Happy New Year, and welcome back to Fuels Market Watch Weekly!

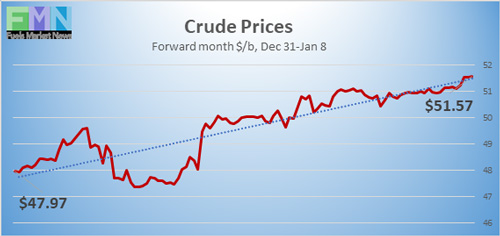

The past three weeks have been eventful—and outright tumultuous this week. This week’s violent assault on the U.S. Capitol was counterbalanced by congressional finalization of election results. Markets have been taking events in stride, with overall optimism and bullish factors tamping down bearish elements. The “Santa Claus Rally” did seem to appear as hoped for last week. This phenomenon looks at what happens during the last five days of December trading and the first two days of January trading, as though Santa comes to town on December 24 and returns to the North Pole on January 5. Some attribute the Santa Rally to holiday shopping and cheer, the spending of year-end bonuses, institutions squaring their books, traders taking vacations, and general optimism over the start of a new year. This year, the Santa Claus week brought a 0.87% increase in the Dow Jones Industrial Average relative to December 23. The S&P 500 rose nearly 1% relative to December 23, while the NASDAQ was up 0.375%. WTI crude futures prices opened at $50.93 a barrel today, an increase of $2.58 a barrel (5.3%) from last Thursday’s open of $48.35 a barrel. WTI futures prices have not opened above $50 a barrel since late February. Gasoline and diesel futures prices also rose strongly, and the oil complex is headed for a finish in the black this week.

Also supporting oil prices: Markets had been watching the OPEC+ group, since the group had been unable to agree on crude production ceilings. Russia and Kazakhstan argued for a collective increase of 500,000 bpd in February. Ultimately, it was decided that Russia will be allowed to increase its production by 65,000 bpd, and Kazakhstan will raise its production by 10,000 bpd in February and March. However, prices surged when Saudi Arabia announced that it would voluntarily cut its own output by one million bpd, more than compensating for the increases from other producers.

The emergency-use authorization for COVID-19 vaccines brought a wave of optimism last month. Most of this remains, but it is being tempered by disappointment in the slow pace of inoculation. Operation Warp Speed paved the way for vaccine approval and purchase, and the Trump Administration set a goal of 20 million vaccinations by the end of December 2020. However, Bloomberg News reported that only 5.46 million doses were administered. Federal and state agencies have been unable to optimize the logistics of delivering, storing and administering the shots. No state has been able to use all the vaccine it was sent; on the high end, South Dakota used 69% of the doses it received, and at the low end, Georgia managed to use only 22% of its supply. Dr. Anthony Fauci announced that this could be overcome, however, and that the U.S. could ramp up its capability toward a goal of being able to administer one million doses per day.

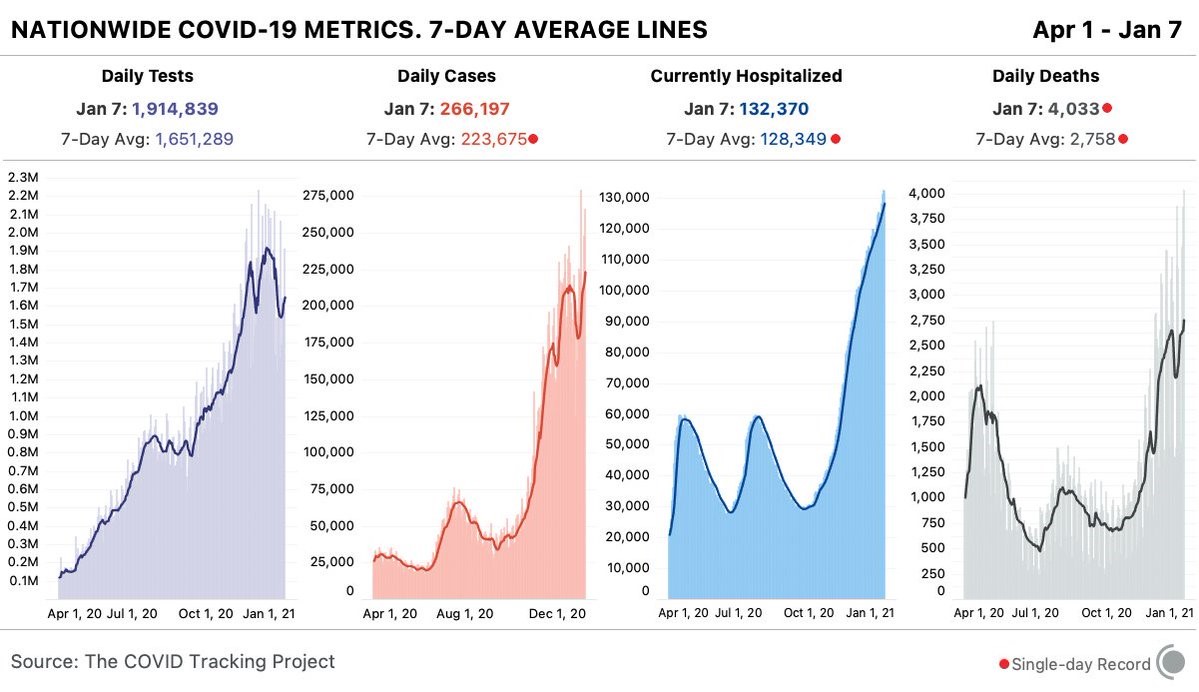

The U.S. continues to suffer ever-higher levels of COVID-19 infections, deaths, and hospitalizations. According to the COVID Tracking Project, new cases in the U.S. averaged 223,675 per day for the past seven days, a new record. Hospitalizations have continued to climb, and the seven-day average of 128,349 is also a new record. Daily deaths averaged 2,758 over the past seven days, yet another record, and the January 7 death toll of 4,033 was the highest number of daily deaths. This is the third, and worst, surge. Late-April brought a peak of 35,958 new daily cases. Mid-July brought a second peak of 76,550 new daily cases. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 stand at 88,203,229, with 1,901,510 deaths. The U.S. continues to lead the world with 21,589,666 cases and 365,448 deaths.

This morning, the U.S. Bureau of Labor Statistics released the Employment Situation Report for December 2020, also known as the Jobs Report. According to the BLS, “Total nonfarm payroll employment declined by 140,000 in December, and the unemployment rate was unchanged at 6.7 percent… The decline in payroll employment reflects the recent increase in coronavirus (COVID-19) cases and efforts to contain the pandemic. In December, job losses in leisure and hospitality and in private education were partially offset by gains in professional and business services, retail trade, and construction.”

Initial unemployment claims moved down by 3,000 last week, though because of an upward revision of 3,000 for the prior week. According to data collected by the Department of Labor, initial weekly unemployment claims fell by 3,000 during the week ended January 2, coming in at 787,000. The prior week’s figure was revised up by 3,000 to a total of 790,000. Initial weekly claims had finally subsided below the one-million mark at the end of August, but it took until mid-October before claims finally fell below 800,000. Prior to the pandemic, initial claims were typically 200,000–220,000 each week. During the 42 weeks since U.S. states began to issue shelter-in-place orders, approximately 73.8 million Americans have filed initial jobless claims.

U.S. jobs continue to be weighed down by the COVID-19 pandemic. Markets reacted with relief when Congress approved a $900 billion economic stimulus package on December 21. Stimulus checks of approximately $600 are en route. Democrats and President Trump had advocated for $2,000 checks, though the Republican-led Senate limited the amount to $600, mainly because of budgetary constraints. The newly installed Democratic leadership now is pressing for follow-up checks. This will create future problems with the deficit, but markets appear to favor the spend-now pay-later approach, the idea being that families need additional support until the pandemic can be brought under control.

WTI crude futures prices opened at $50.93 a barrel today, up by $2.58 a barrel (5.3%) from last Thursday’s open of $48.35 a barrel. WTI futures prices had a strong week, with Santa Claus rally gains, stimulus checks on the way, congressional certification of the presidential election, a crude inventory draw, and Saudi Arabia volunteering to cut crude production in February and March. WTI crude is trading in the range of $50.81-$51.83 a barrel currently. Prices are heading for a finish in the black this week. Our weekly price review covers hourly forward prices from Thursday, December 31 through Friday, January 8. Markets were closed on January 1. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

Source: Prices as reported by DTN Instant Market

Gasoline Prices

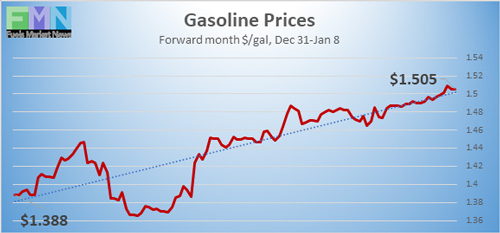

Gasoline futures prices opened at $1.4866 a gallon today on the NYMEX, compared with $1.3166 a gallon last Thursday (New Year’s Eve.) This was a major increase of 9.03 cents (6.5%.) It builds further upon strong gains achieved in December. U.S. average retail prices for gasoline rose by 0.6 cents to average $2.249/gallon during the week ended January 4. Gasoline futures contracts are trading in the range of $1.4831/gallon to $1.5134/gallon. This week is heading for a finish in the black. The latest price is $1.5129/gallon.

Source: Prices as reported by DTN Instant Market

Diesel Prices

Diesel opened on the NYMEX today at $1.5404/gallon, up by 5.14 cents, or 3.5%, from last Thursday’s open of $1.4891/gallon. Diesel futures prices have risen strongly for four consecutive weeks. U.S. average retail prices for diesel rose by 0.5 cents per gallon during the week ended January 4 to reach an average of $2.64/gallon. Diesel prices had been weakening significantly this year until November and December brought a price rebound. Currently, diesel futures prices are trending up, and the week is headed for a finish in the black. Contracts are trading in the range of $1.5379-$1.5672/gallon. The latest price is $1.5634/gallon.

Source: Prices as reported by DTN Instant Market

WTI Crude Prices

WTI crude futures prices opened at $50.93 a barrel today, an increase of $2.58 a barrel (5.3%) from last Thursday’s open of $48.35 a barrel. Markets were closed on Friday for the New Year’s Day holiday. WTI futures prices have not opened above $50 a barrel since late February. Prices continued to trend up this week, supported by overall market optimism, stock market gains, a crude oil inventory draw, OPEC+ production cuts, and the long-awaited confirmation of the new U.S. president. Additional federal stimulus is considered likely. The market optimism currently is overcoming some bearish fundamentals: the COVID-19 pandemic is worsening, and vaccinations are far behind schedule; oil demand is depressed; and unemployment is up. Futures contracts are trading in the range of $50.81-$51.83 a barrel currently. The week is headed for a finish in the black. The latest price is $51.67 a barrel.

PRICE MOVERS THIS WEEK: FULL BRIEFING

Happy New Year and welcome back to Fuels Market Watch Weeky!

The past three weeks have been eventful—and outright tumultuous this week. This week’s violent assault on the U.S. Capitol was counterbalanced by congressional finalization of election results. Markets have been taking events in stride, with overall optimism and bullish factors tamping down bearish elements. The “Santa Claus Rally” did seem to appear as hoped for last week. This phenomenon looks at what happens during the last five days of December trading and the first two days of January trading, as though Santa comes to town on December 24 and returns to the North Pole on January 5. Some attribute the Santa Rally to holiday shopping and cheer, the spending of year-end bonuses, institutions squaring their books, traders taking vacations, and general optimism over the start of a new year. This year, the Santa Claus week brought a 0.87% increase in the Dow Jones Industrial Average relative to December 23. The S&P 500 rose nearly 1% relative to December 23, while the NASDAQ was up 0.375%. WTI crude futures prices opened at $50.93 a barrel today, an increase of $2.58 a barrel (5.3%) from last Thursday’s open of $48.35 a barrel. WTI futures prices have not opened above $50 a barrel since late February. Gasoline and diesel futures prices also rose strongly, and the oil complex is headed for a finish in the black this week.

Also supporting oil prices: Markets had been watching the OPEC+ group, since the group had been unable to agree on crude production ceilings. Russia and Kazakhstan argued for a collective increase of 500,000 bpd in February. Ultimately, it was decided that Russia will be allowed to increase its production by 65,000 bpd, and Kazakhstan will raise its production by 10,000 bpd in February and March. Libya is not a participant in the production cut agreement. However, prices surged when Saudi Arabia announced that it would voluntarily cut its own output by one million bpd, more than compensating for the increases from other producers.

The emergency-use authorization for COVID-19 vaccines brought a wave of optimism last month. Most of this remains, but it is being tempered by disappointment in the slow pace of inoculation. Operation Warp Speed paved the way for vaccine approval and purchase, and the Trump Administration set a goal of 20 million vaccinations by the end of December 2020. However, Bloomberg News reported that only 5.46 million doses were administered. Federal and state agencies have been unable to optimize the logistics of delivering, storing and administering the shots. No state has been able to use all of the vaccine it was sent; on the high end, South Dakota used 69% of the doses it received, and at the low end, Georgia managed to use only 22% of its supply. Dr. Anthony Fauci announced that this could be overcome, however, and that the U.S. could ramp up its capability toward a goal of being able to administer one million doses per day.

The U.S. continues to suffer ever-higher levels of COVID-19 infections, deaths, and hospitalizations. According to the COVID Tracking Project, new cases in the U.S. averaged 223,675 per day for the past seven days, a new record. Hospitalizations have continued to climb, and the seven-day average of 128,349 is also a new record. Daily deaths averaged 2,758 over the past seven days, yet another record, and the January 7 death toll of 4,033 was the highest number of daily deaths. This is the third, and worst, surge. Late-April brought a peak of 35,958 new daily cases. Mid-July brought a second peak of 76,550 new daily cases. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 stand at 88,203,229, with 1,901,510 deaths. The U.S. continues to lead the world with 21,589,666 cases and 365,448 deaths.

This morning, the U.S. Bureau of Labor Statistics released the Employment Situation Report for December 2020, also known as the Jobs Report. According to the BLS, “Total nonfarm payroll employment declined by 140,000 in December, and the unemployment rate was unchanged at 6.7 percent… The decline in payroll employment reflects the recent increase in coronavirus (COVID-19) cases and efforts to contain the pandemic. In December, job losses in leisure and hospitality and in private education were partially offset by gains in professional and business services, retail trade, and construction.”

Initial unemployment claims moved down by 3,000 last week, though because of an upward revision of 3,000 for the prior week. According to data collected by the Department of Labor, initial weekly unemployment claims fell by 3,000 during the week ended January 2, coming in at 787,000. The prior week’s figure was revised up by 3,000 to a total of 790,000. Initial weekly claims had finally subsided below the one-million mark at the end of August, but it took until mid-October before claims finally fell below 800,000. Prior to the pandemic, initial claims were typically 200,000–220,000 each week. During the 42 weeks since U.S. states began to issue shelter-in-place orders, approximately 73.8 million Americans have filed initial jobless claims.

U.S. jobs continue to be weighed down by the COVID-19 pandemic. Markets reacted with relief when Congress approved a $900 billion economic stimulus package on December 21. Stimulus checks of approximately $600 are en route. Democrats and President Trump had advocated for $2,000 checks, though the Republican-led Senate limited the amount to $600, mainly because of budgetary constraints. The newly installed Democratic leadership now is pressing for follow-up checks. This will create future problems with the deficit, but markets appear to favor the spend-now pay-later approach, the idea being that families need additional support until the pandemic can be brought under control.

U.S. oil product demand remains anemic, and retail gasoline prices averaged just $2.17 per gallon in 2020, 44 cents (17%) lower than prices in 2019. The Energy Information Administration (EIA) this week reported that 2020 prices were the lowest on average since 2016. The EIA noted that vehicle travel in April dropped to its lowest monthly level on record, citing a Bureau of Transportation Statistics data series extending back to 2000.

U.S. oil inventories unexpectedly were drawn down during the week ended January 1. The U.S. Energy Information Administration (EIA) reported that crude oil inventories declined by 8.01 million barrels (mmbbls.) However, this was outweighed by additions of 4.519 mmbbls to gasoline inventories plus 6.39 mmbbls to diesel inventories. The EIA net result was an inventory build of 2.899 mmbbls. Although this was a net build, it was a more bullish result than the numbers reported earlier by the American Petroleum Institute (API.) The API had reported a crude stock draw of 1.663 mmbbls, overwhelmed by a gasoline stock build of 5.473 mmbbls and a distillate stock build of 7.136 mmbbls.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks fell to 45,582 mmbbls during the week ended June 26. However, the downward trend was reversed in July through early August, sending Cushing stocks back up to 53,289 mmbbls during the week ended August 7. Cushing stocks generally trended up over the past quarter. The most recent weekly data showed Cushing crude stocks at 59,202 mmbbls.

During the week ended January 1, U.S. crude production remained stable at 11.1 mmbpd. According to the EIA, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. The COVID-19 pandemic forced prices down. U.S. production fell to 12.25 mmbpd in April, 11.52 mmbpd in May, and 10.9 mmbpd in June. Production in July rose to an average of 11.04 mmbpd. In August, however, production fell to an average of 10.475 mmbpd before rising to 10.575 mmbpd in September. October production averaged 10.6 mmbpd, and December production climbed to 11.025 mmbpd. Along with impacts caused by the pandemic, this year’s production has varied because of record-breaking hurricanes.