In Part 1, found here, Dr. Nancy Yamaguchi described why marketers and retailers should follow crude prices, the history of the WTI-Brent price differential, crude quality and the changing crude slate. She now explores how the regional supply-demand balance comes into play, as well as the various impacts of the shale boom in the U.S. and the loosening of U.S. export controls.

The Change in Supply-Demand Balance, North America vs Europe/Eurasia

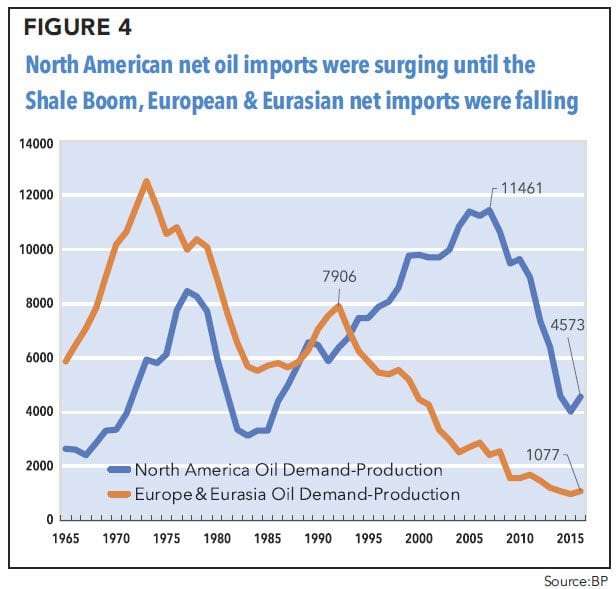

Another key determinant of the relative value of WTI crude versus Brent crude is the regional supply-demand balance. North America is a major net importer of oil, and the world expected its net import requirements to continue to grow. The accompanying figure uses British Petroleum’s (BP’s) data on oil demand minus oil production as a rough estimate of North American and European/Eurasian net import requirements from 1965 through 2016. In the years before the oil price shocks of the 1970s, net import requirements were soaring in both regions. The price shocks caused demand to fall and production to rise, cutting into the net import requirement.

After the collapse of oil prices in 1986, however, North American demand began to climb, whereas crude production peaked and entered a period of decline. The net import requirement grew from around 4.4 MMbpd in 1986 to over 11.4 MMbpd in 2005. Then, the Shale Boom, plus expanded output in Canada, reversed this. North American demand also has declined over the past decade. Between 2005 and 2016, North America’s net supply gap fell below 4.6 MMbpd, an astonishing drop of 6.8 MMbpd.

In contrast, crude production in Europe/Eurasia has been growing steadily for decades, while demand has been declining. The result has been a sustained decline in the net import requirement, which fell from approximately 7.9 MMbpd in 1992 to less than 1.1 MMbpd in 2016.

In short, the world expected that the U.S. would continue to purchase more and more crude from the international market. The expansion of regional supply reversed this.

The Shale Boom and Internal Crude Logistics

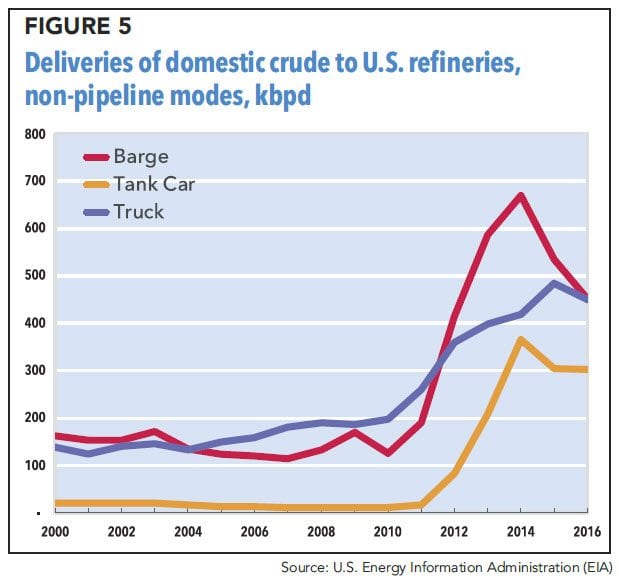

The huge upsurge in U.S. production from shale plays placed enormous pressure on oil transport infrastructure. This was compounded by the increase in Canadian production of bitumen-based synthetic crudes and diluted bitumens (dilbits), which are produced mainly in Alberta province. This is north of the Dakotas, where Bakken LTOs already were straining the oil delivery system. The crude pipelines in the area were accustomed to small, locally crude batches, but they were overwhelmed when North Dakota’s crude production jumped from less than 100 thousand barrels per day (kbpd) in 2005 to over 1 MMbpd in 2014.

Looking back to Figure 1 illustrating the change in the WTI-Brent price differential, note the huge drop in relative WTI prices in 2011 – 2012. Domestic crudes were being sold at heavily discounted prices during those years. Infrastructure was overloaded, and producers cut prices to get rid of excess inventory.

In the U.S., pipelines are the chief mode of transporting crude to refineries. As pipeline capacity was filled, delivery of domestic crude by non-pipeline modes increased. According to the EIA, delivery by barge rose by over 500% (from 126 kbpd in 2010 to 669 kbpd) in 2015. Delivery by tank car grew a whopping 30x (from 12 kbpd in 2010 to 365 kbpd in 2014). Delivery by truck more than doubled during that time, rising from 198 kbpd in 2010, to 418 kbpd in 2014, and to 484 kbpd in 2015. By 2014 – 2015, additional pipeline capacity began to come online, and the use of these other modes began to ebb.

Removal of restrictions on crude exports

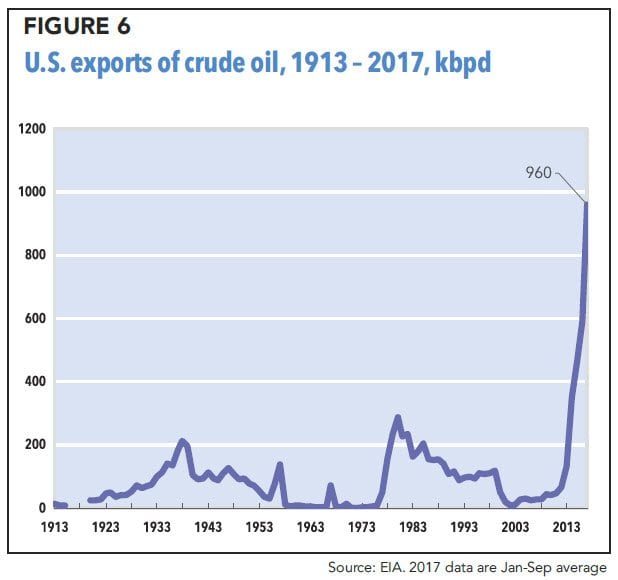

The regional oversupply of crude in the U.S. was exacerbated by laws in place that severely restricted the exports of domestic crude. The restrictions were commonly referred to as the “crude export ban,” though as accompanying Figure 6 illustrates, the U.S. has exported crude for over a century. The EIA reported that the U.S. exported 13 kbpd of crude in the year 1913. In 1975, following the oil price shock caused by the Arab Oil Embargo, the U.S. enacted severe restrictions on the export of crude oil under the Energy Policy and Conservation Act. Some crude trades were allowed, but others required specific licenses from the U.S. Department of Commerce.

The restrictions on exports, although not a ban, were a major deterrent to free trade. The restrictions were in place for forty years, and much of the nation’s petroleum infrastructure was built with these restrictions in mind. In 2015, Congress voted to end the restrictions. Crude exports shot up to 591 kbpd in 2016, and they have averaged 960 kbpd during the first three quarters of 2017. Unsurprisingly, the value of WTI crude improved relative to Brent.

Allowing exports also alleviated some of the strain on oil transport. Already, additional pipeline capacity was easing the flow of oil, reducing the need for more expensive transport options. Freeing up the export of U.S. light crudes made seaborne tanker trade more efficient as well, since inbound tankers carrying medium or heavy crudes could sometimes load a backhaul cargo for at least part of the return voyage, rather than steaming back in ballast (with empty cargo tanks).

No more “steady state” for the WTI-Brent price differential

When the U.S. was on its staid course of doing everything the global market expected, WTI tracked its Trans-Atlantic cousin, Brent, quite closely. The price differential was on a steady course, with WTI favored with a premium based on its slightly more favorable quality.

But the steady-state relationship ended.

The past decade has been enormously eventful. The price spike of 2008 sent crude prices above $130/b. A catastrophic global recession followed. But the high prices fostered the U.S. Shale Boom, bringing over 4 million barrels per day of new supply online in short order. Oil transport infrastructure was overwhelmed, prompting use of non-pipeline modes and a wave of pipeline construction.

Prices weakened, and OPEC launched an oil price war. Many U.S. producers went out of business, but many remained and grew even stronger. As of the time of this writing, U.S. crude production has hit a new record of over 9.6 MMbpd.

The removal of crude export restrictions unleashed exports. Although the accompanying figure shows exports averaging 960 kbpd during the first three quarters of 2017, the EIA’s weekly export data for the fourth quarter to date show that exports are now close to 1500 kbpd.

The market has changed in so many ways, and it appears that the changes are irrevocable. Although WTI is most likely a more valuable refinery feedstock than Brent, many other factors are at play that refinery economics cannot explain. Numerous forces beyond just quality weigh upon the WTI-Brent relationship: the shale boom, the changing crude slate, the supply-demand balances in regional markets, transport logistics and regulatory requirements. These are large, powerful forces, and they are changing the relationship between the two Trans-Atlantic cousins.

Will the differential ever revert back to the steady course with WTI slightly above Brent? Such a thing is not expected in 2018. What are these crudes really “worth” relative to one another? As the Latin writer Publilius Syrus in the first century BC noted: “Everything is worth what its purchaser will pay for it.”

This article contains material appearing in Mansfield Energy’s FUELSNews360°, Q4 2017