EIA Posts Higher Crude Oil Price For 2021

- Crude oil price rally holds near top

- Energy price volatility stalls

- Petroleum use patterns impacted by vaccine

- LNG exports reduce supply in underground storage

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

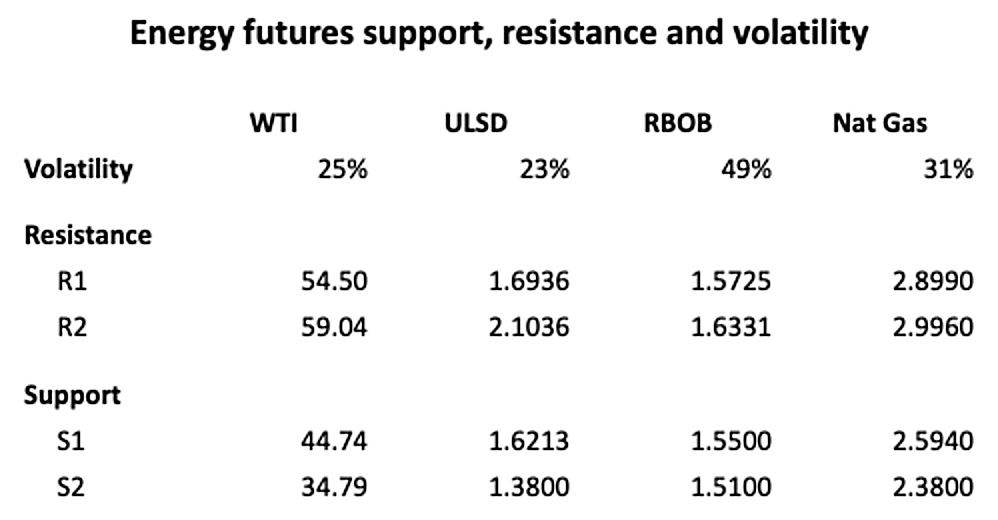

The price for WTI spot futures settled at $52.36 on Friday January 15, 2021. This was slightly below the current rally high of $53.93 seen on January 13. A futures rally underway since late April 2021, has offered few opportunities for buyers. The January futures price moved slightly lower on January 15 but not low enough to indicate a reversal in the rally.

Price patterns have been similar for ULSD and RBOB. Prices are experiencing slow advances with very small corrections. This has the effect of reducing volatility. Lower volatility produces narrower price bands and the possibility of greater price ranges once they break support or resistance.

Projections of oil prices in 2021 have generally been bullish. They have been offered with the assumption that the economy will be acting to offset the bearish impact of high unemployment on demand. The Energy Information Administration has revised upward its forecast for 2021 crude oil prices.

The January Short Term Energy Outlook (STEO) projects the 2021 average spot price for WTI to be $49.70 per barrel. This is a nearly $4 per barrel increase from EIA’s December projection.

EIA estimates world-wide demand to add 5.6 million barrels per day in 2021. An additional 3.3 million barrels daily will be added in 2022. EIA put 2020 demand at 92.2 million barrels daily. The impact of COVID-19 is very uncertain and could lead to a change in overall oil use, geographically and among industries.

A new consideration is the impact of ostensibly highly successful vaccines on the behavior of the economy. The Federal Government’s Project Warp Speed has encountered strong headwinds in its attempt to provide vaccines. As these barriers fall, improved vaccine availability should contribute to demand.

Supply/Demand Balances

Supply/demand data in the United States for the week ended January 8, 2021, were released by the Energy Information Administration.

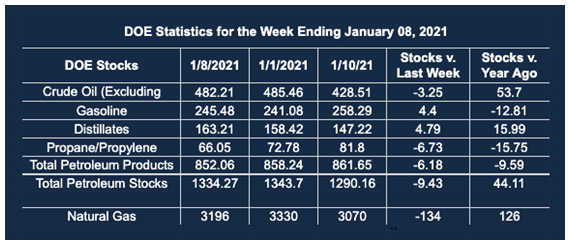

Total commercial stocks of petroleum fell by 9.4 million barrels during the week ended January 8, 2021.

Commercial crude oil supplies in the United States decreased by 3.2 million barrels from the previous report week to 482.2 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 0.1 million barrels to 10.2. million barrels

PADD 2: Down 2.4 million barrels to 144.1 million barrels

PADD 3: Down 1.1 million barrels to 257.5 million barrels

PADD 4: Plus 0.6 million barrels to 24.3 million barrels

PADD 5: Down 0.1 million barrels to 46.2 million barrels

Cushing, Oklahoma inventories were down 2.0 million barrels from the previous report week to 57.2 million barrels.

Domestic crude oil production was unchanged from the previous report week at 11.0 million barrels daily.

Crude oil imports averaged 6.239 million barrels per day, a daily increase of 870,000 barrels. Exports decreased 621,000 barrels daily to 3.011 million barrels per day.

Refineries used 82.0% of capacity, up 1.3% from the previous report week.

Crude oil inputs to refineries increased 274,000 barrels daily; there were 14.650 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 237,000 barrels daily to 15.071 million barrels daily.

Total petroleum product inventories fell 6.2 million barrels from the previous report week.

Gasoline stocks increased 4.4 million barrels daily from the previous report week; total stocks are 245.5 million barrels.

Demand for gasoline rose 91,000 barrels per day to 7.532 million barrels per day.

Total product demand increased 2.263 million barrels daily to 19.047 million barrels per day.

Gasoline stocks increased 4.4 million barrels daily from the previous report week; total stocks are 245.5 million barrels.

Demand for gasoline rose 91,000 barrels per day to 7.532 million barrels per day.

Total product demand increased 2.263 million barrels daily to 19.047 million barrels per day.

Distillate fuel oil stocks increased 4.8 barrels from the previous report week; distillate stocks are at 163.2 million barrels. EIA reported national distillate demand at 3.609 million barrels per day during the report week, an increase of 653,000 barrels daily.

Propane stocks decreased 6.7 million barrels from the previous report week; propane stocks are 66.0 million barrels. The report estimated current demand at 2.104 million barrels per day, an increase of 403,000 barrels daily from the previous report week.

Natural Gas

The impact of export LNG is changing the construction of natural gas prices. LNG has become a significant factor in pricing, especially removing more than 10 Bcf per day from U.S. storage. One analysis suggests that if exports continue at this rate, domestic underground storage could end this withdrawal season with only 2.6 Tcf daily, the lowest start to the injection season ever recorded.

According to the EIA:

The net withdrawals from [natural gas] storage totaled 134 Bcf for the week ending January 8, compared with the five-year (2016–2021) average net withdrawals of 161 Bcf and last year’s net withdrawals of 91 Bcf during the same week. Working natural gas stocks totaled 3,196 Bcf, which is 218 Bcf more than the five-year average and 126 Bcf more than last year at this time.

The average rate of withdrawals from storage is 3% lower than the five-year average so far in the withdrawal season (November through March). If the rate of withdrawals from storage matched the five-year average of 14.3 Bcf/d for the remainder of the withdrawal season, the total inventory would be 2,024 Bcf on March 31, which is 218 Bcf higher than the five-year average of 1,806 Bcf for that time of year.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2021 Powerhouse Brokerage, LLC, All rights reserved