Oil Fundamentals Still Determine Price Outlook

- OPEC+ plans to raise production in 2021 in question.

- Libya returns to supplying global markets

- U.S. oil inventories high but shrinking

- Natural gas production falling

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

The outlook for global crude oil supply remains muddled. OPEC+ had expressed interest in easing current quotas in 2021 but resistance from managers of Russian oil companies may have thrown a wrench into that plan. Oil companies have reportedly discussed a possible extension of current oil output restrictions into the first quarter of 2021 with Russian Energy Minister Alexander Novak. The UAE, Kuwait, and Iraq have also been uncertain about extending OPEC oil production cuts into 2021. This is no more than the recognition of an oversupplied oil market.

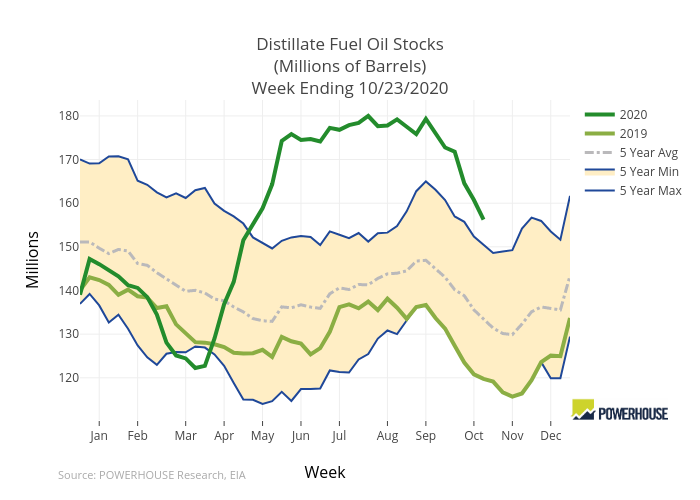

Distillate Fuel Oil Stocks 2015 – 2020 Source: EIA, POWERHOUSE

Bearish industry data have been carrying prices lower in the week just passed. WTI crude oil, for example, lost around five dollars in the nearest futures contract. The loss has been largely attributed to a new expansion of Covid-19 and the resulting impact on product demand. EIA reported a recovery of 1.2 million barrels daily in domestic crude oil production, bouncing back from shut-ins in the Gulf of Mexico and on-shore facilities as well.

Another bearish element is the return of Libya to global markets. This too will add to excess global crude oil stocks.

There have been countervailing factors providing support for prices. Earlier this year, inventories stood at record levels. Distillate fuel oil stocks, for example, topped at 180 million barrels at the end of July. There are now 156 million barrels available, a drawdown of nearly 13 percent.

Refiners have reduced product output in response to softer demand.

Supply/Demand Balances

Supply/demand data in the United States for the week ended October 23, 2020, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell by 3.9 million barrels during the week ended October 23, 2020.

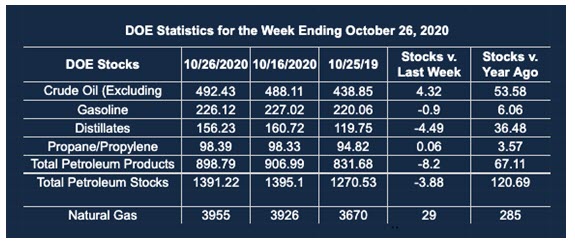

Commercial crude oil supplies in the United States increased by 4.3 million barrels from the previous report week to 492.4 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.4 million barrels to 10.7 million barrels

PADD 2: Down 0.8 million barrels to 146.0 million barrels

PADD 3: Plus 5.3 million barrels to 255.9 million barrels

PADD 4: Down 0.1 million barrels to 23.0 million barrels

PADD 5: Down 0.4 million barrels to 51.5 million barrels

Cushing, Oklahoma inventories were down 0.4 million barrels from the previous report week to 60.4 million barrels.

Domestic crude oil production rose 1,600,000 barrels per day to 11.1 million barrels daily.

Crude oil imports averaged 5.664 million barrels per day, a daily increase of 545,000 barrels. Exports increased 424,000 barrels daily to 3.460 million barrels per day.

Refineries used 74.6% of capacity, up 1.7% from the previous report week.

Crude oil inputs to refineries increased 362,000 barrels daily; there were 13.388 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 307,000 barrels daily to reach 13.890 million barrels daily.

Total petroleum product inventories fell 8.2 million barrels from the previous report week.

Gasoline stocks decreased 0.9 million barrels daily from the previous report week; total stocks are 226.1 million barrels.

Demand for gasoline rose 256,000 barrels per day to 8.545 million barrels per day.

Total product demand increased 1.519 million barrels daily to 19.631 million barrels per day.

Distillate fuel oil stocks decreased 4.5 million barrels from the previous report week; distillate stocks are at 156.2 million barrels. EIA reported national distillate demand at 4.240 million barrels per day during the report week, an increase of 553,000 barrels daily.

Propane stocks increased 0.1 million barrels from the previous report week; propane stocks are 98.4 million barrels. The report estimated current demand at 1.121 million barrels per day, a decrease of 353,000 barrels daily from the previous report week.

Natural Gas

December natural gas futures are now the spot futures contract price. November prices settled at $2.996. December spot added nearly $0.29 to natural gas value, trading around $3.30. Prices bottomed in late June at $1.432; they are now 2.3 times that level.

As we approach the beginning of the natural gas withdrawal season, analysts are asking if these prices are the start of a new period of tight supply in natural gas pricing. This reflects expectations of lower production of associated natural gas and tight funding among drillers. Pipeline transportation shortfalls continue to be a barrier to availability as well.

A further diversion of U.S. supply will be created by expanding LNG exports. Scheduled flows have reportedly recovered to their highest levels since 2016, when LNG exports began.

According to the EIA:

The net [natural gas] injections into storage totaled 29 Bcf for the week ending October 23, compared with the five-year (2015–19) average net injections of 67 Bcf and last year’s net injections of 89 Bcf during the same week. Working natural gas stocks totaled 3,955 Bcf, which is 289 Bcf more than the five-year average and 285 Bcf more than last year at this time.

The average rate of injections into storage is 1% lower than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 7.1 Bcf/d for the remainder of the refill season, the total inventory would be 4,012 Bcf on October 31, which is 289 Bcf higher than the five-year average of 3,723.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2020 Powerhouse Brokerage, LLC, All rights reserved