The oil complex is weakening today, after beginning the week holding well to last week’s gains. Reductions in oil inventories bolstered prices midweek. Now, West Texas Intermediate (WTI) crude oil futures are struggling to remain above the $42 a barrel level. Gasoline and diesel prices also are declining this morning, though gasoline prices appear to be holding on for a finish in the black, while diesel prices are heading for a finish in the red. Global stock markets are pointing down after European data revealed a pullback in economic activity in August after rosy data in July. Profit-taking on Wall Street is expected to pull U.S. markets down as well. Wall Street has been buoyed by exceptionally strong performance in the tech industry, but most other economic sectors have not recovered fully.

The jobs market received a setback this week. Initial weekly unemployment claims rose once again above the 1 million mark, after finally receding below that level last week. When last week’s claims finally fell below 1 million, optimism rose that the jobs market was recovering. Unfortunately, the Department of Labor reported that 1,106,000 people filed initial claims during the week ended August 15, an increase of 135,000 above last week’s upward-revised level of 971,000. During the 21 weeks since U.S. states began to issue shelter-in-place orders, 57.4 million Americans have filed initial jobless claims. The DOL reports that over 16 million people claim ongoing benefits.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have reached 22,707,352, with 794,256 deaths. Confirmed cases in the U.S. have risen to 5,576,089. U.S. deaths attributed to the disease have reached 174,290.

The OPEC+ group met this week to discuss the global oversupply and the production cut agreement. The cuts have been relaxed, but fine-tuning has been next to impossible. The group must cope with the huge drop in demand and the wide range of possibilities for demand recovery in coming months. Demand is not expected to recover to its pre-pandemic level this calendar year. Several countries did not comply with the cuts in May, June and July, and they now are being pressured to compensate by cutting production in August and September. Without a strong show of OPEC+ unity, oil prices will remain under pressure.

WTI crude futures prices opened at $42.33 a barrel today, up by $0.36 a barrel (0.9%) from last Friday’s open of $41.97 a barrel. Prices were strengthened midweek by across-the-board inventory draws and progress in reducing unemployment. Today, crude oil prices are weakening, and they are struggling to maintain the level above $42 a barrel. The week may finish with prices in the red. Our weekly price review covers hourly forward prices from Friday, August 14 through Friday, August 21. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

Source: Prices as reported by DTN Instant Market

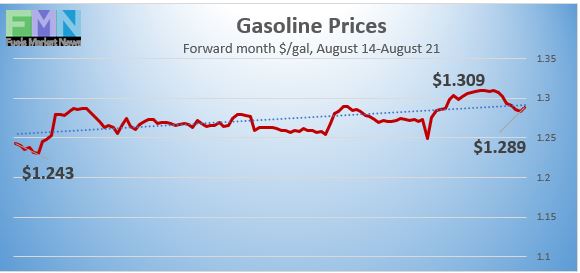

Gasoline Prices

Gasoline futures prices opened at $1.2981 per gallon today on the NYMEX, compared with $1.2364/gallon on Friday, August 14. This was a significant gain of 6.17 cents (5.0%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April and May. U.S. average retail prices for gasoline were unchanged at $2.166/gallon during the week ended August 17.

Ten weeks ago, retail prices reclaimed the territory above $2 per gallon. Gasoline futures prices have risen this week four out of five trading days, given an extra boost by unexpected drains on inventory. But prices now are falling off their previous highs. Currently, gasoline futures are trading in the range of $1.274/gallon to $1.311/gallon. The week appears to be heading for a finish in the black. The latest price is $1.2792/gallon.

Source: Prices as reported by DTN Instant Market

Diesel Prices

Diesel opened on the NYMEX today at $1.2471/gallon, up by 0.46 cents, or 0.4%, from last Friday’s open of $1.2425/gallon. U.S. average retail prices for diesel retreated by 0.1 cent per gallon during the week ended August 17 to average $2.427/gallon. Diesel prices generally have weakened this year, missing some of the price recovery see in crude and gasoline markets. Diesel futures prices rose midweek when inventory draws were announced, but prices trended up only modestly. Today, prices are retreating, and the week appears headed for a finish in the red. Currently, diesel is trading in the range of $1.212-$1.253/gallon. The latest price is $1.2157/gallon.

Source: Prices as reported by DTN Instant Market

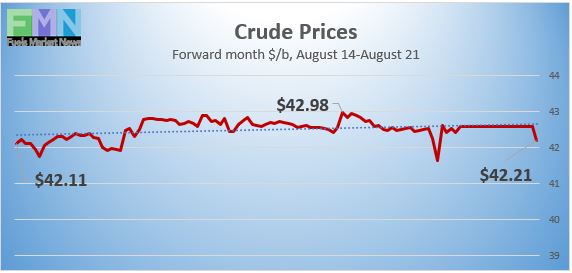

WTI Crude Prices

WTI crude forward prices opened on the NYMEX today at $42.75 a barrel, compared with $42.33 a barrel last Friday. This was a gain of $0.42 a barrel (0.9%.) Prices were stable through the middle of this week, supported by crude and product inventory draws. Over the past three weeks, WTI crude futures prices have solidified above $41 a barrel and even touched $43 a barrel, which has not happened for five months. Prices are trending down today, however, and WTI futures prices are dipping below $42 a barrel. The week may be heading for a finish with prices in the red. WTI crude is trading in the $41.94 to $42.96 a barrel range currently. The latest price is $42.04 a barrel.

PRICE MOVERS THIS WEEK: BRIEFING

The oil complex began this week holding week to last week’s gains, with midweek reductions in inventory bolstering prices. However, prices are weakening today. WTI crude oil futures are struggling to remain above the $42 a barrel level. Gasoline and diesel prices also are declining this morning, though gasoline prices appear to be holding on for a finish in the black, while diesel prices are heading for a finish in the red. Global stock markets are pointing down today after European data revealed a pullback in economic activity in August after rosy data in July. Profit-taking on Wall Street is expected to pull U.S. markets down as well. Wall Street has been buoyed by exceptionally strong performance in the tech industry, but most other economic sectors have not recovered.

The jobs market received a setback this week. Initial weekly unemployment claims rose once again above the one-million mark, after finally receding below that level last week. The Department of Labor reported that 1,106,000 people filed initial claims during the week ended August 15, an increase of 135,000 above last week’s upward-revised level of 971,000. (Last week’s reported level of 963,000 was revised up by 8,000.) During the week of March 28, initial jobless claims hit a peak of 6,867,000. From that peak, initial jobless claims fell for 15 weeks. July brought a setback, and claims rose again. When last week’s claims finally fell below one million, optimism rose that the jobs market was recovering, and there are hopes that this week’s setback will be reversed soon. During the 21 weeks since U.S. states began to issue shelter-in-place orders, 57.4 million Americans have filed initial jobless claims. The DOL reports that over 16 million people claim ongoing benefits.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have reached 22,707,352, with 794,256 deaths. Confirmed cases in the U.S. have risen to 5,576,089. U.S. deaths attributed to the disease have reached 174,290.

The OPEC+ group met this week to discuss the global oversupply and the production cut agreement. The cuts have been relaxed to 7.7 mmbpd, down from 9.7 mmbpd. Fine-tuning has been next to impossible, however, because of the huge drop in demand in the first part of the year and the wide range of possibilities for demand recovery in coming months. Demand is not expected to recover to its pre-pandemic level this calendar year. Several countries, including Iraq, Nigeria, Gabon, Angola, Russia and Kazakhstan, did not comply with the cuts in May, June, and July. Other countries over-complied. The non-complying countries now are being pressured to compensate by cutting production in August and September. Without this, oil prices are expected to remain under pressure.

Local fuel markets may be impacted in the next few days by two weather systems that are projected to strengthen into Tropical Storms or possibly even hurricanes. The first, designated Invest 97, is headed toward Texas. The second, Invest 98, is in the Caribbean and may hit Florida.

The American Petroleum Institute (API) released information this past Tuesday showing a significant drawdown from crude oil inventories, counteracted by a large addition to gasoline inventories. According to the API, 4.26 mmbbls of crude was drawn from stockpiles, along with 0.964 mmbbls from diesel stockpiles. In contrast, gasoline inventories surged by 4.991 mmbbls. The API’s net drain on inventories was a modest 0.233 mmbbls. Market analysts had predicted across-the-board drawdowns from crude and product inventories.

The U.S. Energy Information Administration (EIA) published official inventory data on Wednesday. While the crude oil drawdown was smaller than the API’s numbers, gasoline inventories fell rather than rose. The data can be viewed as more bullish than the API numbers. EIA statistics showed drawdowns of 1.632 mmbbls from crude oil inventories, 3.322 mmbbls from gasoline inventories, and a small addition of 0.152 mmbbls to diesel inventories. The EIA net result was an inventory drawdown of 4.802 mmbbls. Crude oil inventories have expanded in 21 of the 32 weeks since the first week of January, sending a total of 85.49 mmbbls of crude oil into storage.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks fell to 45,582 mmbbls during the week ended June 26. However, the downward trend was reversed in July through early August, sending Cushing stocks are back up to 53,289 mmbbls during the week ended August 7. The current week ended August 14 brought Cushing stocks down to 52,682 mmbbls.

During the week ended August 14, U.S. crude production remained unchanged at an average of 10.7 mmbpd. According to the EIA, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd in April, 11.52 mmbpd in May, and 10.9 mmbpd in June. Production in July rose to an average of 11.04 mmbpd. The decline to 10.7 mmbpd during the first week of August may signal the coming of a more serious decline, which could cause higher prices. The EIA reported that crude production in North Dakota dropped by 41.6% between December 2019 and May 2020. In total, U.S. production fell 21.9% between December 2019 and May 2020.