By Dr. Nancy Yamaguchi

The United States is emerging as a regional and global powerhouse in the petroleum sector. It was not all that long ago that the U.S. was expected to become more and more heavily dependent on imported oil. Forecasts of U.S. crude production all were pointing down. Production from mature domestic oilfields was declining, and the most oil-prospective areas remaining were in difficult or environmentally sensitive areas. On the other side of the equation, forecasts of oil demand continued to rise, resulting in a widening gap between supply and demand. This trend seemed the most likely for the future.

It is rare to witness a reversal of fortune on the scale of what has happened in the U.S. oil industry since then. The advent of hydraulic fracturing and horizontal drilling brought the “Shale Boom.” This has transformed the U.S. into one of the world’s top three oil producers, in the company of Saudi Arabia and Russia. The U.S. Energy Information Administration (EIA) reports that U.S. crude production rose to an average of 11.24 million barrels per day (mmbpd) during the third quarter of 2018. This places the U.S. in the number two spot, since the International Energy Agency (IEA) lists third quarter 2018 oil production from Saudi Arabia at 10.43 mmbpd and Russian output at 11.65 mmbpd.

Saudi Arabia and Russia currently are working to cut oil production to reduce global oversupply and strengthen prices. U.S. producers are under no such compulsion, and their output is expected to rise in 2019. The EIA forecasts that U.S. production will average 11.9 mmbpd in 2019. Already, there have been times when U.S. crude output has placed it in the number one spot globally, and there appears to be little reason to doubt that it could not claim this top spot on a more sustained basis in coming months.

We are calling this “A Reversal of Misfortune.” There is an element of judgement here: Is the reversal good fortune, bad fortune, or unknowable? In some countries, abundant resources have been detrimental to economic development. This is common enough to be known as “the resource curse.” Resource prices can swing wildly, making revenue projections impossible. If governments rely on a resource extraction economy, tax revenues can spike or plunge, possibly destabilizing entire regimes. When Norway discovered oil in the 1960s, the government declared ownership of the reserves, and many Norwegians worried that oil would ruin their government and their country. The fact that it did not was attributed to the presence of an already-established economy, a competent and forward-thinking government, and strong rule of law. The U.S. may share some of these qualities, but perhaps more importantly, there is no national oil company.

In the U.S., the oil industry is composed of numerous, long-established, companies. Also, the economy already was large and diverse before oil production began to rise again. The “resource curse” in the U.S. could take another shape, however, since the presence of abundant domestic oil may lengthen the fossil energy era and stifle investment in other energy technologies and prevent us from cutting carbon emissions. Indeed, we may be on the doorstep of innovations that will make fossil energy obsolete. Perhaps the shale boom will end because oil demand collapses. In that case, the resources will remain in the ground.

From a purely pragmatic point of view, the author’s perspective is: First, oil is valuable. It contains so much easily accessible energy, and it is so thoroughly entrenched in the modern world that it will take time to dethrone it. Second, that it is better to have it and not need it, than to need it and not have it. Good, bad or indifferent, the reversal in the U.S. oil balance has been astonishing. How significant are the impacts on trade?

Forecasts of U.S. Crude Import Requirements, Then and Now

Early each year, the EIA publishes its Annual Energy Outlook (AEO.) The AEO is the nation’s official long-term forecasting program. It is a massive data-gathering and computer-modeling exercise, covering a full range of energy supply, disposition, demand and price issues and projecting what might happen in coming decades given pre-determined scenario assumptions. The country’s oil sector has changed so dramatically that projections of the future are now wildly different than they once were.

The AEO2005 report noted that the U.S. crude oil imports had risen from 9.14 mmbpd in 2002 to 9.95 mmbpd in 2004. AEO2005 forecast an increase to 14.16 mmbpd of imports in the year 2017. This meant that oil imports were expected to rise by 3% per year from 2002 to 2017. Since then, the actual data now reveals that the import requirement fell to 7.97 mmbpd in 2017, amounting to a decrease of 1.9% per year over the fifteen-year period. The U.S. required 7.3 mmbpd less imported crude than had been expected.

To place this volume in context, Figure 1 compares the reduction in U.S. crude imports with the volume of crude exports by each OPEC country in 2017. The U.S. cut its projected crude import requirement by 7.3 mmbpd, a volume greater than the total exports of every single OPEC country, including Saudi Arabia, which exported 7 mmbpd in 2017. Obviously, the impact on the global oil market has been massive.

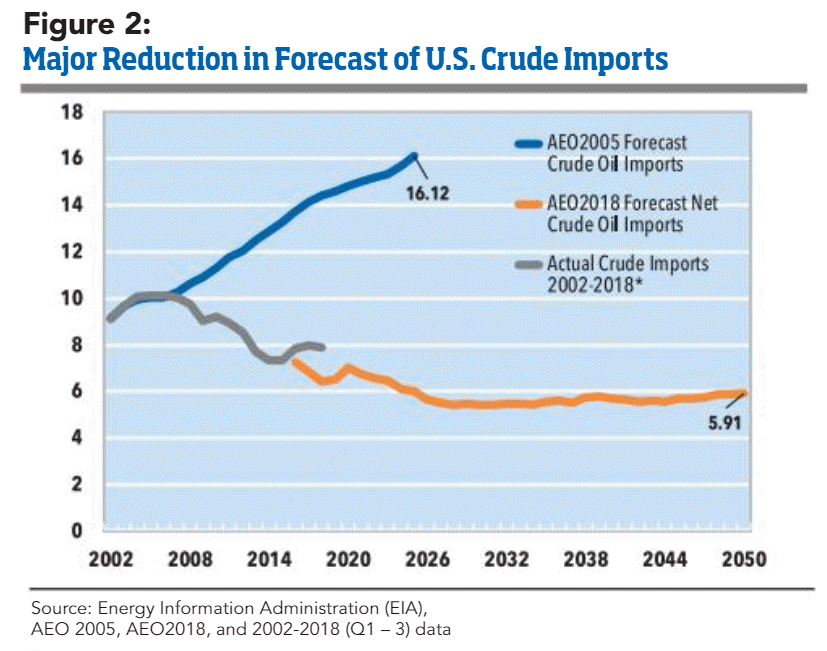

This chart presents a snapshot of 2017, but the projected change did not stop there. Figure 2 plots the AEO2005 forecast of the national crude import requirement to the year 2025, when the U.S. was expected to import 16.12 mmbpd of crude oil. Note the huge divergence between the AEO2005 forecast and the actual import volumes from 2002 through the first three quarters of 2018, as reported by the EIA.

Moving forward to the AEO2018 report, its forecast now calls for a crude import requirement of only 6.0 mmbpd in 2025, nearly 10.12 mmbpd less than what was projected by AEO2005. As time moves forward, U.S. crude import requirements are projected to fall below 6 mmbpd and to remain in this neighborhood for over thirty years. Imports are projected to be 5.91 mmbpd in the year 2050—a far cry from where they might have been if the trend seen in AEO2005 had continued. Extrapolating the AEO2005 line would have placed U.S. crude import requirements at over 33 mmbpd in the year 2050. Presumably, this type of demand would have stimulated investment by other oil producing countries, and it would have supported a much higher oil price than is seen today. But it is worth noting that 33 mmbpd is more than the sum of all OPEC exports in 2017.

Reversing the Downward Slide in U.S. Oil Production

As the U.S. becomes more and more of a powerhouse in the global oil market, is there anyone still among the living that worked in the early years of the industry? Figure 3 presents the long-term trend in U.S. crude production, beginning in the year 1900—one hundred and nineteen years ago. The U.S. was indeed the world’s oil superpower back then. Oil production grew from 0.174 mmbpd in 1900 to 9.637 mmbpd in 1970, a growth rate of 5.9% per year. This was the peak year of output. Production was sustained for a time as Alaskan crudes began to replace declining volumes from the lower 48 states, but by the mid-1980s, production began to decline steadily. Oil output dropped below 5 mmbpd in 2008.

For decades, our forecasts of oil production assumed that this downward trend would be permanent. The Shale Revolution turned this around. Oil production of 4.998 mmbpd in 2008 jumped to 10.761 mmbpd during the first ten months of 2018. This astonishing growth equates to an increase averaging 8% per year. Year 2018 output has smashed the prior record of 1970, which had held for forty-eight years.

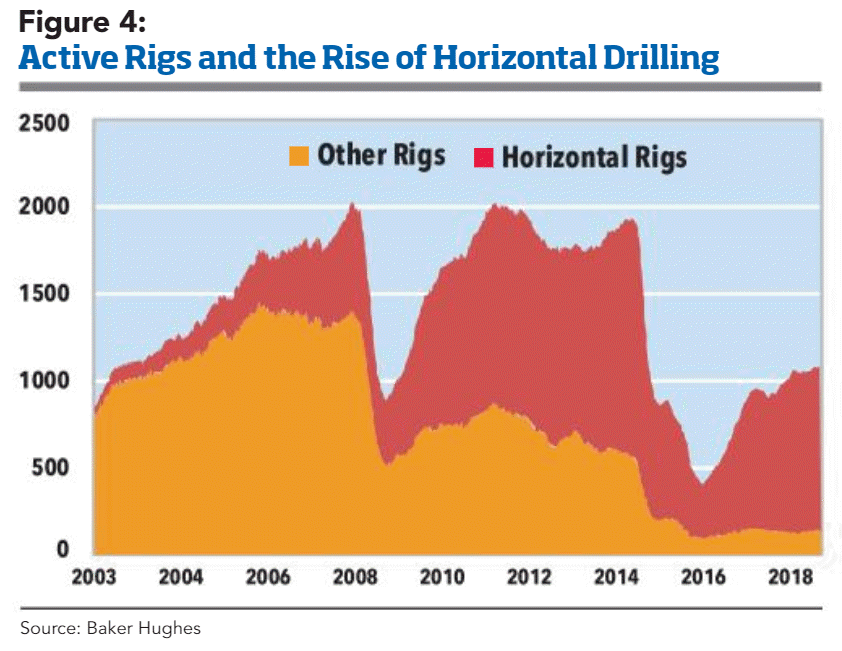

Reversing the downward trend was not a simple matter. Drilling for oil and gas is sensitive to price, time and location. Figure 4 displays the tremendous variability in the number of active oil and gas drilling rigs in the U.S. from 2003 through 2018. Oil prices were rising during the 2003 – 2008 period, and steady growth can be seen in the number of active rigs. But prices spiked in 2008, and the U.S., along with many other countries, slid into the Great Recession. The rig count was cut by more than half from over 2,000 in the summer of 2008 to less than 900 by mid-2009. The recession forced many companies to declare bankruptcy.

The second dramatic downturn in the U.S. active rig count can be seen after 2015. The turnaround in U.S. production began to erode the market share of OPEC exporters. Saudi Arabia had been cutting its production to keep the market balanced, but eventually this became a thankless task. Saudi Arabia began to ramp up production and launched a price war.

When the rig count began to recover in 2010, the growth was in horizontal drilling. In 2003, only around 6 – 7% of U.S. rigs were horizontal rigs. By 2010, horizontal rigs accounted for over half of the rig count. As of the first week of January 2019, 88% of the active rigs in the U.S. were horizontal rigs.

One of the most prolific and famous oil-producing regions is the Permian Basin in Texas. Figure 5 shows the rise and fall in the active rig count between 2007 and 2018. The rig count dropped from 265 in 2008 to 137 in 2009, in response to the Great Recession. The count then climbed to a peak of 536 rigs in 2014. It collapsed to 181 in 2016 in response to the Saudi-led oil price war. These were difficult years for the operators, but during this time, production efficiency soared. In 2007, each rig averaged 60 barrels per day of oil. When the rig count fell, the less-efficient rigs left the field first, and production per rig doubled to 123 bpd in 2010. Drilling efficiency rose to 588 bpd per rig in 2016 before leveling off. In 2018, the rig count had recovered to 463 active rigs, with an average production of 608 bpd each.

The U.S. Becomes a Major Oil Exporter

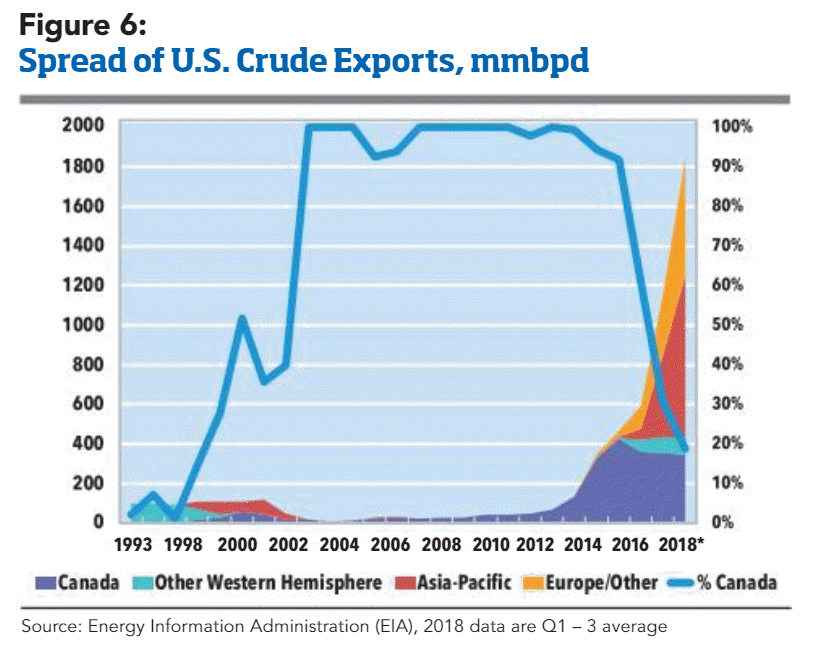

During the 1970s, the U.S. placed restrictions on exports of domestic crude oil, the idea at the time being that this would provide some sort of supply security. Certain exports were permitted, including exports to Canada, exports of crude from Alaska state waters and a specified volume of California heavy crude. As U.S. production began to rise, the export restrictions placed artificial barriers to trade, and oil from key shale plays created localized surpluses, driving down prices and creating inefficiencies.

The export restrictions finally were eliminated at the end of 2015. As Figure 6 illustrates, U.S. crude exports were unleashed beginning in 2016. Crude exports skyrocketed to 591 kbpd in 2016, jumped to 1158 kbpd in 2017 and rose to an average of 1843 kbpd during the first three quarters of 2018. The U.S. began shipping crude to far-flung destinations. During the 2000 – 2015 period, Canada usually was the destination for 95 – 100% of U.S. crude exports. In 2016, this share fell to 61%. It dropped to 31% in 2017, and it fell to just 19% during the first three quarters of 2018.

Although crude exports to Canada remain significant, during the first three quarters of 2018, the Asia-Pacific region has been the destination for nearly 45% of U.S. crude exports. China, Taiwan, India, South Korea and Japan have become major customers. Europe and other destinations accounted for 32% of U.S. crude exports, with large volumes being shipped to the United Kingdom, Italy and the Netherlands.

The U.S. also has an even larger role in exports of refined products, as shown in Figure 7. During the years when crude production was growing and restrictions were placed on its export, U.S. refineries with access to the inexpensive new crudes were running at very high rates of utilization to process the crude and export refined products instead. Product exports more than quintupled from around 1 mmbpd in 2003 to 5.5 mmbpd during the first three quarters of 2018.

The destinations for these exports also are diverse. During the first three quarters of 2018, Canada was the destination for 11% of U.S. refined product exports, while other Western Hemisphere countries accounted for 52% of U.S. exports. Mexico imported nearly 1.2 mmbpd of U.S. refined fuel. Other key destinations included Brazil, Ecuador, Peru, Panama, Venezuela and Argentina. Asia-Pacific countries accounted for 19% of U.S. product exports, including Japan, China, India, Indonesia and Singapore. Europe and other countries accounted for 18% of exports, including the Netherlands, the United Kingdom, Turkey and France.

Conclusion: A Reversal of (Mis)Fortune

The U.S. oil market has gone through some major cycles. It is difficult to believe that, a century or so ago, the U.S. was the world’s largest producer of oil. The public’s mind is more likely to recall the days of oil price spikes and perceived shortages. It is just as difficult to believe that the U.S. is emerging once again as the world’s number one oil producer (it most likely already occupies this spot), with crude oil exports and refined product exports growing and reaching consumers around the world.

Contrary to some sensationalist headlines, the U.S. is not a net exporter of crude oil. During the January – October period of 2018, the U.S. produced 10.76 mmbpd of crude, exported 1.89 mmbpd of crude and imported 7.85 mmbpd of crude. Nonetheless, this is a huge shift from where the country might have been. The AEO2005 forecasting exercise projected that crude imports would exceed 16 mmbpd in the year 2025. This projection was slashed to 6 mmbpd in the AEO2018 report. The impact on the global market is huge. Essentially, the U.S. as a customer was projected to buy 10 mmbpd of crude, and it has left the market, and the volume left behind is as much as the largest producers (the U.S., Russia and Saudi Arabia) can produce.

The resurgence of U.S. oil is a massive reversal of (mis)fortune, though in fairness, we cannot say that it is all good fortune. Fossil energy development and utilization place large tolls on the environment. Hydraulic fracturing is water-intensive, chemical-intensive and reinjection of fluids has caused seismic activity in some areas. Many believe that the fossil age is coming to a much-needed end at last. If U.S. oil production had continued to sink, and imports continued to soar, global oil prices would be higher today, and alternatives would be more competitive. The Shale Boom has delayed that. We can only reiterate that it is better to have it and not need it, than need it and not have it. If technological advancements make fossil energy obsolete, it can be left underground.

Nancy is an author and petroleum industry expert specializing in the advanced analysis of energy markets. Dr. Yamaguchi is the President of Trans-Energy Research Associates, Inc. focusing on a wide spectrum of fuel related issues such as economics and the environment. She possesses a strong interest in global oil industry including supply, demand, trading trends as well as transport, refining, product blending, alternative and reformulated fuels, product quality and price behavior. Dr. Yamaguchi can be reached at [email protected]

Nancy is an author and petroleum industry expert specializing in the advanced analysis of energy markets. Dr. Yamaguchi is the President of Trans-Energy Research Associates, Inc. focusing on a wide spectrum of fuel related issues such as economics and the environment. She possesses a strong interest in global oil industry including supply, demand, trading trends as well as transport, refining, product blending, alternative and reformulated fuels, product quality and price behavior. Dr. Yamaguchi can be reached at [email protected]