Oil Prices Turning Lower

- RBOB prices near support

- U.S. refineries operating below par

- Gasoline crack spreads for next spring are around $13.70

- Global natural gas demand is recovering

Alan Levine, Chairman of Powerhouse

The Matrix

Labor Day-week futures prices ended on a soft note. RBOB spot futures reached a new contract low at $1.0755 before settling at $1.0949.

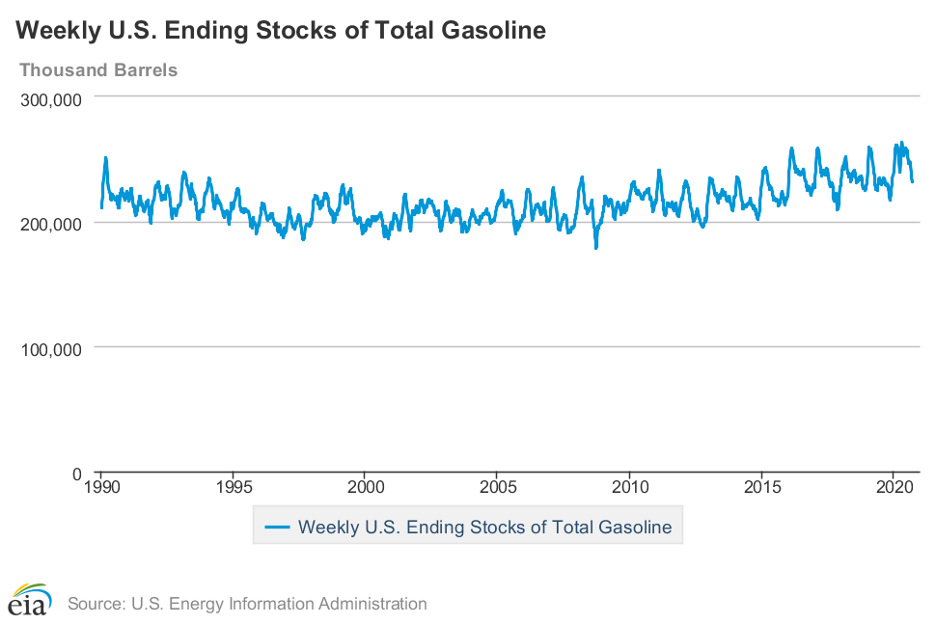

Gasoline Stocks 1990 – 2020 source: EIA

Low gasoline prices are not uncommon in the autumn. Current levels, then, are in line with historical experience. But low prices are coming at a time when inventories have shed more than 31 million barrels since stocks were bloated in April’s shut-down economy.

Low prices are not consistent either with sub-par refinery activity. The EIA weekly supply/demand report showed refinery utilization at 71.8% of capacity. Underutilization was particularly sharp along the Gulf Coast (PADD III.) Facilities in Texas and Louisiana ran at 63.9% of capacity. Only last year at this time, Gulf operations were put at 96.6%. Both the Midwest and the West Coast also showed lower refining activity.

Covid-19 has played a significant role in reducing refinery output. Gasoline demand is currently at 8.4 million barrels daily. This is far better than earlier this year, but 1.5 million barrels per day less than last year at this time.

Typically in autumn, traders watch gasoline demand and refinery use with an eye toward entering long spring gasoline crack spreads (the gasoline crack spread is comprised of one long gasoline futures contract minus one short crude oil futures contract. There are other formulations as well). Demand is running behind normal but is slowly improving. And gasoline inventories are falling and approaching their five-year average level.

Improving demand, declining inventories and below-average gasoline output at refineries are the ingredients of a more robust crack spread. Currently, the January 2021 winter gas crack is trading at $6.80; the May 2021 spring grade gas crack is $13.78.

Weather-related events have kept some refining out of service and with it the capacity to make gasoline. Expectations of improved gasoline demand next spring could work to support RBOB futures. Powerhouse does not see a gasoline crack spread buying opportunity just now, but that opportunity may develop soon.

Supply/Demand Balances

Supply/demand data in the United States for the week ended September 4, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose by 2.0 million barrels during the week ended Sept. 4, 2020.

Commercial crude oil supplies in the United States increased by 2.0 million barrels from the previous report week to 500.4 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.2 million barrels from to 12.2 million barrels

PADD 2: Plus 1.2 million barrels to 141.1 million barrels

PADD 3: Plus 0.7 million barrels to 269.4 million barrels

PADD 4: Down 1.2 million barrels to 23.4 million barrels

PADD 5: Plus 1.2 million barrels to 54.4 million barrels

Cushing, Oklahoma inventories were up 1.9 million barrels from the previous report week to 54.4 million barrels.

Domestic crude oil production was rose 300,000 barrels per day from the previous report week to 10.0 million barrels daily.

Crude oil imports averaged 5.423 million barrels per day, a daily increase of 523,000 barrels. Exports decreased 58,000 barrels daily to 2.944 million barrels per day.

Refineries used 81.0% of capacity, up 1.4% from the previous report week.

Crude oil inputs to refineries decreased 1.089 million barrels daily; there were 12.779 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 943,000 barrels daily to reach 13.362 million barrels daily.

Total petroleum product inventories fell 5.4 million barrels from the previous report week.

Gasoline stocks decreased 3.0 million barrels daily from the previous report week; total stocks are 231.9 million barrels.

Demand for gasoline fell 396,000 barrels per day to 8.390 million barrels per day.

Total product demand increased 1.699 million barrels daily to 18.678 million barrels per day.

Distillate fuel oil stocks decreased 1.7 million barrels from the previous report week; distillate stocks are at 175.8 million barrels. EIA reported national distillate demand at 3.713 million barrels per day during the report week, a decrease of 205,000 barrels daily.

Propane stocks increased 2.2 million barrels from the previous report week; propane stocks are 97.4 million barrels. The report estimated current demand at 1.096 million barrels per day, an increase of 473,000 barrels daily from the previous report week.

Natural Gas

September natural gas futures ended August on an exuberant note. Prices moved above resistance, reaching $2.743 in the spot contract. There was no follow-through, however, and prices have since retreated.

Range-bound trading has kept prices in a narrow band since February. The move above resistance, even though it failed, may carry other bullish news. Press sources are reporting that global demand is recovering. Excess storage is being whittled away. Europe carried a surplus to last year; supplies are now nearly on par. And the U.S. is no longer insulated from the effect of international natural gas movements.

According to the EIA:

The net injections [of natural gas] into storage totaled 70 Bcf for the week ending September 4, compared with the five-year (2015–19) average net injections of 68 Bcf and last year’s net injections of 80 Bcf during the same week. Working natural gas stocks totaled 3,525 Bcf, which is 409 Bcf more than the five-year average and 528 Bcf more than last year at this time.

The average rate of injections into storage is 7% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 10.6 Bcf/d for the remainder of the refill season, the total inventory would be 4,132 Bcf on October 31, which is 409 Bcf higher than the five-year average of 3,723 Bcf for that time of year.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2020 Powerhouse Brokerage, LLC, All rights reserved