Markets Respond Slowly to Hurricane Ida and Afghan Withdrawal

- Uncertainty shrouds U.S. withdrawal from Afghanistan

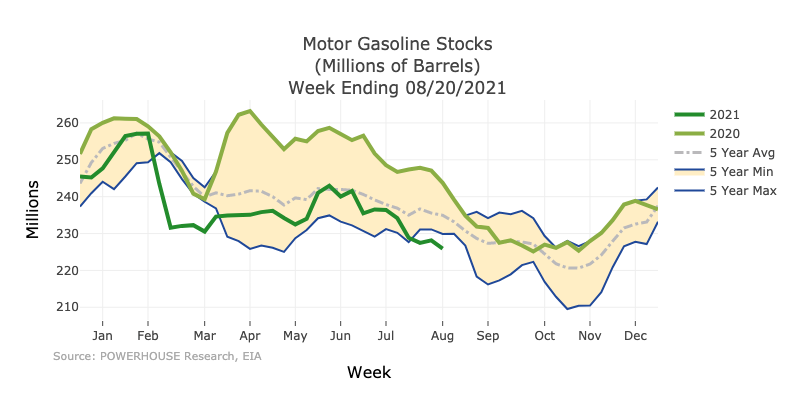

- U.S. gasoline inventories below five-year average

- Natural gas injections well below expectations

Alan Levine—Chairman, Powerhouse

(202) 333-5380

The Matrix

Powerhouse has chronicled an oil market trading in a price range through the summer now ended. Ironically, the factors that created a vibrant and volatile futures market for ULSD and gasoline remain in place. These include supply/demand balances, refinery utilization, persistent geopolitical instability in North Africa and the Middle East (MENA) and dramatic changes in climate. They are becoming more insistent over time.

One important geopolitical element is the announced conclusion of the 20-year war in Afghanistan and the withdrawal of U.S. forces, civilians and allies. The departure was disorderly, leading to more deaths. Nonetheless, oil prices have not reacted in any significant way. Afghanistan itself is not an important oil producer.

The regional balance of power could be affected following the United States departure from Afghanistan. While the U.S. retains the ability to project military power “over-the-horizon,” the withdrawal of on the ground forces in the region may open the door to uncertainty in larger strategic political relationships including those among the oil-rich nations in the region.

Oil demand in the U.S. remains a focus of the markets. The most recent report from the EIA showed gasoline demand rising to 9.57 million barrels per day, with gasoline sales expected to be even stronger during the upcoming Labor Day holiday weekend. Gasoline inventories have now fallen below the five-year average for this time of year.

Motor Gasoline Stocks 2016 – 2021 Source: EIA, Powerhouse

Propane is a much smaller part of total inventories, at 68.7 million barrels. Propane demand is growing and becoming an important part of the petroleum product story. Inventories have been hugging the lower edge of the five-year average of propane supplies, inviting continued price strength should demand conditions turn bullish this autumn.

Propane Stocks 2016 – 2021 Source: EIA, Powerhouse

Supply/Demand Balances

Supply/demand data in the United States for the week ended Aug. 20, 2021, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell 4.8 million barrels during the week ended Aug. 20, 2021.

Commercial crude oil supplies in the United States decreased by 3.0 million barrels from the previous report week to 432.6 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Down 0.6 million barrels to 8.2 million barrels

PADD 2: Down 0.6 million barrels to 114.5 million barrels

PADD 3: Down 1.4 million barrels to 239.6 million barrels

PADD 4: Down 1.1 million barrels to 21.1 million barrels

PADD 5: Up 0.5 million barrels to 47.0 million barrels

Cushing, Oklahoma, inventories were up 0.1 million barrels from the previous report week to 33.7 million barrels.

Domestic crude oil production was unchanged at 11.4 million barrels per day from the previous report week.

Crude oil imports averaged 6.157 million barrels per day, a daily decrease of 193,000 barrels. Exports fell 619,000 barrels daily to 2.812 million barrels per day.

Refineries used 92.4% of capacity; 0.2 percentage points higher than the previous report week.

Crude oil inputs to refineries increased 66,000 barrels daily; there were 16.072 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 43,000 barrels daily to 16.759 million barrels daily.

Total petroleum product inventories fell 1.9 million barrels from the previous report week.

Gasoline stocks decreased 2.2 million barrels from the previous report week; total stocks are 225.9 million barrels.

Demand for gasoline rose 239,000 barrels per day to 9.572 million barrels per day.

Total product demand increased 354 million barrels daily to 21.817 million barrels per day.

Natural Gas

Futures prices for natural gas moved higher during the week ended August 27. The weekly injection report added only 29 Bcf to underground storage—far less than the 40 Bcf addition anticipated by the industry. The shortfall was attributed to a failure to measure wind generation accurately.

Early indications of tropical storm activity pushed prices higher as well. The week ended with the previous resistance level of $4.205 being easily surpassed. Next major resistance is at $4.923. This level was last seen in November 2018. A projection of declining demand for this week as temperatures ease and Gulf Coast hurricane activity could impact the current rally.

According to the EIA:

Net [natural gas] injections into storage totaled 29 Bcf for the week ended August 20, compared with the five-year (2016–2020) average net injections of 44 Bcf and last year’s net injections of 45 Bcf during the same week. Working natural gas stocks totaled 2,851 Bcf, which is 189 Bcf lower than the five-year average and 563 Bcf lower than last year at this time.

The average rate of injections into storage is 13% lower than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 9.4 Bcf/d for the remainder of the refill season, the total inventory would be 3,530 Bcf on October 31, which is 189 Bcf lower than the five-year average of 3,719 Bcf for that time of year.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2021 Powerhouse Brokerage, LLC, All rights reserved