Oil Prices Eye Signs of Softening Economy

- Equity markets under pressure

- Price risks of Iranian sanctions ease

- U.S. crude oil production remains flat

- End-of-October natural gas storage could be 3.2 Tcf

The Matrix

Oil price levels and directions are inevitably uncertain. The current economic environment provides no exception. Broad equities markets are showing cracks in a long running bull market and any list of economy-moving elements includes a wider than normal range of influences. Overall, concerns focus on growth slowing globally and the effect of tariffs imposed between the United States and China. An (incomplete) list of factors would include:

- Rising interest rates,

- Brexit

- Emerging Market challenges

- Growing U.S. budget deficits

- Political uncertainties in the Middle East.

Oil markets continue to worry about the planned imposition of sanctions on Iranian oil, now scheduled for November 5th. The sanctions are bullish, but a softer economy could limit their impact. Indeed, some observers believe the lost production has already been factored into price. Analysis of how to deal with Iranian oil already taken in anticipation of sanctions is complicated because China has reportedly been storing, rather than refining the crude oil. This is bearish for future supply/demand balances.

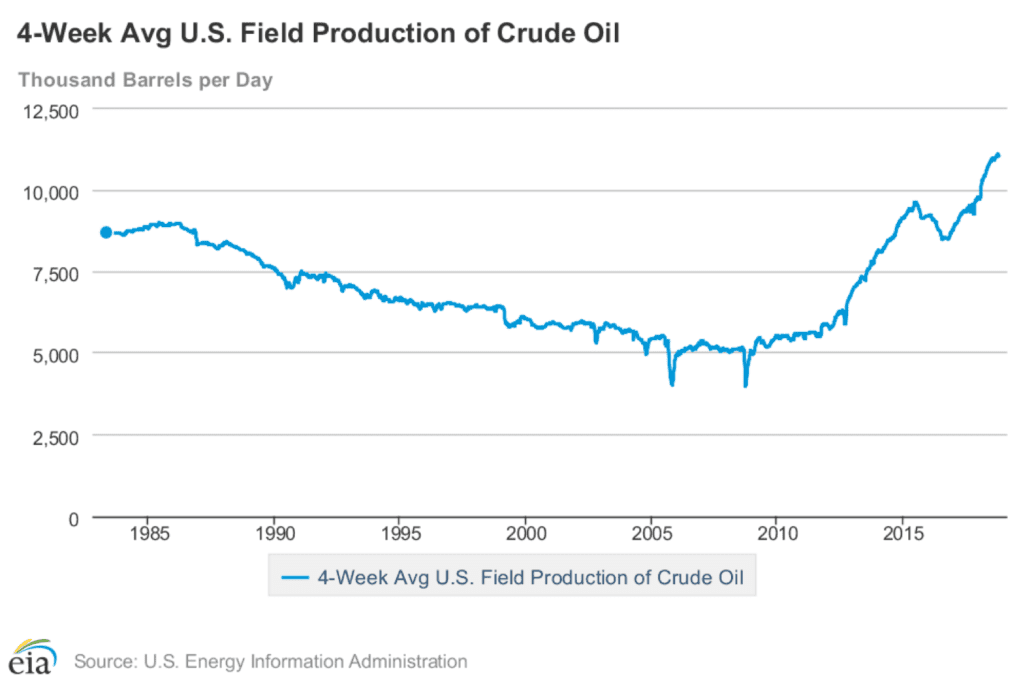

Alternative supply sources may not be able fully to supply adequate crude oil to refiners. U.S. crude oil production remains at 10.9 million barrels daily In EIA’s weekly Supply/Demand estimates. This level of output was reached In June 2018, after a long period of growth. Production has remained stuck around 11 million barrels per day. since then.

U.S Field Production of Crude 1983 – 2018 Source: EIA

One private analysis projects domestic U.S. production moving to 13 million barrels daily by 2021. This analysis suggests after 2021, U.S. production will be less important in global balances. This will be because (1) there will prove to be fewer barrels than first thought, (2) per-well productivity will also be lower than expected and (3) flatter growth in production. The Eagle Ford Shale, for example is already facing reduced estimates of quantity.

Supply/Demand Balances

Supply/demand data in the United States for the week ending October 19, 2018 were released by the Energy Information Administration.

Total commercial stocks of petroleum declined 8.0 million barrels during the week ending October 19, 2018.

There were draws in stocks of gasoline, fuel ethanol, K-jet fuel, distillates, residual fuel, propane, and other oils.

Commercial crude oil supplies in the United States increased to 416.4 million barrels, a build of 6.5 million barrels.

Crude oil supplies increased in four of the five PAD Districts. PAD District 1 (East Coast) stocks rose 0.6 million barrels, PADD 2 (Midwest) stocks increased 3.0 million barrels, PADD 3 (Gulf Coast) stocks were up 2.3 million barrels, and PADD 5 (west Coast) stocks gained 0.6 million barrels. PADD 4 (Rockies) stocks fell 0.1 million barrels from the previous report week.

Cushing, Oklahoma inventories increased 1.4 million barrels from the previous report week to 30.0 million barrels.

Domestic crude oil production was unchanged from the previous report week to 10.9 million barrels per day.

Crude oil imports averaged 7.678 million barrels per day, a daily increase of 63,000 barrels per day. Exports rose 398,000 barrels daily to 2.180 million barrels per day.

Refineries used 89.2 per cent of capacity, an increase of 0.4 percentage points from the previous report week.

Crude oil inputs to refineries decreased 48,000 barrels daily; there were 16.268 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, increased 78,000 barrels daily to 16.591 million barrels daily.

Total petroleum product inventories fell 14.3 million barrels from the previous report week.

Gasoline stocks decreased 4.8 million barrels from the previous report week; total stocks are 229.3 million barrels.

Demand for gasoline increased 141,000 barrels per day to 9.324 million barrels per day.

Total product demand increased 1.531 million barrels daily to 21.491 million barrels per day.

Distillate fuel oil stocks decreased 2.3 million barrels from the previous report week; distillate stocks are 130.4 million barrels. National distillate demand was reported at 4.006 million barrels per day during the report week. This was a weekly increase of 213,000 barrels daily.

Propane stocks declined 0.3 million barrels from the previous report week; propane stock are 82.0 million barrels. Current demand is estimated at 1.408 million barrels per day, an increase of 546,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Net injections fell lower than the five-year average. Net injections into storage totaled 58 Bcf for the week ending October 19, compared with the five-year (2013–17) average net injections of 77 Bcf and last year’s net injections of 63 Bcf during the same week. Working gas stocks totaled 3,095 Bcf, which is 624 Bcf lower than the five-year average and 606 Bcf lower than last year at this time.

Working gas stocks’ deficit to the five-year average increased, and the deficit to the bottom of the five-year range also increased. The average rate of net injections into storage is 14% lower than the five-year average so far in this refill season (April through October). If the rate of injections into storage matched the five-year average of 8 Bcf/day for the remainder of the refill season, total inventories will be 3,191 Bcf on October 31, which is 624 Bcf lower than the five-year average of 3,815 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2018 Powerhouse, All rights reserved.