Markets are in flux this week. Oil prices are off mid-week highs, yet are heading for another finish firmly in the black. Fundamentals are bearish, yet the market appears doggedly determined to look forward to 2021. The U.S. has for the first time in its history seen a president impeached twice, the COVID-19 pandemic appears at its direst, and unemployment has surged. Perhaps it is seen as a patient needing to get worse before being on the mend? President-elect Biden announced his plans for a massive $1.9 trillion stimulus package that will fund a major COVID-19 testing and vaccination program, provide $1,400 checks for individuals, boost and extend unemployment benefits, raise the minimum wage, and provide support for communities and small businesses. Markets appear to be banking on a more orderly transition to the Biden presidency and, although the proposed stimulus package has a hefty price tag, there is the sense that something must—and will—be done. WTI crude prices remain at the highest levels seen since last February. The U.S. Energy Information Administration (EIA) has just revised upwards its forecast of crude prices for 2021. In its January Short Term Energy Outlook (STEO,) the EIA forecasts that WTI crude spot prices will average $49.70 a barrel in 2021, whereas last month, the EIA had forecast a price of only $45.78 a barrel. The EIA forecasts that demand will increase from 18.06 million barrels per day (mmbpd) in 2020 to 19.51 mmbpd in 2021. The forecast price strength is attributed partly to OPEC+ production cuts in 2021, plus a forecast of only 11.1 mmbpd of crude production in the U.S., down from 11.29 mmbpd in 2020. Crude prices also have increased as the U.S. dollar index has decreased. Hefty inventories will place a lid on upward price movement, and the EIA forecasts that WTI prices will rise only modestly to $49.81 a barrel in 2022—an increase of only 11 cents above 2021’s forecast level.

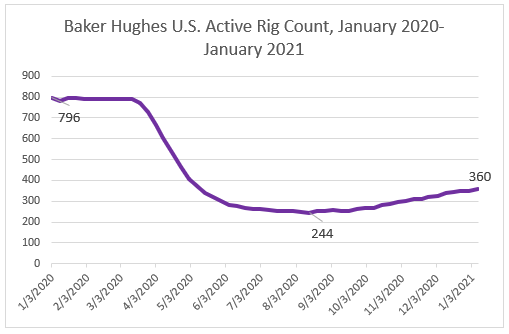

The active oil and gas rig count is a key indicator of industry perception. The Biden presidency is expected to be a mixed bag for the oil industry, but the president-elect has adopted a middle-of-the-road position. There is no fracking ban proposed. Mr. Biden has opposed fracking on federal lands only, and the vast majority of oil and gas is not produced on federal lands. As crude prices have recovered, the active rig count has crept back also. According to Baker Hughes, the active rig count plunged from 796 at the beginning of January 2020 to just 244 in August 2020. As of the week of January 8, the rig count had climbed back to 360. A year ago, WTI crude futures prices were over $60 a barrel. By April, prices had collapsed to around $20 a barrel. Prices rose gradually to the $38-$42 a barrel range thereafter, but they only reclaimed the territory above $50 a barrel this month.

The unemployment situation took a turn for the worse this week. According to data collected by the Department of Labor, initial unemployment claims spiked by 181,000 during the week ended January 9, rising to 965,000 from the prior week’s 784,000. Economists had anticipated claims to rise to only 795,000, so the news cast a pall on markets. Initial weekly claims had finally subsided below the one-million mark at the end of August, but it took until mid-October before claims finally fell below 800,000. By November, COVID-19 infections began to surge again, and initial unemployment claims began to climb. Prior to the pandemic, initial claims were typically 200,000–220,000 each week. During the 43 weeks since U.S. states began to issue shelter-in-place orders, approximately 74.8 million Americans have filed initial jobless claims.

The U.S. continues to suffer ever-higher levels of COVID-19 infections, deaths, and hospitalizations. According to the COVID Tracking Project, as of the week of January 14, deaths are 25% higher than any other week since the pandemic began. Approximately 130,000 COVID-19 patients are hospitalized. This is the third and most severe surge. Late-April brought a peak of 35,958 new daily cases. Mid-July brought a second peak of 76,550 new daily cases. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 stand at 93,235,680, with 1,996,948 deaths. The U.S. continues to lead the world with 23,314,898 cases and 388,709 deaths.

WTI crude futures prices opened at $53.80 a barrel today, up by $2.87 a barrel (5.6%) from last Friday’s open of $50.93 a barrel. WTI futures prices had a strong week, with a round of stimulus checks on the way, President-elect Biden’s proposal for a massive stimulus package, progress to come on mass vaccinations, and OPEC+ restraint on crude production. WTI crude is trading in the range of $52.63-$53.83 a barrel currently. Prices are heading down today, but weekly prices still are heading for a finish in the black. Our weekly price review covers hourly forward prices from Friday, January 8 through Friday, January 15. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

Source: Prices as reported by DTN Instant Market

Gasoline Prices

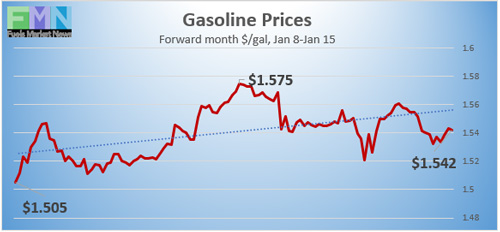

Gasoline futures prices opened at $1.5597 a gallon today on the NYMEX, compared with $1.4866 a gallon last Friday. This was a significant increase of 7.31 cents (4.9%.) It builds further upon strong gains achieved in December. U.S. average retail prices for gasoline rose by 6.8 cents to average $2.317/gallon during the week ended January 11. Gasoline futures contracts are moving down today, trading in the range of $1.5306/gallon to $1.5624/gallon. This week is heading for a finish in the black. The latest price is $1.5424/gallon.

Source: Prices as reported by DTN Instant Market

Diesel Prices

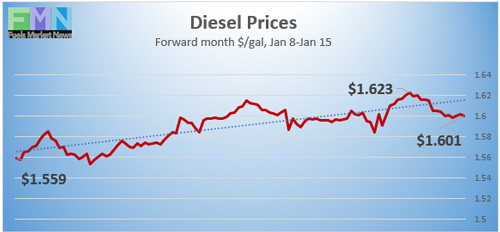

Diesel opened on the NYMEX today at $1.6201/gallon, up strongly by 7.96 cents, or 5.2%, from last Friday’s open of $1.5405/gallon. Diesel futures prices have risen significantly for five consecutive weeks. U.S. average retail prices for diesel rose by three cents per gallon during the week ended January 11 to reach an average of $2.67/gallon. Diesel prices had been weakening this year until November and December brought a price rebound. Currently, diesel futures prices are trending down, though the week is headed for a finish in the black. Contracts are trading in the range of $1.5941-$1.6235/gallon. The latest price is $1.5977/gallon.

Source: Prices as reported by DTN Instant Market

WTI Crude Prices

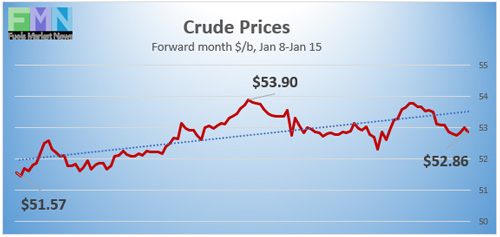

WTI crude futures prices opened at $53.80 a barrel today, an increase of $2.87 a barrel (5.6%) from last Friday’s open of $50.93 a barrel. WTI futures prices have not opened steadily above $50 a barrel since late-February. Prices reached 11-month highs this week, supported by overall market optimism, progress on COVID-19 vaccine logistics, President-elect Biden’s proposal for a massive stimulus package, OPEC+ production cuts, and a low U.S. Dollar index. Forward-looking market optimism is overcoming bearish fundamentals: the COVID-19 pandemic is worsening, demand is depressed; and unemployment claims unexpectedly spiked. Futures contracts are trading in the range of $52.68-$53.83 a barrel currently. The week is headed for a finish in the black. The latest price is $52.81 a barrel.

PRICE MOVERS THIS WEEK: FULL BRIEFING

Markets are in flux this week, with oil prices falling off mid-week highs, yet holding gains for another finish firmly in the black. Fundamentals are bearish, yet the market appears doggedly determined to look forward to 2021. The U.S. has for the first time in its history seen a president impeached twice, the COVID-19 pandemic appears at its direst, and unemployment has surged. Perhaps it is seen as a patient needing to get worse before being on the mend? President-elect Biden announced his plans for a massive $1.9 trillion stimulus package that will fund a major COVID-19 testing and vaccination program, provide $1,400 checks for individuals, boost and extend unemployment benefits, raise the minimum wage, and provide support for communities and small businesses. Markets appear to be banking on a more orderly transition to the Biden presidency and, although the proposed stimulus package has a hefty price tag, there is the sense that something must—and will—be done. WTI crude prices remain at the highest levels seen since last February. The U.S. Energy Information Administration (EIA) has just revised upwards its forecast of crude prices for 2021. In its January Short Term Energy Outlook (STEO), the EIA forecasts that WTI crude spot prices will average $49.70 a barrel in 2021, whereas last month, the EIA had forecast a price of $45.78 a barrel. The EIA forecasts that demand will increase from 18.06 million barrels per day (mmbpd) in 2020 to 19.51 mmbpd in 2021. The forecast price strength is attributed partly to OPEC+ production cuts in 2021, plus a forecast of only 11.1 mmbpd of crude production in the U.S., down from 11.29 mmbpd in 2020. Crude prices also have increased as the U.S. dollar index has decreased. Hefty inventories will place a lid on upward price movement, and the EIA forecasts that WTI prices will rise only modestly to $49.81 a barrel in 2022—an increase of only 11 cents above 2021’s forecast level.

The active oil and gas rig count is a key indicator of industry perception. The Biden presidency is expected to be a mixed bag for the oil industry, but he has adopted a middle-of-the-road position. There is no fracking ban proposed. Mr. Biden has opposed fracking on federal lands only, and the vast majority of oil and gas is not produced on federal lands. As crude prices have recovered, the active rig count has crept back also. According to Baker Hughes, the active rig count plunged from 796 at the beginning of January 2020 to just 244 in August 2020. As of the week of January 8, the rig count had climbed back to 360. A year ago, WTI crude futures prices were over $60 a barrel. By April, prices had collapsed to around $20 a barrel. Prices rose gradually to the $38-$42 a barrel range thereafter, but they only reclaimed the territory above $50 a barrel this month.

The unemployment situation took a turn for the worse this week. According to data collected by the Department of Labor, initial unemployment claims spiked by 181,000 during the week ended January 9, rising to 965,000 from the prior week’s 784,000. Economists had anticipated claims to rise to only 795,000, so the news cast a pall on markets. Initial weekly claims had finally subsided below the one-million mark at the end of August, but it took until mid-October before claims finally fell below 800,000. By November, unfortunately, COVID-19 infections began to surge again, and initial unemployment claims began to climb. Prior to the pandemic, initial claims were typically 200,000–220,000 each week. During the 43 weeks since U.S. states began to issue shelter-in-place orders, approximately 74.8 million Americans have filed initial jobless claims.

The U.S. continues to suffer ever-higher levels of COVID-19 infections, deaths, and hospitalizations. According to the COVID Tracking Project, as of the week of January 14, deaths are 25% higher than any other week since the pandemic began. Approximately 130,000 COVID-19 patients are hospitalized. This is the third and most severe surge. Late-April brought a peak of 35,958 new daily cases. Mid-July brought a second peak of 76,550 new daily cases. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 stand at 93,235,680, with 1,996,948 deaths. The U.S. continues to lead the world with 23,314,898 cases and 388,709 deaths.

U.S. crude oil inventories were drawn down during the week ended January 8, though the additions to gasoline and diesel inventories outweighed the draw. The EIA reported that crude oil inventories were drawn down by 3.248 million barrels (mmbbls.) This was outweighed by additions of 4.395 mmbbls to gasoline inventories plus 4.786 mmbbls to diesel inventories. The EIA net result was an inventory build of 5.933 mmbbls. This was a more bearish result than the numbers reported earlier by the American Petroleum Institute (API.) The API had reported a crude stock draw of 5.8 mmbbls, a gasoline stock build of 1.9 mmbbls and a distillate stock build of 4.4 mmbbls.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 barrels during the week ended January 3, 2020, to 65,446 barrels during the week ended May 1, 2020, an increase of 29,124 barrels. Cushing stocks trended up during the fourth quarter of 2020. The most recent weekly data showed Cushing crude stocks at 57,227 mmbbls.

During the week ended January 8, U.S. crude production remained stable at 11.1 mmbpd. According to the EIA, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. The COVID-19 pandemic forced prices down. U.S. production fell to 12.25 mmbpd in April, 11.52 mmbpd in May, and 10.9 mmbpd in June. Production in July rose to an average of 11.04 mmbpd. In August, however, production fell to an average of 10.475 mmbpd before rising to 10.575 mmbpd in September. October production averaged 10.6 mmbpd, and December production climbed to 11.025 mmbpd.