Federal Initiatives Taking Hold of Energy Demand?

- Energy industry focusing on different drivers for price this year

- National security implications of threatened electric grids now headline news

- Infrastructure needs affecting demand

- Natural gas consumption, production, and exports broke records last year

Sincerely,

Alan Levine, Chairman

Powerhouse

(202) 333-5380

The Matrix

Big-picture energy topics could translate into higher prices for oil in 2023. Some analysts insist that a warmer winter is masking bullish features in the outlook. Last week’s Weekly Energy Market Situation emphasized damage to refineries and pipelines from harsh storms. These are now in the rear-view mirror and the effect of recent commercial and governmental initiatives to support infrastructure could soon take hold.

The largest concerns driving the energy industry’s thinking as 2023 opens are different than they were at the start of 2022 – and radically different than in, say, 2017, only five years ago.

Energy security has always been an underlying factor in energy planning, but the Russia/Ukraine conflict rocketed the issue to headline status.

Security for the U.S. electrical grid, too, has been troublesome. Recent attacks on the grid have elevated concerns.

Policy shifts at the Federal level have come front-and-center as legislation has opened the door to expanded renewable energy supply. The Inflation Reduction Act provides $11.7 billion for new loans. The Energy Infrastructure Reinvestment loan program takes $5 billion of that to help “retool, repower repurpose or replace” infrastructure.

How different this is from last year, when sustainability and lowering atmospheric carbon were at the top of the hit list. And even more than from five years ago. In 2017, one historian listed battery storage, smart-grids, and autonomous vehicles as the hottest topics among energy planners.

All of these topics still concern us, but the shift to renewable energy supplies, infrastructure upgrading and the prospects for pipeline systems can be seen as positive for the entire upstream/downstream supply chain.

Supply/Demand Balances

Supply/demand data in the United States for the week ended January 6, 2023, were released by the Energy Information Administration.

Total commercial stocks of petroleum rose (⬆) 22.4 million barrels to 1.227 billion barrels during the week ended January 6, 2023.

Commercial crude oil supplies in the United States increased (⬆) by 19.0 million barrels from the previous report week to 439.6 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus (⬆) 0.4 million barrels to 8.0 million barrels

PADD 2: Plus (⬆) 3.7 million barrels to 110.0 million barrels

PADD 3: Plus (⬆) 15.6 million barrels to 249.5 million barrels

PADD 4: Plus (⬆) 0.9 million barrels to 24.8 million barrels

PADD 5: Down (⬇) 1.7 million barrels to 47.3 million barrels

Cushing, Oklahoma, inventories were up (⬆) 2.5 million barrels from the previous report week to 27.8 million barrels.

Domestic crude oil production was up (⬆) 100,000 barrels daily from the previous report week at 12.2 million barrels daily.

Crude oil imports averaged 6.350 million barrels per day, a daily increase (⬆) of 637,000 barrels. Exports decreased (⬇) 2.070 million barrels daily to 2.137 million barrels per day.

Refineries used 84.1% of capacity; 4.5 percentage points higher (⬆) than the previous report week.

Crude oil inputs to refineries increased (⬆) 831,000 barrels daily; there were 14.651 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose (⬆) 817,000 barrels daily to 15.160 million barrels daily.

Total petroleum product inventories rose (⬆) by 3.4 million barrels from the previous report week, rising to 788.0 million barrels.

Total product demand decreased (⬇) 563,000 barrels daily to 17.627 million barrels per day.

Gasoline stocks increased (⬆) 4.1 million barrels from the previous report week; total stocks are 226.8 million barrels.

Demand for gasoline increased (⬆) 44,000 barrels per day to 7.558 million barrels per day.

Distillate fuel oil stocks decreased (⬇) 1.1 million barrels from the previous report week; distillate stocks are at 117.7 million barrels. EIA reported national distillate demand at 3.821 million barrels per day during the report week, an increase (⬆) of 1.022 million barrels daily.

Propane stocks decreased (⬇) by 2.1 million barrels from the previous report week to 78.6 million barrels. The report estimated current demand at 1.221 million barrels per day, an increase (⬆) of 76,000 barrels daily from the previous report week.

Natural Gas

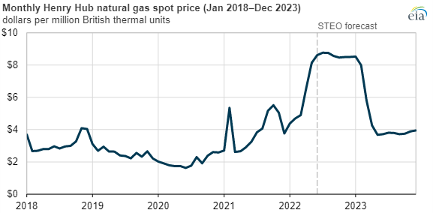

The Department of Energy expects that natural gas prices at Henry Hub could average $4.90 for 2023. DOE forecasts prices for 2024 to move even lower, averaging $4.80 next year. The 2023 forecast is a 9.8% cut in price from 2022. It reflects falling U.S. demand and relatively flat LNG exports. The weakness continuing into 2024 contemplates dry natural gas production growing more rapidly than LNG exports from expanded LNG export capacity.

Falling natural gas prices may be less of a surprise, considering that natural gas activity reached new highs in several important respects. Consumption, production, and exports broke records last year. Real prices hit a 14-year high.

Growth in the electric power sector was largely the result of the third-hottest summer on record affecting air-conditioning use. Moreover, there was less coal-fired power generation because of supply constraints including lower-than-average stockpiles and an increase in natural gas power generation.

DOE estimated domestic consumption at 88.7 Bcf/d for the year, an annual gain of 6 per cent. Electric power grew 8%. The commercial sector gained 7%.

Dry gas production added 3.5 Bcf/d in 2022. It reached 98.0 Bcf/d last year. Output the Permian Basin and the Haynesville region led the nation’s output.

Exports of natural gas trended higher. LNG added materially to the gain. Geopolitics played an important role in overseas use of American natural gas. Russian natural gas exports to Europe were offset by U.S. LNG, and the EU displaced East Asia as America’s main destination.

According to the EIA:

Net injections into [natural gas] storage totaled 11 Bcf for the week ended January 6, compared with the five-year (2018–2022) average net withdrawals of 157 Bcf and last year’s net withdrawals of 157 Bcf during the same week. Working natural gas stocks totaled 2,902 Bcf, which is 40 Bcf (1%) lower than the five-year average and 140 Bcf (5%) lower than last year at this time.

The average rate of withdrawals from storage is 10% lower than the five-year average so far in the withdrawal season (November through March). If the rate of withdrawals from storage matched the five-year average of 16.8 Bcf/d for the remainder of the withdrawal season, the total inventory would be 1,492 Bcf on March 31, which is 40 Bcf lower than the five-year average of 1,532 Bcf for that time of year.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2023 Powerhouse Brokerage, LLC, All rights reserved