Tight Oil Supply is the Most Constant Feature of Pricing

- Unusual weather creates supply shortages

- Refinery use collapses from extreme weather

- Oil prices enter new Supercycle phase?

- U.S. records impressive LNG exports.

Sincerely,

Alan Levine, Chairman

Powerhouse

(202) 333-5380

The Matrix

2022 ended and the New Year began with extreme weather events in many parts of the country. They impacted facilities in the West, where a “bomb cyclone” closed terminals in California. Flooding and loss of power were common in the region.

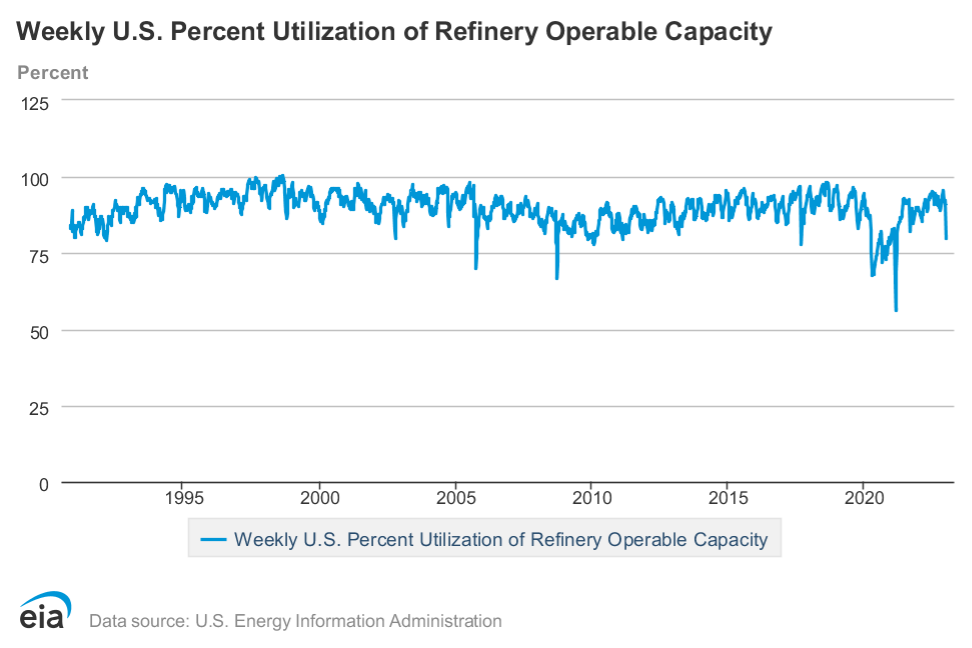

The effect of winter storms on refining was so severe that EIA reported Refinery Utilization at 79.6% of capacity for the week ended December 30. This compared with a rate of 92.0% the week before. Inputs of crude oil to facilities were put at 13.8 million daily barrels, a reduction of 2.3 million barrels daily for the week.

Refinery outages in the Midwest elevated regional prices and the Colonial Pipeline was briefly shut as well. Separately, Colorado’s only refinery was affected by fire, and is likely to be closed for several months.

One analysis put the Gulf Coast loss at 20 million barrels of petroleum products to the market. This included 6 million barrels of diesel fuel and 10 million barrels of gasoline.

Powerhouse has viewed recent industry experience as generally bullish for price over the next few years. Concerns over supply have grown, as U.S. crude oil production seems to have been stuck around 12.1 million barrels daily in the fourth quarter of 2022.

This is especially concerning as U.S. demand has persistently been rising since April of 2020 following the Covid19 economic shutdown and burdened storage. WTI crude oil futures fell to $37 at that time, completing a crude oil “Supercycle,” as seen by one of America’s largest investment banks. A Supercycle is a period of persistent price trending in one direction.

The previous crude oil price up-cycle began in 1997, reflecting the emergence of China as a global economic power, concluding in 2008 with that year’s financial crisis. Prices subsequently fell, bottoming in 2020. This analysis puts crude oil prices now on a course higher, moving perhaps to new all-time highs. This does not suggest a steady unrelenting move higher. There will be interim variations, but the general thrust will be upward.

The analysis posits an unstable first quarter 2023. The dollar is under pressure and China’s economy has yet to steady from its Covid shutdowns. Crude oil supply constraints, reflecting global tensions in Ukraine and China will support prices. As China reopens, renewed demand should continue to hold sway. Underinvestment in shale oil E&P will add to price strength.

Until the balance between inadequate supply and growing demand recovers, prices should be strong according to the banks’ analysis.

Supply/Demand Balances

Supply/demand data in the United States for the week ended December 30, 2022, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell (⬇) 3.1 million barrels to 1.205 billion barrels during the week ended December 30, 2022.

Commercial crude oil supplies in the United States increased (⬆) by 1.7 million barrels from the previous report week to 420.6 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down (⬇) 0.6 million barrels to 7.6 million barrels

PADD 2: Plus (⬆) 0.4 million barrels to 106.3 million barrels

PADD 3: Plus (⬆) 2.2 million barrels to 233.9 million barrels

PADD 4: Down (⬇) 0.5 million barrels to 23.9 million barrels

PADD 5: Plus (⬆) 0.2 million barrels to 49.0 million barrels

Cushing, Oklahoma, inventories were up (⬆) 0.3 million barrels from the previous report week to 25.3 million barrels.

Domestic crude oil production was up (⬆) 100,000 barrels daily from the previous report week at 12.1 million barrels daily.

Crude oil imports averaged 5.712 million barrels per day, a daily decrease (⬇) of 540,000 barrels. Exports increased (⬆) 742,000 barrels daily to 4.207 million barrels per day.

Refineries used 79.6% of capacity; 12.4 percentage points lower (⬇) than the previous report week.

Crude oil inputs to refineries decreased (⬇) 2.330 million barrels daily; there were 13.820 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, fell (⬇) 2.243 million barrels daily to 14.343 million barrels daily.

Total petroleum product inventories fell (⬇) by 4.8 million barrels from the previous report week, falling to 784.6 million barrels.

Total product demand decreased (⬇) 4.631 million barrels daily to 18.190 million barrels per day.

Gasoline stocks decreased (⬇) 0.3 million barrels from the previous report week; total stocks are 222.7 million barrels.

Demand for gasoline decreased (⬇) 1.813 million barrels per day to 7.514 million barrels per day.

Distillate fuel oil stocks increased (⬇) 1.4 million barrels from the previous report week; distillate stocks are at 118.8 million barrels. EIA reported national distillate demand at 2.799 million barrels per day during the report week, a decrease (⬇) of 1.081 million barrels daily.

Propane stocks decreased (⬇) by 3.7 million barrels from the previous report week to 80.7 million barrels. The report estimated current demand at 1.145 million barrels per day, a decrease (⬇) of 547,000 barrels daily from the previous report week.

Natural Gas

Spot Henry Hub natural gas futures ended the week of January 6 with a rally. But the failure of the nation to develop meaningful HDDs inclines one to think the recovery may be little more than a relief rally. The final week of 2022 recorded 14 fewer HDDs than normal for the nation. The populous Northeast accumulated even fewer HDDs. New England gathered 24 fewer HDDs than normal; the East North Central states, 26 HDDs less.

The longer-term situation for natural gas this year will depend on much more than weather. The loss of Russia as a reliable natural gas supplier has dramatically re-oriented the LNG market. European buyers are now competing for waterborne cargoes and Russia is attempting to reorient its natural gas exports to China.

America’s rise to prominence as the largest global supplier occurred last year. The nation tied Qatar to be the largest global supplier of liquified natural gas. Both countries exported 81.2 million tons in 2022. This was an impressive feat for the U.S. which has exported LNG since only 2016. If the export terminal at Freeport, TX had been operative, America would have led global exporters. Freeport is not expected to resume operations until sometime in the first quarter. Australia was in third spot.

According to the EIA:

Working gas in storage was 2,891 Bcf as of Friday, December 30, 2022, according to EIA estimates. This represents a net decrease of 221 Bcf from the previous week. Stocks were 308 Bcf less than last year at this time and 208 Bcf below the five-year average of 3,099 Bcf. At 2,891 Bcf, total working gas is within the five-year historical range.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2022 Powerhouse Brokerage, LLC, All rights reserved