A Silver Lining in Quiet Markets

- Petroleum prices continue to grind sideways

- Price volatility for diesel and gasoline at the lowest since February

- Option premiums are falling with lower volatility

- Natural gas tests $1.80 resistance

The Matrix

Activity in petroleum futures has gone from boom to bust. Earlier this year, energy futures markets experienced high trading volume due to the double whammy of a market share price war between Saudi Arabia and Russia and the realization that COVID-19 would become a global pandemic. It was not uncommon to see daily price moves of a dime or more in gasoline and diesel. And, of course, who can forget that WTI futures turned negative.

Flash forward three months, and trading activity has ground to a halt. It is not unexpected to see a dip in trading volumes in July, but this summer has been exceptionally slow. Global demand for petroleum has recovered from earlier this year. OPEC+ has been, for the most part, disciplined with agreed cuts. U.S. shale production has stuttered. A week ago, U.S. oil and gas rigs fell to an all-time low of 253 rigs in service. The market has found equilibrium, and prices are chopping in a tight trading range in place for several weeks. The sideways price action is taking its toll on trading volumes.

There is a silver lining to a quiet market. Volatility is a vital component to option pricing. Lower volatility corresponds to cheaper option premiums. Price volatility is at the lowest we have experienced since February. Given the low volatility premium, an option strategy could be a good approach to some of the issues currently facing buyers and sellers of fuel.

Some fixed price buyers of physical fuel are now wondering if they will need all the volume of committed gallons due to new shut-downs. At writing, the at-the-money monthly average ULSD puts covering the next three months would cost under a dime per gallon. As witnessed earlier this year, the market can move a dime in a day.

There are nearly 200 vaccines being developed with five now in large scale testing. What if a viable cure for Covid-19 is ready for distribution in early 2021? Where could prices go? It is not uncommon for prices to jump on any announcement of successful vaccine news.

As mentioned in last week’s Energy Market Situation, distillate and gasoline prices are still better than this time last year, or for that matter, the past several years.

A call option allows the buyer to take advantage of today’s lower prices for future gallons without buyer’s remorse if prices collapse. ULSD and RBOB options are available through calendar 2023.

Please contact POWERHOUSE for the latest pricing.

Supply/Demand Balances

Supply/demand data in the United States for the week ended July 17, 2020, were released by the Energy Information Administration.

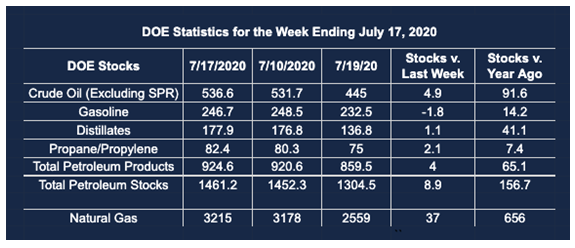

Total commercial stocks of petroleum rose by 8.8 million barrels during the week ended July 17, 2020.

Commercial crude oil supplies in the United States increased by 4.9 million barrels from the previous report week to 536.6 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.1 million barrels to 13.2 million barrels

PADD 2: Plus 0.3 million barrels to 137.5 million barrels

PADD 3: Plus 4.9 million barrels to 306.0 million barrels

PADD 4: Down 0.2 million barrels to 25.4 million barrels

PADD 5: Down 0.2 million barrels to 54.5 million barrels

Cushing, Oklahoma inventories were up 1.4 million barrels from the previous report week to 50.1 million barrels.

Domestic crude oil production rose 100,000 barrels per day to 11.1 million barrels daily.

Crude oil imports averaged 5.941 million barrels per day, a daily increase of 373,000 barrels. Exports rose 450,000 barrels daily to 2.993 million barrels per day.

Refineries used 77.9% of capacity, down 0.2% from the previous report week.

Crude oil inputs to refineries decreased 103,000 barrels daily; there were 14.206 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 49,000 barrels daily to reach 14.777 million barrels daily.

Total petroleum product inventories rose 3.9 million barrels from the previous report week.

Gasoline stocks decreased 1.8 million barrels daily from the previous report week; total stocks are 246.7 million barrels.

Demand for gasoline fell 98,000 barrels per day to 8.550 million barrels per day.

Total product demand decreased 826,000 barrels daily to 17.654 million barrels per day.

Distillate fuel oil stocks increased 1.1 million barrels from the previous report week; distillate stocks are at 177.9 million barrels. EIA reported national distillate demand at 3.223 million barrels per day during the report week, a decrease of 470,000 barrels daily.

Propane stocks increased 2.0 million barrels from the previous report week; propane stocks are 82.4 million barrels. The report estimated current demand at 1.001 million barrels per day, an increase of 88,000 barrels daily from the previous report week.

Natural Gas

While the EIA storage report did not provide any surprises, a massive heat dome impacting most of the country combined with strengthening overseas prices were able to move the NYMEX Henry Hub futures higher. Prices finished the week near $1.80 If prices can move convincingly through $1.80, the next resistance is $1.90, a level which has capped prices since mid-May.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2020 Powerhouse, All rights reserved.