the green, most of which are located in the Northeast U.S. Cases in the Sunbelt states are rising sharply, and some hospitals are at or nearing capacity—exactly the situation that the stay-at-home orders were intended to forestall.

Three major pipeline projects were set back this week. The natural gas Atlantic Coast Pipeline was cancelled entirely on July 5, citing legal uncertainty, ongoing delays, and increasing cost uncertainty. The next day, July 6, the U.S. District Court for the District of Columbia ordered that the Dakota Access Pipeline halt operations and empty the line by August. On the same day, the U.S. Supreme Court upheld a decision to suspend construction on portions of the Keystone XL Pipeline. Energy Transfer is defying the court order and continuing to schedule shipments in the Dakota Access pipeline, stating in its appeal that it would not be physically possible to empty the line in such a short period of time. During the recent Shale Boom years, companies have aggressively worked to expand transport infrastructure, but numerous communities along the pathways have protested. In the near term, the loss of this pipeline capacity may not be felt, since demand has fallen. In the longer term, however, the contraction in investment could cause prices to rise.

Oil prices were unchanged Tuesday when the American Petroleum Institute (API) released information showing an addition of 2.05 mmbbls to crude oil stockpiles, counteracted by drawdowns of 1.83 mmbbls from gasoline inventories and 0.847 mmbbls from diesel inventories. The API’s net inventory draw was 0.627 mmbbls. Market analysts had predicted across-the-board drawdowns from inventory.

Official inventory data were more bearish than the API numbers. Oil prices weakened on Wednesday when U.S. Energy Information Administration (EIA) official statistics showed a larger addition to crude oil stockpiles, plus a significant addition to diesel inventories. Gasoline inventories fell. The EIA reported a significant addition of 5.654 mmbbls to crude stockpiles, plus an addition to diesel inventories of 3.135 mmbbls. Gasoline stocks fell by 4.839 mmbbls. The EIA net result was an inventory build of 3.95 mmbbls. Crude oil inventories have expanded in 20 of the 26 weeks since the first week of January, sending a total of 112.22 mmbbls of crude oil into storage.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks fell to 45,582 mmbbls during the week ended June 26, but the downward trend was reversed during the week ended July 3, ticking back up to 47,788 mmbbls. Some surplus crude is being stored in the National Strategic Petroleum Reserve (SPR). The EIA reports that SPR additions were made in the weeks ended April 24 (1.150 mmbbls), May 1 (1.716 mmbbls), May 8 (1.933 mmbbls), May 15 (1.882 mmbbls), May 22 (2.111 mmbbls), May 29 (4.02 mmbbls), June 5 (2.22 mmbbls), June 12 (1.731 mmbbls), June 19 (1.991 mmbbl), June 26 (1.692 mmbbls) and July 3 (0.61 mmbbls). Current SPR stocks are 656.023 mmbbls.

U.S. crude production has been flat. The EIA reported that U.S. crude production during the week ended July 3 averaged 11 mmbpd, unchanged from the two prior weeks. According to the EIA’s weekly data series, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd in April, 11.52 mmbpd in May and 10.9 mmbpd in June. The EIA has revised downward its forecast of 2020 production, cutting it to 11.56 mmbpd. However, the forecast of demand has been cut as well, leaving a supply overhang.