Oil Markets Turn Bearish

- Bullish price expectations run into trouble

- American oil production surprises to the upside

- Global producers outperform plan

- Technical charts support bear case

- Natural gas prices seek a new equilibrium

The Matrix

Oil markets were expected to move higher until early October. Then, market observers pointed to a slowdown in American oil production. Traders expected supplies from Iran to fall sharply as U.S. sanctions were to be imposed as of early November. OPEC and Russia were likely to cut output in support of price.

Increases in crude oil production were seen as substituting for failing output in several traditional producing areas rather than adding to global supply. Venezuela in particular was experiencing significant losses as part of the country’s general economic failure. Elsewhere, Libyan exports had stalled. Nigeria also faced

constraints on output. Iraqi shortfalls cut supply too.

About six weeks ago, the outlook started to shift to a more bearish position.

After a full year, Iraq re-introduced Kirkuk exports to global balances. This reflected the end of a dispute between the central Iraqi government and the Kurdish semi-autonomous area. Initial output came in around 50-60,000 barrels daily. This was well below peak output of 300,000 barrels per day last year, but was expected to reach 100,000 barrels daily.

The United States reported a dramatic increase in output. After stalling around eleven million barrels daily, production jumped to 11.4 million daily barrels and in the following week, added still another 100,000 barrels per day.

At the same time, Russia and several OPEC members reportedly were supplying oil at higher rates than expected. Other OPEC members adding to stocks were Kuwait, UAE and Iraq.

The Iranian sanctions became operative, but their power was undercut by a series of waivers. China and India are major off-takers from Iran. The U.S. expressed concern that tight supply to these countries would raise prices, contravening our interest in lower costs of materials.

Technical analysis supports this bearish turn of events. One analyst noted that “a study on the long-term charts from 2008 suggests a conservative 15 per cent loss in a few months and aggressive near 60 per cent drop over the next one or two years.” Put more plainly, the current downtrend could reach $43.75 on WTI. “Wave theory suggests a return of the price to $26.05.” This level was last seen in 2016

Supply/Demand Balances

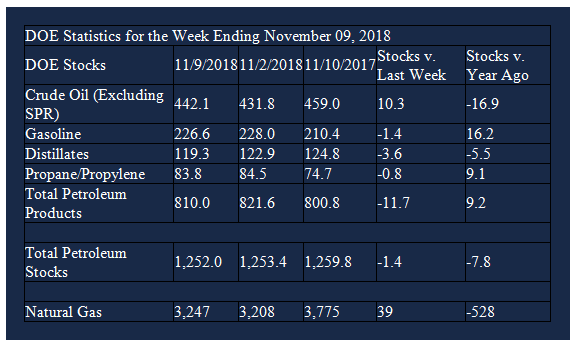

Supply/demand data in the United States for the week ending November 9, 2018 were released by the Energy Information Administration.

Total commercial stocks of petroleum decreased 1.4 million barrels during the week ending November 9, 2018.

There were draws in stocks of gasoline, K-jet fuel, distillates, residual fuel, propane, and other oils. There was a build in stocks of fuel ethanol.

Commercial crude oil supplies in the United States increased to 442.1 million barrels, a build of 10.3 million barrels.

Crude oil supplies increased in four of the five PAD Districts. PAD District 1 (East Coast) stocks increased 2.4 million barrels, PADD 2 (Midwest) stocks grew 2.2 million barrels, PADD 3 (Gulf Coast) stocks expanded 5.3 million barrels, and PADD 4 (Rockies) stocks were up 0.6 million barrels. PADD 5 (West Coast) stocks declined 0.2 million barrels.

Cushing, Oklahoma inventories increased 1.2 million barrels from the previous report week to 35.5 million barrels.

Domestic crude oil production was up 100,000 barrels per day from the previous report week to 11.7 million barrels per day.

Crude oil imports averaged 7.452 million barrels per day, a daily decrease of 87,000 barrels per day. Exports fell 355,000 barrels daily to 2.050 million barrels per day.

Refineries used 90.1 per cent of capacity, an increase of 0.1 percentage points from the previous report week.

Crude oil inputs to refineries increased 24,000 barrels daily; there were 16.432 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, increased 25,000 barrels daily to 16.765 million barrels daily.

Total petroleum product inventories fell 11.7 million barrels from the previous report week.

Gasoline stocks decreased 1.4 million barrels from the previous report week; total stocks are 226.6 million barrels.

Demand for gasoline increased 92,000 barrels per day to 9.192 million barrels per day.

Total product demand increased 2.001 million barrels daily to 22.387 million barrels per day.

Distillate fuel oil stocks decreased 3.6 million barrels from the previous report week; distillate stocks are 119.3 million barrels. National distillate demand was reported at 4.633 million barrels per day during the report week. This was a weekly increase of 315,000 barrels daily.

Propane stocks decreased 0.8 million barrels from the previous report week; propane stock are 83.8 million barrels. Current demand is estimated at 1.547 million barrels per day, an increase of 640,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Net injections of natural gas were higher than the five-year average. Net injections into storage totaled 39 Bcf for the week ending November 9, compared with the five-year (2013-17) average net injections of 19 Bcf and last year’s net withdrawals of 13 Bcf during the same week. Working natural gas stocks totaled 3,247 Bcf, which is 601 Bcf lower than the five-year average and 528 Bcf lower than last year at this time.

Working gas stocks’ deficit to the five-year average and deficit to the bottom of the five-year range decreased. In the Lower 48 states, total working gas stocks were 359 Bcf lower than the five-year minimum. Every storage region is currently lower than the bottom of the five-year range.

Natural gas futures pricing stood in stark contrast with petroleum liquids. Gas prices vaulted higher, moving from a low of 3.735 on Monday, November 12 to $4.929 by Wednesday, November 14. This reflected buying previously deferred because of strong bearish attitudes among traders. Expectations of colder weather came to bear on the market, helped along by recognition that regional distribution infrastructure would be seriously tested by strong demand. Natural gas prices returned to $3.90 and have since been seeking a new equilibrium. The powerful reaction to a rather modest weather forecast reminds us, however, how rapidly and intensely futures markets can respond to various stimuli. Complacency can incur a heavy cost.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright © 2018 Powerhouse, All rights reserved.