Excerpted from This Week in Petroleum, December 14, 2022

Third-quarter 2022 (3Q22) financial results for 50 U.S. exploration and production (E&P) companies show that improved cash from operations went to increase capital expenditure and grow shareholder returns. Our analysis of public financial statements from these companies suggests their capital expenditure this year could increase 35% compared with 2021 because of more drilling and increased drilling costs related to supply chain constraints. These companies also continued to reduce their overall debt. This debt reduction suggests more profits could be directed to shareholder returns, such as dividends and share repurchases, in the future.

We base our analysis on the published financial reports of 50 publicly traded oil companies that produce most of their crude oil in the United States. As a result, our observations do not represent the sector as a whole because the analysis does not include private companies, which do not publish financial reports. These 50 publicly traded companies collectively produced about 4.2 million barrels per day (b/d) of crude oil, or 35% of all crude oil produced in the United States in 3Q22.

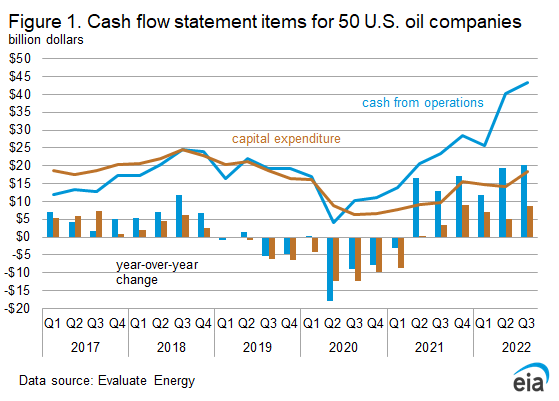

The West Texas Intermediate (WTI) crude oil price averaged $93.07 per barrel (b) in 3Q22, a 32% ($22.46/b) increase compared with 3Q21 and a 15% ($15.86/b) decrease compared with 2Q22. Cash from operations for the E&P companies increased 86% ($20.1 billion) from 3Q21 to $43.4 billion in 3Q22 and increased 8% ($3.2 billion) from 2Q22 (Figure 1). Despite lower crude oil prices in 3Q22, a $6.2 billion decrease in receivables meant the companies collected payments this quarter on earlier sales, contributing to increased cash from operations. These companies produced 10% more crude oil in 3Q22 (389,000 b/d) than in 3Q21. Compared with pre-pandemic levels, production in 3Q22 was 5% (215,000 b/d) lower than in 1Q20. Capital expenditures increased 89% ($8.7 billion) compared with 3Q21 to $18.3 billion and increased 30% ($4.2 billion) compared with 2Q22. Capital expenditures in 3Q22 were only 1% ($300 million) lower than in 3Q19, although they were 26% ($6.3 billion) lower than the most recent peak in 3Q18, when crude oil prices averaged $70/b.

Distributions to shareholders, as share repurchases and dividends, increased to $17.3 billion in 3Q22, the most in the past five years (Figure 2). The E&P companies spent $9.0 billion on share repurchases and $8.3 billion on dividends, both five-year highs. Shareholder distributions as a percentage of cash from operations increased to 40% in 3Q22, after averaging 33% over the past three quarters, and being consistently lower than that in previous years. Dividends, which are typically steady from quarter to quarter, have grown 30% on average each quarter since the most recent low in 3Q20. A combination of increasing ordinary dividends, distributing special dividends (one-time payments that can share exceptional profits with shareholders), and some E&P companies adopting variable dividends (where a variable component based on a company’s cash flow adjusts quarterly dividend payouts) are contributing to higher dividends.

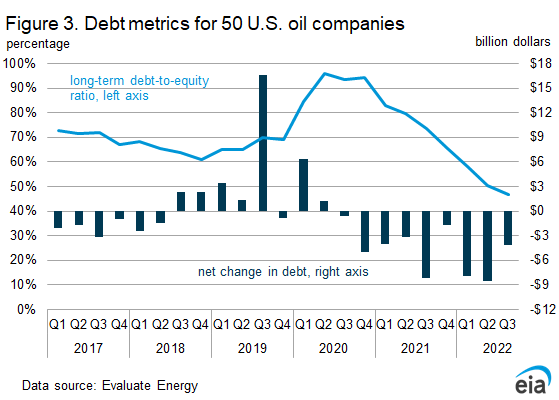

The E&P companies decreased their overall debt by $4.2 billion in the third quarter and lowered their long-term debt-to-equity ratio to 47%, the lowest in the past five years (Figure 3). The companies have collectively reduced debt in nine consecutive quarters, with a cumulative decline of $43.1 billion over the past two years. Typically, companies raise debt as a funding source for capital expenditure or merger and acquisition activity. Less-than-average capital expenditure over the past two years likely reduced the need to issue debt. More recently, the Federal Reserve’s interest rate increases have raised borrowing costs and could be discouraging companies from taking on new debt. These factors paired with stronger cash from operations have led the companies to hold less debt overall than in recent years; total debt is now below pre-pandemic levels. Some companies have paid off large acquisitions initially funded with debt. For example, Occidental Petroleum Corporation recorded a $17.0 billion net increase in debt in 3Q19 to finance their acquisition of Anadarko Petroleum Corporation. Since then, Occidental has recorded an $18.9 billion net decrease in debt, with $15.0 billion of that decrease taking place between 3Q21 and 3Q22. Reaching its debt target allowed Occidental to resume its share buyback program with a purchase of $3 billion in shares starting this summer. Less debt could explain recent increases in share repurchases and suggests a larger portion of cash from operations could be distributed to shareholders in the near term.

Publicly traded companies often publish future plans for their operations and spending, called company guidance, to help investors analyze company performance. Companies routinely release this information in corporate presentations, press releases, and official filings with the U.S. Securities and Exchange Commission. An analysis of company guidance for the 50 E&P companies shows that these companies spent an average of 10% more on capital expenditure over the past four years than they announced for guidance (Figure 4). Actual spending usually exceeds guidance because companies may not include asset acquisition spending in their guidance, but such transactions regularly occur each year. If actual spending this year matches the average deviation compared with company guidance over the past four years, capital expenditure by the E&P companies will increase 35% in 2022 compared with 2021. Supply chain constraints likely led to increased capital expenditure in 2022 due to higher material and labor costs needed to maintain production targets, in addition to increased drilling activity and oil production this year. As of December 9, 2022, only two companies in the dataset have provided guidance on capital expenditure for 2023.