MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

January 10, 2020: Oil prices retreated this week, based on ratcheting down of U.S.-Iran hostilities and increased oil supplies. Last week, oil prices surged when U.S. airstrikes in Iraq killed five people, including the Iranian general who commanded the Revolutionary Guards Corps. The ensuing week brought de-escalation, and prices began to subside. Today’s twist to the story is that Canada and the U.S. now believe that the Ukrainian jet crash near Tehran was caused by two Iranian missiles. Iran denies the attack, and officials have invited an international investigation with access to the airliner’s black box. It appears possible that it was an accident and not an act of terrorism. WTI crude futures prices retreated below $60/b and have dipped below $59/b this morning. Prices currently are in the $58.95-$59.75/b range. The week appears to be headed for a finish in the red.

The Bureau of Labor Statistics has just released the Employment Situation Report for December 2019. Total nonfarm payroll employment rose by 145,000 in December. Economists had forecast that jobs formation would be 160,000, so the official statistics will be viewed as slightly disappointing. Nonetheless, the unemployment rate was unchanged at the already-low 3.5%.

WTI futures crude prices opened on Friday, January 3, at $61.18/b, and prices eased to an open of $59.61/b today, down by $1.57/b. WTI futures prices were volatile this week, ranging from a high of $65.65 on Wednesday to a low of $58.66/b on Thursday (a range of nearly $7/b,) but prices generally trended down, falling below the $60/b level, and threatening to drop below $59/b as well. Gasoline and diesel prices followed crude, surging midweek then collapsing. Our weekly price review covers hourly forward prices from Friday, January 3rd, through Friday, January 10th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

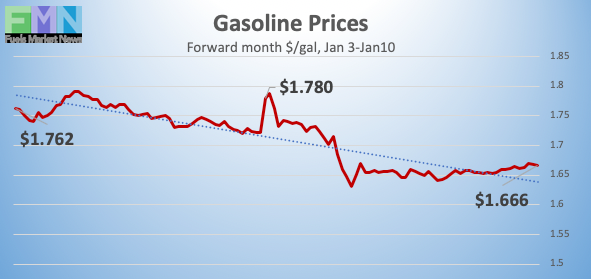

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.7069/gallon on Friday, January 3, and prices fell to open at $1.6579/gallon on Friday, January 10. This was a drop of 4.9 cents (2.9%.) Gasoline futures prices were volatile this week, ranging from a low of $1.6289/gallon to a high of $1.8011/gallon on Wednesday, a huge range of 17.22 cents. On Wednesday, the EIA reported a massive 9.137-mmbbl addition to gasoline stocks. The addition to gasoline stocks was the largest in four years, and it was the fourth-largest addition since the EIA started reporting the data in 1990. U.S. average retail prices rose by 0.7 cents/gallon during the week ended January 6th. Gasoline prices currently are stabilizing. Trades are occurring mainly in the range of $1.65-$1.67/gallon. The latest price is $1.6587/gallon.

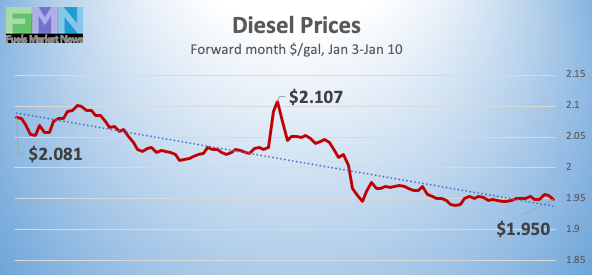

DIESEL PRICES

Diesel opened on the NYMEX at $2.026/gallon on Friday, January 3, and opened on Friday, January 10, at $1.9522/gallon, down sharply by 7.38 cents (3.6%.) U.S. average retail prices for diesel rose by 1.0 cent/gallon during the week ended January 6th. Diesel futures prices were volatile this week, ranging from a low of $1.9282/gallon on Thursday to a high of $2.1195/gallon on Wednesday, a huge range of 19.13 cents. The week appears to be heading for a finish in the red. Prices are currently stabilizing, with contracts trading in the $1.93-$1.96/gallon range. The latest price is $1.9463/gallon.

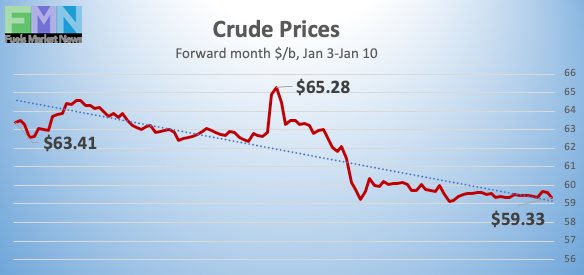

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday, January 3, at $61.18/b. Prices opened at $59.61/b today, a drop of $1.57 (2.6%.) WTI futures prices were volatile this week, ranging from a high of $65.65/b on Wednesday to a low of $58.66/b on Thursday (a range of nearly $7/b.) Prices are trending down, falling first below the $60/b level, and currently dipping below the $59/b level as well. During the week, prices were also pressured by major additions to U.S. crude oil and refined product inventories. The week is heading for a finish in the red. WTI futures prices currently are in the range of $58.95-$59.75/b. The latest price is $59.16/b.

PRICE MOVERS THIS WEEK : BRIEFING

Oil prices eased from last week’s highs, with markets soothed but rightly wary in the aftermath of U.S. airstrikes in Iraq and Iranian response. U.S. President Donald Trump stated on Thursday that killing Major General Qassem Soleimani was justified, saying “We did it because they were looking to blow up our embassy.” In retaliation, Iran fired over a dozen ballistic missiles at two military bases in Iraq where U.S. forces were stationed, but no casualties were reported. The Iranian missile attack response appeared moderate. It gave both sides an opportunity to back away from escalation. However, Canadian Prime Minister Justin Trudeau accused Iran of shooting down the Ukrainian plane that crashed on Wednesday after taking off from Tehran. The crash killed all 176 people on board, including at least 63 Canadians. If this was found to be an act of terrorism, it would ruin Iran’s efforts to win international support in the conflict. Iranian investigators said they would be willing to provide the airliner’s black box to international investigators, and Iran has invited investigators from the Boeing Corporation, Canada, Ukraine, and the U.S. It appears possible that the aircraft downing was accidental.

The Bureau of Labor Statistics has just released the Employment Situation Report for December 2019. Total nonfarm payroll employment rose by 145,000 in December. Economists had forecast that jobs formation would be 160,000, so the official statistics are slightly disappointing. Nonetheless, the unemployment rate was unchanged at an already-low level of 3.5%.

U.S. oil inventories rose this week, further suppressing prices. The American Petroleum Institute (API) reported a 5.95-million barrel (mmbbl) drawdown from U.S. crude oil inventories. This was outweighed by an addition of 6.7 mmbbls to gasoline inventories and an addition of 6.4 mmbbls to diesel inventories. Industry experts also had anticipated a crude stock drawdown more than counterbalanced by additions to gasoline and diesel stocks. The API’s net inventory build was a significant 7.15 mmbbls.

The U.S. Energy Information Administration (EIA) released an even more bearish set of official statistics, showing across-the-board additions to inventories: a 1.164-mmbbl crude stock build, a massive 9.137-mmbbl addition to gasoline stocks, and a significant 5.33-mmbbl addition to diesel inventories. The addition to gasoline stocks was the largest in four years, and it was the fourth-largest addition in the three decades since the EIA started reporting the data in 1990. The net result was a huge inventory build of 15.631 mmbbls.

The EIA also reported that U.S. crude production remained at its historic high level of 12.9 mmbpd during the week ended January 3rd. Production hit this record during the second half of November, and it has bounced between 12.8 and 12.9 mmbpd since then. Approximately 1.2 mmbpd was added to U.S. crude oil output in 2019.