Weather Expectations Bullish for Oil Pricing

- Accelerating intensity of weather events

- Tornadoes caused 103 deaths in the U.S. last year

- Nineteen named hurricanes possible this year

- Eurasian natural gas supply to slip 5% in 2022

Sincerely,

Alan Levine, Chairman

Powerhouse

(202) 333-5380

The Matrix

Hurricanes, tornadoes, snowfall, and rainfall always underlie oil pricing, despite the current industry focus on geopolitical events. And weather events have been having significant implications for petroleum balances, reflecting the impact of climate change throughout the supply chain.

There were, for example, more than 1,300 confirmed reports of tornadoes in 2021 in the United States, where 103 tornado-related deaths were recorded. These were the most such deaths in the United States since 2011.

Hurricanes are severe weather features forming over tropical or subtropical waters. They are particularly important for oil and gas interests along the Atlantic and Gulf Coasts. The National Weather Service defines a “hurricane season” extending from June 1 to November 30.

The Colorado State University (CSU) has issued a seasonal hurricane forecast annually since 1984. It is a key planning tool for those involved with the petroleum supply chain.

Its projections for 2022 are now available. CSU expects 19 storms to be named this season. Nine of those are likely to become hurricanes. Four more could reach Categories 3, 4, or 5, requiring sustained winds of 111 miles per hour or more.

Nineteen storms are a significantly elevated number of events. They represent 130% of the thirty-year average number of named storms. Last year’s activity was 120% of the average.

Further evidence of the growing intensity of weather can be found in the likelihood that 47% of major hurricanes on the East Coast could make landfall in 2022. By comparison, the same data for the 20th century were 31%. (Gulf Coast expectations are similar.)

CSU cites the absence of El Nino as central to its forecasts. Moreover, Sea Surface Temperatures are near average in the Tropical Atlantic; the Caribbean and Subtropical Atlantic SSTs are warmer than average. Both conduce to an active season this year.

Supply/Demand Balances

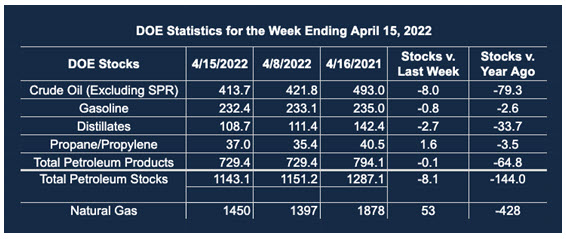

Supply/demand data in the United States for the week ended April 15, 2022, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell 8.1 million barrels during the week ended April 15, 2022.

Commercial crude oil supplies in the United States decreased by 8.1 million barrels from the previous report week to 413.7 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Minus 0.3 million barrels to 7.3 million barrels

PADD 2: Minus 1.5 million barrels to 105.8 million barrels

PADD 3: Minus 3.5 million barrels to 229.1 million barrels

PADD 4: Minus 0.3 million barrels 24.6 million barrels

PADD 5: Minus 2.4 million barrels to 47.0 million barrels

Cushing, Oklahoma, inventories were minus 0.1 million barrels from the previous report week to 26.2 million barrels.

Domestic crude oil production was plus 0.1 million daily barrels from the previous report week at 11.9 million barrels daily.

Crude oil imports averaged 5.837 million barrels per day, a daily decrease of 159,000 barrels. Exports increased from 2.090 million barrels daily to 4.270 million barrels per day.

Refineries used 91.0% of capacity; 1.0 percentage points higher than the previous report week.

Crude oil inputs to refineries increased by 194,000 barrels daily; there were 15.717 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 184,000 barrels daily to 16.332 million barrels daily.

Total petroleum product inventories fell 0.8 million barrels from the previous report week.

Gasoline stocks decreased 0.8 million barrels from the previous report week; total stocks are 232.4 million barrels.

Demand for gasoline rose by 131,000 barrels per day to 8.868 million barrels per day.

Total product demand increased by 0.262 million barrels daily to 19.033 million barrels per day.

Distillate fuel oil stocks decreased 2.7 million barrels from the previous report week; distillate stocks are at 108.7 million barrels. EIA reported national distillate demand at 3.822 million barrels per day during the report week, an increase of 339,000 barrels daily.

Propane stocks increased by 1.6 million barrels from the previous report week; propane stocks are at 37.0 million barrels. The report estimated current demand at 1.083 million barrels per day, an increase of 254,000 barrels daily from the previous report week.

Natural Gas

Eurasian natural gas supply is likely to be cut because of sanctions imposed on Russian exports. The International Energy Administration (IEA) predicts Eurasian supply to fall by 5% in 2022.

Lower expectations may already be seen in the price charts for Henry Hub natural gas spot futures. Prices peaked at $8.065 on April 18, 2022, following a long rally from $4.54 in mid-March. The four sessions of April subsequent to the top brought prices back to $6.53 on April 22, a little more than a 38.2% Fibonacci retracement. A full 50% retracement lies below at $6.23, constituting first major support.

Recent Elliott Wave counts suggest that the action since April 18th represents a completed third wave up followed by what could be a fourth wave downward retracement. If this pattern holds, we would expect a fifth and final wave higher to unfold with an initial target of $9.50 basis the front-month contract.

According to the EIA:

Net injections into storage totaled 53 Bcf for the week ended April 15, compared with the five-year (2017–2021) average net injections of 42 Bcf and last year’s net injections of 42 Bcf during the same week. Working natural gas stocks totaled 1,450 Bcf, which is 292 Bcf lower than the five-year average and 428 Bcf lower than last year at this time.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Powerhouse Futures & Trading Disclaimer

Copyright 2021 Powerhouse Brokerage, LLC, All rights reserved