Release Date: Jan. 11, 2022

Forecast Highlights

This edition of the Short-Term Energy Outlook (STEO) is the first to include forecasts for 2023.

The STEO continues to reflect heightened levels of uncertainty as a result of the ongoing COVID-19 pandemic. Notably, the Omicron variant of COVID-19 raises questions about global energy consumption. U.S. real GDP declined by 3.4% in 2020 from 2019 levels. Based on forecasts that use the IHS Markit macroeconomic model, we estimate U.S. GDP increased 5.7% in 2021 and that it will rise by 4.3% in 2022 and by 2.8% in 2023. In addition to macroeconomic uncertainties, uncertainty about winter weather and consumer energy demand also present a wide range of potential outcomes for energy consumption. Supply uncertainty in the forecast stems from uncertainty about OPEC+ production decisions and the rate at which U.S. oil and natural gas producers will increase drilling.

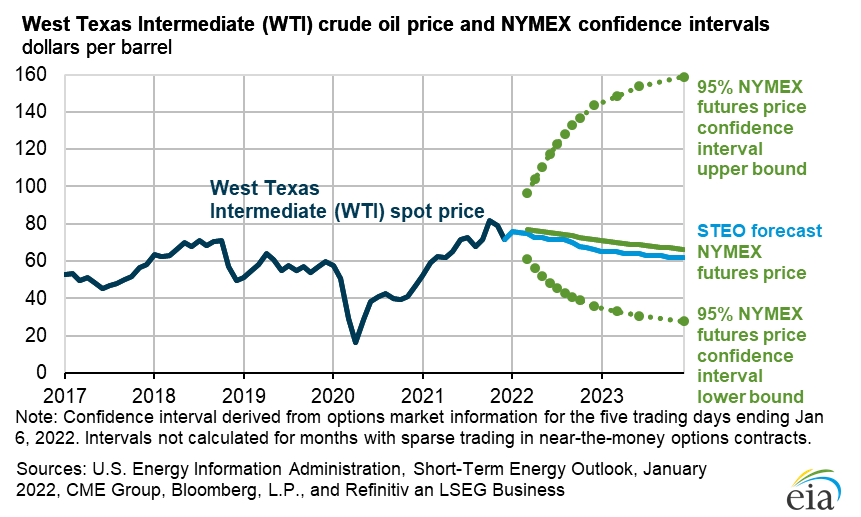

Brent crude oil spot prices averaged $71 per barrel (b) in 2021, and we forecast Brent prices will average $75/b in 2022 and $68/b in 2023.

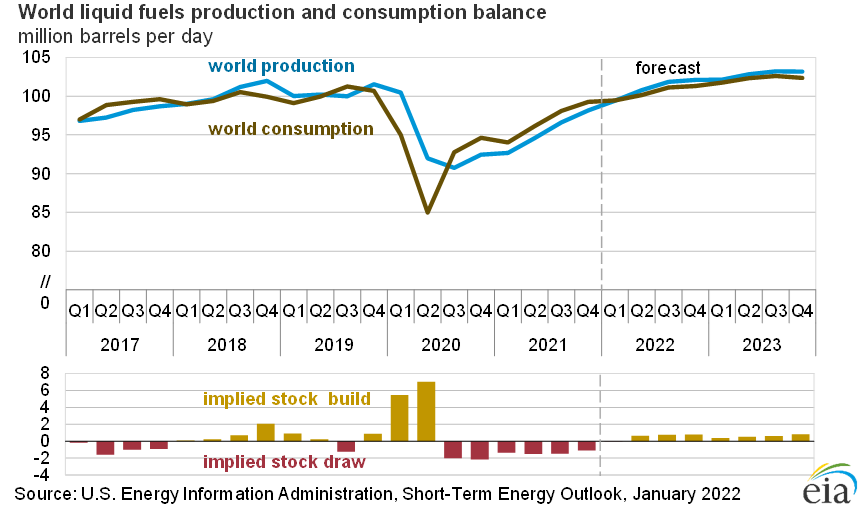

We estimate global liquid fuels inventories fell by an average of 1.4 million barrels per day (b/d) in 2021 compared with inventory growth of 2.1 million b/d in 2020. Global oil inventories rise in the forecast, increasing at a rate of 0.5 million b/d in 2022 and 0.6 million b/d in 2023.

Global consumption of petroleum and liquid fuels averaged 96.9 million b/d in 2021, up by 5.0 million b/d from 2020, when consumption fell significantly because of the pandemic. We expect global liquid fuels consumption will grow by 3.6 million b/d in 2022 and 1.8 million b/d in 2023.

Crude oil production from OPEC member countries averaged 26.3 million b/d in 2021, up from 25.6 million b/d in 2020. We forecast that average OPEC crude oil production will rise by 2.5 million b/d to average 28.8 million b/d in 2022 and average 28.9 in 2023.

U.S. crude oil production averaged 11.2 million b/d in 2021. We expect production to average 11.8 million b/d in 2022 and to rise to 12.4 million b/d in 2023, which would be the highest annual average U.S. crude oil production on record. The current record is 12.3 million b/d, set in 2019.

U.S. regular gasoline retail prices averaged $3.02 per gallon (gal) in 2021, compared with an average of $2.18/gal in 2020. We forecast gasoline prices will average $3.06/gal in 2022 and $2.81/gal in 2023. U.S. diesel fuel prices averaged $3.29/gal in 2021, compared with $2.56/gal in 2020, and we forecast diesel prices will average $3.33/gal in 2022 and $3.27/gal in 2023.

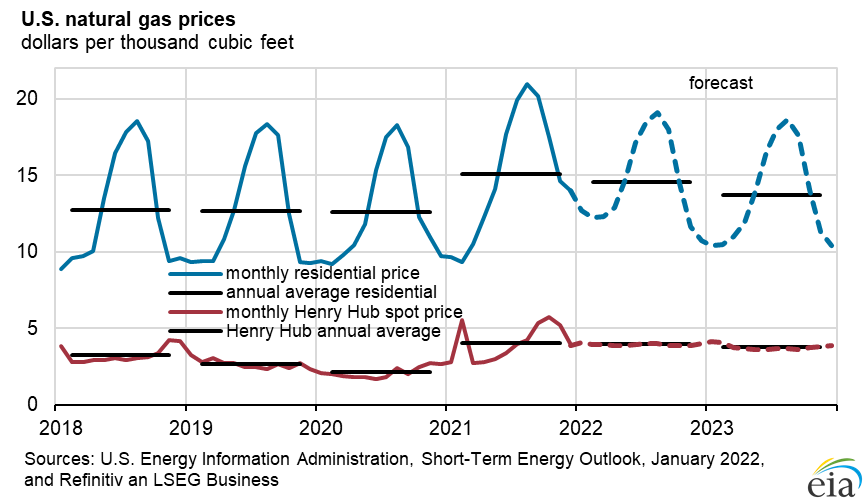

The natural gas spot price at Henry Hub averaged $3.91 per million British thermal units (MMBtu) in 2021. Monthly average prices reached $5.51/MMBtu in October, but they declined in November and December as mild weather prevailed across much of the country, resulting in less natural gas used for space heating. We expect Henry Hub spot prices will average $3.82/MMBtu in the first quarter of 2022 and average $3.79/MMBtu for all of 2022 and $3.63/MMBtu in 2023.

We estimate that U.S. liquefied natural gas (LNG) exports averaged 9.8 billion cubic feet per day (Bcf/d) in 2021, compared with 6.5 Bcf/d in 2020. We expect U.S. LNG export capacity increases will contribute to LNG exports averaging 11.5 Bcf/d in 2022 and 12.1 Bcf/d in 2023.

U.S. dry natural gas production averaged 93.5 Bcf/d in 2021, up 2.0 Bcf/d from 2020. Natural gas production in the forecast averages 96.0 Bcf/d for all of 2022 and then rises to 97.6 Bcf/d in 2023.

U.S. natural gas inventories ended December 2021 at 3.2 trillion cubic feet (Tcf), 3% more than the 2016–20 average. We forecast inventories will end March 2022 at 1.8 Tcf, which would be 8% more than the 2017–21 average for the end of March.