Excerpted from This Week in Petroleum

Release Date: September 8, 2022

In our September 2022 Short-Term Energy Outlook (STEO), we forecast that East Coast (PADD 1) gasoline inventories will increase from their lows in July and August 2022 (Figure 1). August East Coast gasoline inventories were an estimated 51.8 million barrels, a slight increase from our estimate for July 2022 of 50.7 million barrels. Following forecast builds in the fourth quarter of 2022 (4Q22), we expect East Coast gasoline inventories to be higher in 2023. You can find our regional gasoline inventories in Table 4c of the STEO and in the STEO data browser.

In July, East Coast gasoline inventories were the lowest since October 2014 due to a couple of factors affecting supply. Russia’s full-scale invasion of Ukraine has disrupted global petroleum product trade and increased competition for fuel supplies in the Atlantic Basin, contributing to less gasoline imported into the East Coast this year. Average motor gasoline imports in the first half of 2022 (1H22) decreased 24% compared with 1H21. In addition, petroleum production capacity on the East Coast has decreased since the 2019 closure of the Philadelphia Energy Solutions refinery and the idling of the Come-by-Chance refinery in Newfoundland, Canada, in 2020. Although product movement from the U.S. Gulf Coast to the East Coast has been robust, further increases in these shipments are limited by transportation constraints.

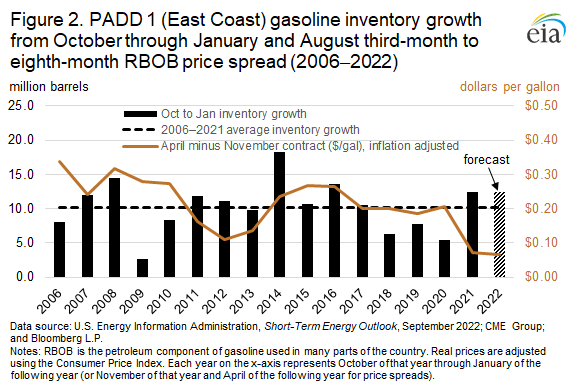

We forecast that East Coast gasoline inventories will build by 12.5 million barrels between October 2022 and January 2023, more than the 10.2 million barrel seasonal average build in the 16 years starting with the period from October 2006 to January 2007 (Figure 2). Gasoline inventories typically build during these months for a variety of reasons. One is that less gasoline is consumed in the fall and winter than in the summer when drivers tend to travel more. In addition, futures prices for RBOB (the petroleum component of gasoline used in many parts of the country) generally exhibit higher prices for summer-month delivery than for winter-month delivery. This seasonal structure in RBOB futures prices encourages market participants to build inventory in the winter, ahead of the high-demand summer months. For example, in August trading from 2006 to 2021, the premium for April delivery of RBOB compared with November delivery ranged from $0.34 per gallon (gal) in 2006 to $0.07/gal in 2021 and 2022 in inflation-adjusted prices.

Another explanation for the higher-than-average build forecast for 4Q22 is our expectation that demand will be 0.3% less than in 4Q21. After reaching a peak of 66 million barrels in January 2023, we forecast East Coast gasoline inventories will remain at around 60 million barrels until June 2023. We forecast inventories will decrease to around 55 million barrels during the peak driving demand season in July and August 2023, and then we expect inventories to increase back above 60 million barrels by the end of 2023.

Turning to distillate inventories, for which we forecast only U.S.-level rather than regional data, we anticipate inventories will remain low through 2023. U.S distillate inventories have been below their five-year (2017–2021) range all year, and August inventories were the lowest for that month since 2000. Distillate inventories typically build in the summer months ahead of the harvest and winter heating season, although distillate’s seasonal patterns have changed in recent years. In 2022, we estimate distillate inventories declined from the end of March to the end of August, the second consecutive year in which distillate inventories declined during these months. On average between 2000 and 2020, inventories built by 16 million barrels during these months. We forecast U.S. distillate inventories will reach their lowest volumes in October 2022 at 107.3 million barrels and that they will remain at similar levels in March and April of 2023 before increasing to around 119 million barrels in 2H23 (Figure 3).

Distillate inventories have been low globally in 2022 as Western sanctions against Russia’s petroleum product exports have decreased supplies circulating among major trading hubs. Like gasoline supply, distillate supply has also been affected by less production capacity in the United States. Unlike gasoline supply where inventory concerns are concentrated on the East Coast, however, the low distillate inventories are present across all regions, according to Weekly Petroleum Status Report data. Overall, we expect U.S. distillate inventories to be slightly higher in 2023 than in 2022 but to remain below their five-year range.