Principal contributor: Naser Ameen

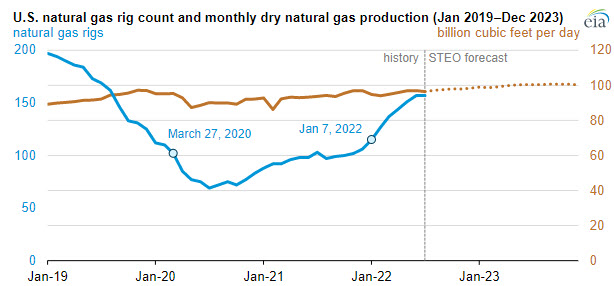

U.S. natural gas producers are operating more drilling rigs now than at the beginning of the COVID-19 pandemic in early 2020. Before the pandemic, the number of operating rigs in the United States had generally been declining. On January 31, 2020—when the U.S. Department of Health and Human Services first declared a public health emergency related to COVID-19—the Baker Hughes Company reported that 112 natural gas rigs were operating in the United States. The number of natural gas-directed rigs continued to fall in the first half of 2020, reaching a low of 68 rigs on July 24, 2020, the fewest in Baker Hughes’s historical data, dating back to 1987. Since then, the natural gas rig count has generally been increasing, returning to pre-pandemic levels in January 2022. On September 9, Baker Hughes reported that 166 natural gas rigs were operating in the United States, 54 more than at the outset of the pandemic in the United States.

As natural gas drilling increases in the United States, we expect that production will grow as well. Our September Short-Term Energy Outlook (STEO) estimates that dry natural gas production averaged 97.6 billion cubic feet per day (Bcf/d) in the United States during August 2022. We expect U.S. dry natural gas production to increase throughout the STEO forecast period (2022–23), averaging 100.5 Bcf/d during December 2023.

Our Drilling Productivity Report (DPR) measures historical natural gas production in selected onshore regions, including the Appalachia, Haynesville, and Permian regions, where most of the natural gas activity is concentrated. To develop estimates of overall changes in production for each region, the DPR uses recent rig activity data, but it also explicitly considers:

- Recent information on rig productivity

- Average oil and natural gas production rates from new wells during their first full month of operation

- Estimated changes in production from existing wells

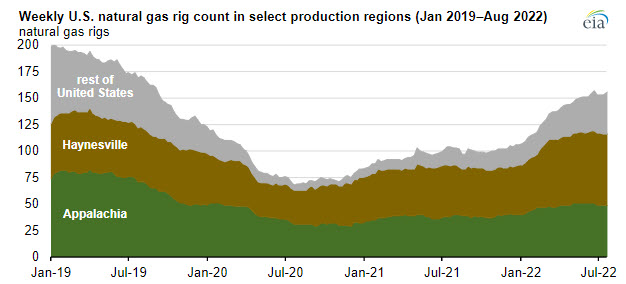

Most of the growth in natural gas-directed rigs in the United States has been in the Haynesville region, which spans Texas and New Mexico. The rig count in Haynesville increased by more than 50% between January 2020 and August 2022. Despite relatively high natural gas prices, drilling in Haynesville remains economical. Haynesville’s well productivity and proximity to the U.S. Gulf Coast liquefied natural gas (LNG) export terminals and to major industrial natural gas consumers draws operators to the region.

Rig activity in the Appalachia region of Pennsylvania and West Virginia is close to returning to the 51 operating rigs reported as of January 31, 2020; it stood at 48 natural gas-directed rigs as of July 29, 2022. Improved well productivity, pipeline buildouts, and increased takeaway capacity have aided the long-term trend of production growth in Appalachia over the past 10 years; however, regional transportation capacity limits may have begun to constrain drilling activity in the region.

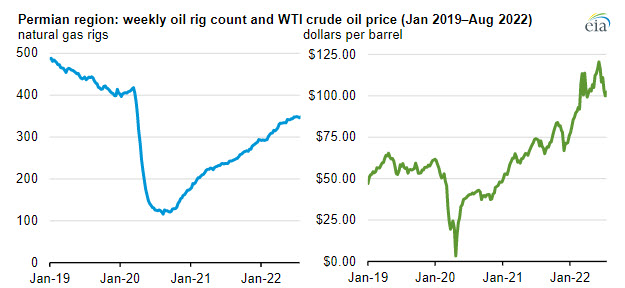

Note: WTI=West Texas Intermediate

In the Permian region, spanning West Texas and New Mexico, most natural gas production is associated gas produced from oil wells. Permian producers respond to fluctuations in the crude oil price when planning their rig deployment. Crude oil prices and oil-directed rigs both declined in 2020 amid peak COVID-19 mitigation efforts. In 2021, the West Texas Intermediate (WTI) crude oil price increased steadily, averaging $68 per barrel (b) for the year, compared with $39/b in 2020. WTI prices continued to increase in 2022, averaging more than $100 per barrel in the first half of the year. The number of oil-directed rigs in the region has also been generally rising since the 2020 lows, but the rig count is still 15% below the January 31, 2020, pre-pandemic count of 406 rigs.