Exclusive Analysis by Dr. Nancy Yamaguchi

June 19, 2020

Oil prices are bouncing back after last week’s retreat. West Texas Intermediate (WTI) crude prices have climbed back to the $40 a barrel level. Crude and refined product prices are trending up today. Last week’s retreat was prompted in part by the official declaration by the National Bureau of Economic Research (NBER) that the U.S. fell into economic recession in February, a sobering assessment by the Fed of the “long road” to economic recovery, and an alarming uptick in new COVID-19 cases. Yet the economic re-opening is continuing, and consumers are pumping money into the economy. Retail sales jumped 17.7%, fuel demand rose, and this week brought a surprising drawdown from oil inventories.

Fed Chair Jerome Powell stated that the Fed was expanding the ways it could increase market liquidity. Markets surged, indicating that most investors feel comfortable with the Fed expanding its ability to intervene. Investors also remain optimistic about the prospects for another stimulus plan that would spend $1 trillion on infrastructure, chiefly roads, bridges, and the 5G network. China has promised to pick up the pace on its promise to purchase more U.S. agricultural products. Trading today will be unpredictable, because of a quarterly event known as “quadruple witching.” As of this morning, however, markets are opening higher, and market bulls are outweighing market bears.

U.S. Department of Labor weekly data show 1.508 million initial jobless claims for the week ended June 13, a decrease of 58,000 from the prior week. This news came as a disappointment, shaking faith in a speedy recovery. The prior week’s figure was revised upward from 1.542 million to 1.566 million for the week ended June 6. There have been over 48.1 million unemployment claims so far this year, more than 45.7 million of them in the 13 weeks since COVID-19 shelter-in-place orders were launched.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have risen to 8,514,522, with 454,522 deaths. Confirmed cases in the U.S. rose to 2,191,200. U.S. deaths attributed to the disease have reached 118,435. Twenty-two states reported an increase in new COVID-19 cases. On the upbeat side, a clinical trial showed that dexamethasone (a common, inexpensive steroid) cut death rates by a third among the most severely ill patients.

WTI crude futures prices opened at $38.85 a barrel today, an increase of $2.59 a barrel (7.1%) from last Friday’s open of $36.26 a barrel. The week appears to be heading for a finish in the black. Our weekly price review covers hourly forward prices from Friday, June 12 through Friday, June 19. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

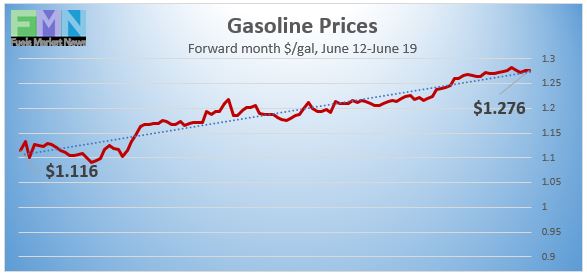

Gasoline Prices

Gasoline futures prices surged to open at $1.2654 per gallon today on the NYMEX, compared with $1.1142/gallon on June 12. This was a major gain of 15.12 cents (13.6%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April and May. U.S. average retail prices for gasoline rose significantly by 6.2 cents/gallon during the week ended June 15, after just last week reclaiming the territory above $2 per gallon. Retail prices averaged $2.098/gallon at the national level. Gasoline futures prices are rising today, trading in the range of $1.26/gallon to $1.29/gallon. The latest price is $1.2749/gallon.

Source: Prices as reported by DTN Instant Market

Diesel Prices

Diesel opened on the NYMEX today at $1.201/gallon, a strong increase of 11.61 cents, or 10.7%, from last Friday’s open of $1.0849/gallon. U.S. average retail prices for diesel rose by 0.7 cents per gallon during the week ended June 15 to average $2.403/gallon. Diesel prices have weakened more or less steadily this year, but crude and refined product prices appear to be in recovery. Diesel futures prices today are rising, and the week appears to be headed for a finish in the black. Currently, diesel is trading in the range of $1.20-$1.23/gallon. The latest price is $1.2253/gallon.

Source: Prices as reported by DTN Instant Market

WTI Crude Prices

WTI crude forward prices opened on the NYMEX today at $38.85 a barrel, compared with $36.26 a barrel last Friday. This was a gain of $2.59 a barrel (7.1%.) Last week brought a price retreat, motivated partly by a disturbing uptick in coronavirus cases and cautions from the Fed warning of a “long road” to economic recovery. COVID-19 continues to spread, but there is hope for a treatment. The Fed also broadened its ability to intervene in the market. Oil prices appear to be headed for a finish in the black. WTI prices are trading in the $39.00–$40.50 a barrel range currently. The latest price is $40.43 a barrel.

Source: Prices as reported by DTN Instant Market

PRICE MOVERS THIS WEEK: BRIEFING

Oil prices are bouncing back after last week’s retreat. West Texas Intermediate (WTI) crude prices have climbed back to the $40 a barrel level. Crude and refined product prices are trending up today. Last week’s retreat was prompted in part by the official declaration by the National Bureau of Economic Research (NBER) that the U.S. fell into economic recession in February, a sobering assessment by the Fed of the “long road” to economic recovery, and an alarming uptick in new COVID-19 cases. Yet the economic re-opening is continuing, and consumers are pumping money into the economy. Retail sales jumped 17.7%, fuel demand rose, and this week brought a surprising drawdown from oil inventories. The International Energy Agency (IEA) estimates that global oil demand will fall by 8.1 million barrels per day this year, but that demand will jump back by 5.7 mmbpd in 2021.

Fed Chair Jerome Powell stated that the Fed was expanding the ways it could increase market liquidity by purchasing individual corporate bonds, not just ETFs, using two credit facilities it established during the COVID-19 pandemic. Some have criticized this, saying that the Fed could buy “junk” debt of companies that have been downgraded since the COVID-19 pandemic. But the fact that markets surged indicates that most investors feel comfortable with the Fed expanding its ability to intervene in markets. Moreover, the Fed has pledged to put away these “tools” when the pandemic is over. Markets also remain optimistic about the prospects for another stimulus plan that would spend $1 trillion on infrastructure, chiefly roads, bridges, and the 5G network.

China has promised to pick up the pace on its pledge to purchase more U.S. corn, soybeans, and ethanol. Stock markets now are regaining most of what they lost last week. Trading today will be unpredictable, because of a quarterly event known as “quadruple witching” where options on futures and indexes are set to expire. As of this morning, however, markets are opening higher, and market bulls are outweighing market bears.

U.S. Department of Labor weekly data show 1.508 million initial jobless claims for the week ended June 13, a decrease of 58,000 from the prior week. This news came as a disappointment, shaking faith in a speedy recovery. The prior week’s figure was revised upward from 1.542 million to 1.566 million for the week ended June 6. There have been over 48.1 million unemployment claims so far this year, more than 45.7 million of them in the 13 weeks since COVID-19 shelter-in-place orders were launched.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have risen to 8,514,522, with 454,522 deaths. Confirmed cases in the U.S. rose to 2,191,200. U.S. deaths attributed to the disease have reached 118,435. Twenty-two states reported an increase in new COVID-19 cases. Some states have reported significant increases, including Arizona, Florida, Louisiana, Oklahoma, Alabama, South Carolina, Arkansas, Oregon, California, and Texas.

The World Health Organization (WHO) said it would update its guidelines on COVID-19 treatment following upbeat news about a possible treatment. A clinical trial showed that dexamethasone cut death rates by a third among the most severely ill patients. Dexamethasone is a common, inexpensive steroid used since the 1960s to reduce inflammation in diseases including arthritis.

Oil prices were largely unfazed midweek when the American Petroleum Institute (API) released information showing an addition of 3.9 mmbbls to crude oil stockpiles. The API also reported additions of 4.3 mmbbls to gasoline inventories and 0.919 mmbbls to diesel inventories. The API’s net inventory build was a significant 9.119 mmbbls. Market analysts had predicted builds of crude and diesel stocks but a drawdown from gasoline stockpiles.

Prices rose on Wednesday when U.S. Energy Information Administration (EIA) official statistics reported a much more bullish picture. The EIA reported a much smaller addition to crude oil stockpiles of 1.215 mmbbls, more than outweighed by stock drawdowns of 1.666 mmbbls of gasoline and 1.358 mmbbls of diesel. The EIA net result was an inventory draw amounting to 1.809 mmbbls. Crude oil inventories have expanded in 18 of the 23 weeks since the first week of January, sending a total of 112.32 mmbbls of crude oil into storage. The volume of crude flowing into stockpiles has slowed over the past month, however, as production is being cut and demand is picking up.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks steadily have been drained since then, falling to 46,836 mmbbls during the week ended June 12. Some surplus crude is being stored in the National Strategic Petroleum Reserve (SPR.) The EIA reports that SPR additions were made in the weeks ended April 24 (1.150 mmbbls), May 1 (1.716 mmbbls), May 8 (1.933 mmbbls), May 15 (1.882 mmbbls), May 22 (2.111 mmbbls), May 29 (4.02 mmbbls), June 5 (2.22 mmbbls), and June 12 (1.731 mmbbls), Current SPR stocks are 651.730 mmbbls.

U.S. crude production continues to decline. The EIA reported that U.S. crude production during the week ended June 12 declined to 10.5 mmbpd, down 0.6 mmbpd from 11.1 mmbpd the prior week. According to the EIA’s weekly data series, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd in April, 11.52 mmbpd in May, and 10.8 mmbpd during the first two weeks of June. The EIA has revised downward its forecast of 2020 production, cutting it to 11.56 mmbpd. However, the forecast of demand has been cut as well, leaving a supply overhang.