Distillate Fuel Oil Loses Volatility and Value

- Demand approaching 5-year October highs

- Stock levels are falling

- Refinery turnarounds ending

- IMO 2020 storage is growing

- Natural gas storage is 559 Bcf more than last year.

The Matrix

Crude oil prices ended October gasping for air. Volatility, a measure of swings in price changes (dispersion,) was low throughout the month. Low volatility reflected uncertainty in the markets because of difficult trade war negotiations between the United States and China and internally contradictory data reported in the EIA’s weekly Petroleum Balance Sheets for this time.

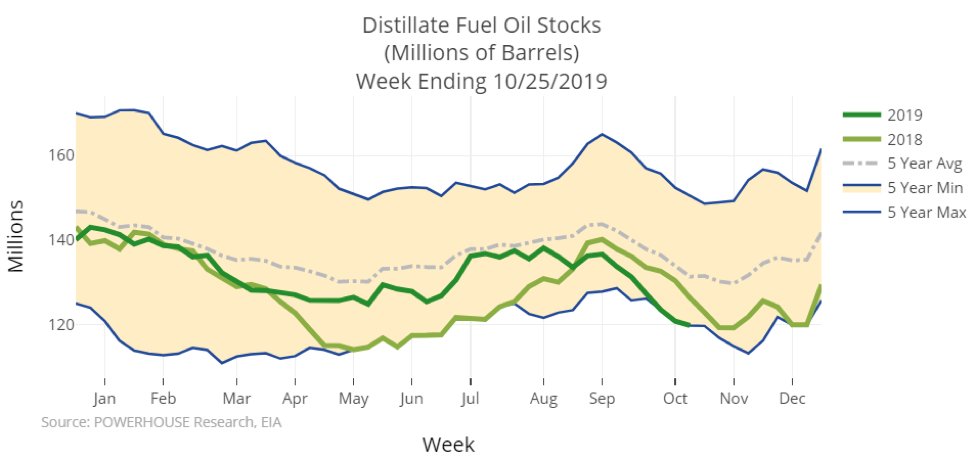

Distillate fuel oil volatility was low, as well. Data for distillate fuel oil painted a mixed picture. Demand, the principal driver of inventory change, clocked in at 4.3 million barrels daily for the week ending October 25. Distillate showed weekly growth of nearly 200,000 barrels daily and only 100,000 below the maximum use realized in the past five years. Demand at the current level should be bullish for price.

Distillate Stocks – 5 Year Chart 2015 – 2019 source: EIA, POWERHOSUE

Inventory levels for distillate fuel oil stocks fell. Stocks of 119.8 million barrels made a new five -year low for the report week. Supplies were one million barrels daily below the prior week’s level and 6.6 million barrels behind last year at this time. There are now 30.75 million fewer barrels than at the most recent five-year high.

Powerhouse’s Weekly Energy Market Situation published an analysis of distillate fuel oil supplies on October 14. Our analysis of the tightening global distillate fuel oil situation showed refinery turnaround as one explanation. Refinery use is starting to emerge from turnaround. DOE’s oil balance report showed utilization at 87.7 percent during the week ending October 25th, fully 2.5 percentage points higher than during the prior week. Traders should see this as bearish, as reflected in ULSD futures price.

Another ostensibly bullish factor for ULSD is the 2020 introduction of low sulfur fuels at sea. Uncertainty as to whether refiners could provide enough product to meet demand has supported prices but this concern has started to abate. Distillate fuel oil crack spreads, after a late summer/early autumn rally are starting to soften.

The end of autumn refinery maintenance and evidence of inventory in storage to meet the IMO 2020 initiative could contribute to the bearish performance of ULSD futures.

Supply/Demand Balances

Supply/demand data in the United States for the week ending Oct. 25, 2019, were released by the Energy Information Administration.

Total commercial stocks of petroleum fell by 2.2 million barrels during the week ending Oct. 25, 2019.

Commercial crude oil supplies in the United States increased by 5.7 million barrels from the previous report week to 438.9 million barrels.

Crude oil inventory changes by PAD District:

PADD 1: Plus 0.1 million barrels to 10.9 million barrels

PADD 2: Plus 1.6 million barrels to 131.5 million barrels

PADD 3: Plus 1.6 million barrels to 224.8 million barrels

PADD 4: Plus 1.0 million barrels to 22.6 million barrels

PADD 5: Plus 1.5 million barrels to 49.0 million barrels

Cushing, Oklahoma inventories rose 1.5 million barrels from the previous report week to 46.0 million barrels.

Domestic crude oil production was unchanged from the previous week at 12.6 million barrels per day.

Crude oil imports averaged 6.697 million barrels per day, a daily increase of 840,000 barrels. Exports fell 356,000 barrels daily to 3.327 million barrels per day.

Refineries used 87.7 percent of capacity, up 2.5% from the previous report week.

Crude oil inputs to refineries increased 133,000 barrels daily; there were 15.998 million barrels per day of crude oil run to facilities. Gross inputs, which include blending stocks, rose 475,000 barrels daily to reach 16.487 million barrels daily.

Total petroleum product inventories fell 7.9 million barrels from the previous report week.

Gasoline stocks decreased 3.0 million barrels daily from the previous report week; total stocks are 220.1 million barrels.

Demand for gasoline rose 194,000 barrels per day to 9.784 million barrels per day.

Total product demand increased 433,000 barrels daily to 21.597 million barrels per day.

Distillate fuel oil stocks decreased 1.0 million barrels from the previous report week; distillate stocks are at 119.8 million barrels. EIA reported national distillate demand at 4.263 million barrels per day during the report week, an increase of 187,000 barrels daily.

Propane stocks decreased 0.1 million barrels from the previous report week; propane stocks are 99.8 million barrels. The report estimated current demand at 1.001 barrels per day, an decrease of 276,000 barrels daily from the previous report week.

Natural Gas

A rally in natural gas futures is not being viewed as the start of an extended rally. Storage data show natural gas inventories are above average. Moreover, production continues to be strong notwithstanding low prices.

According to the Energy Information Administration:

Net injections into storage totaled 89 Bcf for the week ending October 25, compared with the five-year (2014–18) average net injections of 65 Bcf and last year’s net injections of 49 Bcf during the same week. Working gas stocks totaled 3,695 Bcf, which is 52 Bcf more than the five-year average and 559 Bcf more than last year at this time.

The average rate of net injections into storage is 27% higher than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 8.1 Bcf/d for the remainder of the refill season, total inventories would be 3,744 Bcf on October 31, which is 52 Bcf higher than the five-year average of 3,692 Bcf for that time of year.

Futures trading involves significant risk and is not suitable for everyone. Transactions in securities futures, commodity and index futures and options on future markets carry a high degree of risk. The amount of initial margin is small relative to the value of the futures contract, meaning that transactions are heavily “leveraged”. A relatively small market movement will have a proportionately larger impact on the funds you have deposited or will have to deposit: this may work against you as well as for you. You may sustain a total loss of initial margin funds and any additional funds deposited with the clearing firm to maintain your position. If the market moves against your position or margin levels are increased, you may be called upon to pay substantial additional funds on short notice to maintain your position. If you fail to comply with a request for additional funds within the time prescribed, your position may be liquidated at a loss and you will be liable for any resulting deficit. Past performance may not be indicative of future results. This is not an offer to invest in any investment program.

Powerhouse is a registered affiliate of Coquest, Inc.

Was this helpful? We’d like your feedback.

Please respond to [email protected]

Copyright© 2019 Powerhouse, All rights reserved.