Petroleum Prices Correct

- Trade war worries take center stage

- Brent crude sees largest single day sell-off in over two years

- Large draw in U.S. crude stocks shrugged off for now

- New LNG futures contract being launched by the CME

The Matrix

The oil markets had been absorbing a slow drip of bearish news without much reaction. This ended Wednesday with a wave of selling moving prices down sharply. Brent crude oil futures had the largest single-day sell-off in over two years, even in the face of a very bullish report on crude oil stocks released by the EIA. What changed? And is this a correction, or the start of something bigger?

For weeks prices had been moving higher. Bearish headlines were shrugged off. Suncor reported the Syncrude production facility would return to service in the second half of July, albeit at reduced rates (a return to full production is not expected until mid-September.) Secretary of State Pompeo said the U.S. would consider requests for waivers from Iran oil sanctions, potentially chipping away at the administration’s “zero” export target. Production from Saudi Arabia is on the rise. The market welcomed the additional supply.

That changed midweek when two news items precipitated the selloff that moved WTI nearly $4.00 a barrel lower and ULSD prices down $0.12 a gallon. Libya’s state-run National Oil Corporation lifted force majeure on eastern oil ports that had been crippled by a continued civil war. Potentially more bearish, the White House escalated trade war by readying tariffs on an additional $200 billion of Chinese imports. If China retaliates, it could be very problematic for the U. S’s booming export business. China has increasingly become one of the largest importers of our crude oil, propane and liquified natural gas. According to the EIA, more U.S. crude was sent to China than another other country except Canada in 2017.

For now, the supply and demand balance still looks tight. Domestic crude oil inventories declined by an impressive 12.6 million barrels in the past week. There are questions about how long it will take to see the Libyan oil hit the markets. New tariffs on China do not take effect for two months, leaving time for negotiations. The Paris based International Energy Agency (IEA) warned that further supply from Saudi Arabia and Russia being pumped to replace the lost production from Venezuela and Iran would leave minimal spare capacity in the system. This is bullish, and for the moment, the pullback in petroleum prices seems corrective. However, if this week’s trading is an indication, a growing trade war could change the market sentiment quickly.

Supply/Demand Balances

Supply/Demand Balances

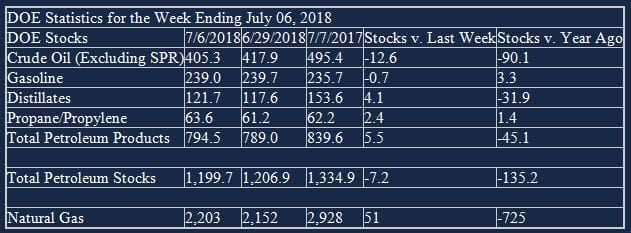

Supply/demand data in the United States for the week ending July 06, 2018 were released by the Energy Information Administration.

Total commercial stocks of petroleum fell 7.2 million barrels during the week ending July 06, 2018.

There were builds in stocks of fuel ethanol, distillates, propane, and other oils. There were draws in stocks of gasoline and residual fuel.

Commercial crude oil supplies in the United States decreased to 405.2 million barrels, a draw of 12.6 million barrels.

Crude oil supplies decreased in all five of the five PAD Districts. PAD District 1 (East Coast) crude oil stocks declined 2.5 million barrels, PADD 2 (Midwest) stocks fell 1.0 million barrels, PADD 3 (Gulf Coast) stocks retreated 7.2 million barrels, PADD 4 (Rockies) stocks decreased 0.4 million barrels, and PADD 5 (West Coast) stocks fell 1.5 million barrels.

Cushing, Oklahoma inventories decreased 2.1 million barrels from the previous report week to 25.7 million barrels.

Domestic crude oil production was unchanged from the previous report week at 10.900 million barrels per day.

Crude oil imports averaged 7.431 million barrels per day, a daily decrease of 1.624 million barrels per day. Exports decreased 309,000 barrels daily to 2.027 million barrels per day.

Refineries used 96.7 per cent of capacity, a decrease of 0.4 percentage points from the previous report week.

Crude oil inputs to refineries decreased 1,000 barrels daily; there were 17.652 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell 70,000 barrels daily to 17.981 million barrels daily.

Total petroleum product inventories saw an increase of 5.4 million barrels from the previous report week.

Gasoline stocks decreased 0.7 million barrels from the previous report week; total stocks are 239.0 million barrels.

Demand for gasoline declined 594,000 barrels per day to 9.275 million barrels per day.

Total product demand decreased 1.364 million barrels daily to 19.908 million barrels per day.

Distillate fuel oil stocks increased 4.1 million barrels from the previous report week; distillate stocks are 121.7 million barrels. National distillate demand was reported at 3.805 million barrels per day during the report week. This was a weekly decrease of 321,000 barrels daily.

Propane stocks rose 2.4 million barrels from the previous report week; propane stock are 63.6 million barrels. Current demand is estimated at 923,000 barrels per day, an increase of 100,000 barrels daily from the previous report week.

Natural Gas

According to the Energy Information Administration:

Working gas in storage was 2,203 Bcf as of Friday, July 6, 2018, according to EIA estimates. This represents a net increase of 51 Bcf from the previous week. Stocks were 725 Bcf less than last year at this time and 519 Bcf below the five-year average of 2,722 Bcf. At 2,203 Bcf, total working gas is within the five-year historical range.

A new LNG contract was announced by the CME last week. The CME has partnered with Cheniere Energy to develop the new contract. The LNG futures contract will be a physically delivered contract at Chenier’s Sabine Pass terminal on the U.S. Gulf Coast. Despite several attempts, there is not currently a global LNG benchmark. Most LNG contracts are long term based off of crude oil or an indexed gas price. “This agreement with Cheniere is significant because it will be the foundation for developing a new LNG risk management tool for producers, consumers and traders around the globe, while further cementing the role of Henry Hub Natural Gas futures as the global gas pricing benchmark,” Peter Keavey, CME Group’s Global Head of Energy said in a press release.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright © 2018 Powerhouse, All rights reserved.