MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

December 20, 2019: Crude oil prices crept up steadily this week, hitting and holding above $60/b, climbing to $61/b, and backing off slightly this morning. These are the highest prices since the brief spike in mid-September caused by drone attacks on Saudi Arabian oil facilities. Last week, markets rose when the news came out that U.S. and China had reached a “phase-one accord” in the trade war. December 15 had been the date for additional U.S. tariffs on $160 billion in consumer goods, and these tariffs now will be canceled. The agreement in principle called for the U.S. to scale back the existing $375 billion in tariffs by half, while China agreed to purchase $50 billion in U.S. agricultural goods and energy in 2020. Oil prices strengthened, then were reinforced by a stellar U.S. Jobs Report. This week, the House signed a renegotiation of the U.S.-Mexico-Canada trade agreement, with broad bi-partisan support just one day after the House voted to impeach President Donald Trump. Senate Republicans repeatedly have said they will vote to acquit the president. Many investors have adopted a business-as-usual stance. The price strength is continuing this week. Oil prices appear to be headed for another finish in the black.

WTI futures crude prices opened on Friday, December 13, at $59.39/b, and prices rose to an open of $61.11/b today, up by $1.75/b. WTI futures prices regained the $60/b level on Monday, and prices climbed slowly but steadily every day this week, attaining the $61/b level on Thursday. WTI futures prices had not been steadily above $60/b since mid-July. This week should finish with oil prices in the black. Gasoline and diesel prices followed crude up, and prices are currently in a holding pattern. Our weekly price review covers hourly forward prices from Friday, December 13, through Friday, December 20. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.6325/gallon on Friday, December 13, and prices opened at $1.7061/gallon on Friday, December 20. This was an increase of 7.36 cents (4.5%.) U.S. average retail prices declined by 2.5 cents/gallon during the week ended December 16th. The week appears to be headed for a finish in the black. Trades are occurring mainly in the range of $1.70-$1.73/gallon. The latest price is $1.7169/gallon.

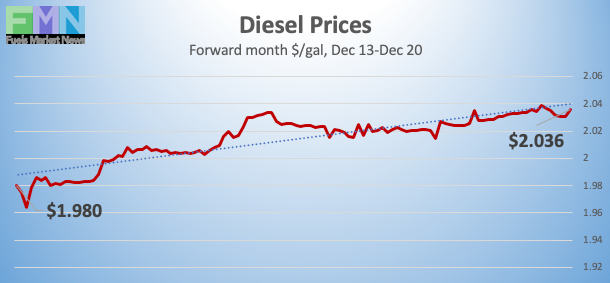

DIESEL PRICES

Diesel opened on the NYMEX at $1.9553/gallon on Friday, December 13 and opened on Friday, December 20 at $2.0307/gallon, up by 7.54 cents (3.9%.) U.S. average retail prices for diesel eased by 0.3 cents/gallon during the week ended December 16th. Diesel futures prices rose steadily on Monday through Wednesday, ebbed on Thursday, and resumed climbing today. The week appears to be heading for a finish in the black. Contracts currently are trading in the $2.02-$2.04/gallon range. The latest price is $2.0347/gallon.

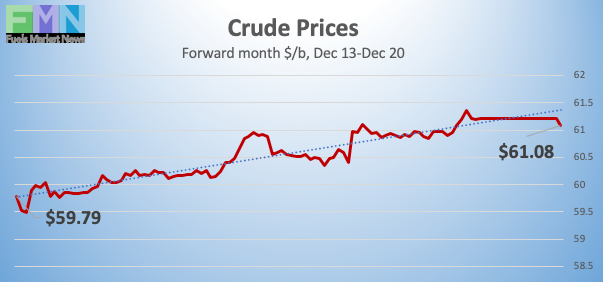

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday, December 13 at $59.36/b. Prices climbed steadily to an open of $61.11/b today, up by $1.75/b (2.9%.) During the week, prices slackened briefly when U.S. supplies rose, but official statistics put prices bac on a more optimistic path. Market continue to strengthen based on the phase-one agreement in the U.S.-China trade war, which in principle will cancel the next set of tariffs that the U.S. had scheduled to take effect on December 15th, roll back existing tariffs by 50%, and increase Chinese purchases of U.S. agricultural and energy products in 2020. Currently, WTI futures prices have retreated from the $61/b level but are holding above $60/b. WTI crude is trading mainly in the range of $60.50/b-$61.25/b. The latest price is $60.62/b.

PRICE MOVERS THIS WEEK : BRIEFING

Crude oil prices crept up daily this week, reaching and holding the $60/b level then pressing on to $61/b before retreating this morning. Last week, markets surged when the news came out that U.S. and China had reached a “phase-one accord” in the trade war. December 15 had been the date for additional U.S. tariffs on $160 billion in consumer goods, and these tariffs now will be canceled. The agreement in principle called for the U.S. to scale back an existing set of tariffs by half, while China agreed to purchase $50 billion in U.S. agricultural goods and energy in 2020. Oil prices strengthened, and the price strength is continuing this week. Oil prices appear to be headed for another finish in the black.

Markets are expected to be unpredictable today, when options and futures on stocks and indexes all expire at the same time. This may cause considerable volatility, as some traders take profits while others assume that upward trends will continue. Countering this, there is often a holiday lull in trading. On Thursday, the Dow Jones Industrial Average set a new record-high of 28,376.96. The Dow broke 28,000 in mid-November, and it has been hovering in this neighborhood since then. Optimism continues in the U.S. economy, most recently bolstered by last month’s strong Jobs Report, the phase-one agreement in the U.S.-China trade war, and the successful approval of the renegotiated U.S.-Mexico-Canada trade agreement. This measure passed overwhelmingly in the Democratic-led House just one day after the House voted to impeach President Donald Trump. Many investors have continued to focus on positive economic factors, since although impeachment stains the president, the Senate’s oft-stated determination to acquit him leaves markets assuming business-as-usual.

Oil prices flattened briefly midweek based on news of increased supply. On Tuesday, the American Petroleum Institute (API) reported, for the second week in a row, across-the-board additions to U.S. oil inventories: 4.71 million barrels (mmbbls) to crude stocks, 5.6 mmbbls to gasoline inventories and 3.7 mmbbls to diesel stockpiles. Industry experts had anticipated a crude stock drawdown, a gasoline stock build, and no change in diesel stockpiles. The API’s net inventory build was a massive 14.01 mmbbls. This slowed the upward trend in prices.

Prices resumed their upward trend when the EIA released far less bearish official statistics on Wednesday. Instead of a 4.71 mmbbl-crude stock build, there was a 1.085-mmbbl drawdown. Although this was more than outweighed by additions of 2.529 mmbbls of gasoline and 1.509 mmbbls of diesel, it showed a more balanced picture. The net result was an inventory build of 2.953 mmbbls, far less than the API data reported.

The EIA also reported that U.S. crude production remained stable at 12.8 mmbpd during the week ended December 13th. Production had hit a new record-high 12.9 mmbpd during the second half of November. Approximately 1.1 mmbpd has been added to U.S. supply this year. This has been accomplished despite a steady downward trend in active oil and gas rigs. The Baker Hughes rig count was unchanged during the week ended December 13th. So far this year, 276 rigs have exited the field. Nonetheless, the U.S. Energy Information Administration announced that the U.S. is on track to become a net exporter of petroleum in 2020.