Oil prices eased early this week, unable to recoup last week’s losses, but buying interest is picking up today. Gasoline and diesel prices are rising faster than crude prices, and they appear to be heading for a finish in the black, while crude prices may finish flat. Markets doggedly have retained an unusually high level of optimism that drove oil prices up for five consecutive weeks until last week’s downturn. This came despite continued bearish fundamentals. Perhaps it is a good sign that, for each piece of bearish news, a bright side can be found. For example, three new variants of coronavirus have made their way to the U.S., as the vaccine rollout forges ahead, and nearly every state has reported reduced rates of infections and hospitalizations. U.S. GDP in 2020 dropped by the largest amount since 1946, yet the year 2021 is expected to bring back growth. Fuel demand collapsed, especially for jet fuel, but diesel and gasoline now are climbing back up. Unemployment remains severe, but initial jobless claims last week were lower than forecast. Today, stock markets may be volatile as concerns grow over the new coronavirus variants and as the GameStop (etc.) stock rollercoaster continues. Even with last week’s price decline and the flat performance this week, WTI crude prices remain close to $53 a barrel, a price level not seen since last February.

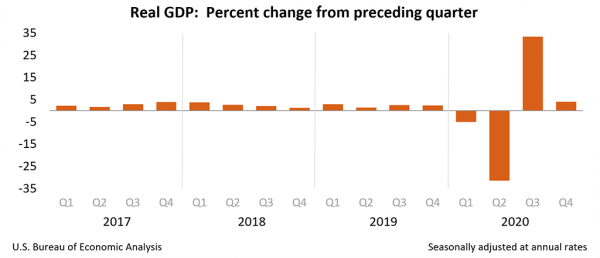

As January draws to a close, more information is becoming available concerning last year’s economic malaise. Yesterday, the U.S. Bureau of Economic Analysis (BEA) released advance estimate data on GDP for the fourt quarter and full-year 2020. The BEA calculates that real GDP in 2020 decreased 3.5% relative to its level in 2019. This was the first time the economy shrank since the year 2009, when GDP dropped by 2.5% during the Great Recession. It was the worst year for the economy since 1946, when wartime demobilization caused the economy to shrink by 11.6%. In 2019, real GDP increased modestly by 2.2%, falling short of the government’s 3% goal. The fourth quarter showed a 4% increase, equating to 1% growth when annualized. Fourth-quarter GDP growth rate was disappointing, but it helped build upon the third-quarter bounce-back of 33.4%. The amount of economic growth in the second half of the year was not sufficient to overcome the drop suffered in the first half of the year. According to the BEA: “The decrease in real GDP in 2020 reflected decreases in PCE, exports, private inventory investment, nonresidential fixed investment, and state and local government that were partly offset by increases in federal government spending and residential fixed investment. Imports decreased.”

The unemployment situation remains severe, but initial jobless claims are heading down. According to data collected by the Department of Labor, 847,000 people filed initial unemployment claims during the week ended January 23, down significantly by 67,000 from the prior week’s revised level of 914,000. Initial weekly claims had finally subsided below the one-million mark at the end of August, but it took until mid-October before claims finally fell below 800,000. By November, COVID-19 infections began to surge again, and initial unemployment claims rose. Prior to the pandemic, initial claims were typically 200,000–220,000 each week. During the 44 weeks since U.S. states began to issue shelter-in-place orders, nearly 75.7 million Americans have filed initial jobless claims.

Federal Reserve Chair Jerome Powell said this week: “There’s nothing more important to the economy right now than people getting vaccinated.” The Fed met this week, leaving interest rates unchanged and renewing commitment to supporting economic recovery. Chairman Powell continued, “That is really the main thing about the economy, is getting the pandemic under control, getting everyone vaccinated, getting people wearing masks and all that. That’s the single most important economic growth policy that we can have.”

The U.S. continues to battle the COVID-19 pandemic, but outbreaks at last are easing. According to the COVID Tracking Project, nearly every state is making progress, and last week’s data showed a 17% drop in new cases and a 10% drop in hospitalizations. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 crossed the 100-million mark, standing at 101,582,467, with 2,193,844 deaths. The U.S. continues to lead the world with 25,769,183 cases and 433,223 deaths. The Centers for Disease Control (CDC) reports that, as of January 28, 48,386,275 doses of vaccine have been distributed, with 26,193,682 doses administered.

WTI crude futures prices opened at $52.15 a barrel today, down by $0.95 a barrel (1.8%) from last Friday’s open of $53.10 a barrel. This is the second week that WTI futures prices have fallen, finally dropping back after rising for five consecutive weeks. Markets may be stabilizing after rising swiftly. Progress finally is being made in battling the COVID-19 pandemic, with some economic recovery expected in 2021 after 2020’s contraction of 3.5%—the worst since 1946. WTI crude is trading in the range of $51.93-$53.25 a barrel currently. Prices have recovered today, and the week appears to be heading for a flattish finish. Our weekly price review covers hourly forward prices from Friday, January 22 through Friday, January 29. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

Gasoline Prices

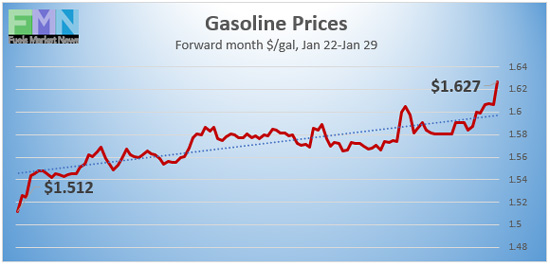

Gasoline futures prices opened at $1.5806 a gallon today on the NYMEX, compared with $1.5509 a gallon last Friday. This was an increase of 2.97 cents (1.9%,) which more than recaptured the prior week’s downturn of 0.88 cents. Before last week, prices had been rising for five consecutive weeks. U.S. average retail prices for gasoline rose by 1.3 cents to average $2.392/gallon during the week ended January 25. Gasoline futures prices rose this morning, trading in the range of $1.5806/gallon to $1.6293/gallon. Contracts are moving to the next forward month. This week appears to be heading for a finish in the black. The latest price is $1.6214/gallon.

Diesel Prices

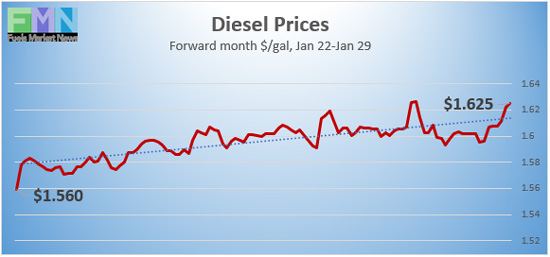

Diesel opened on the NYMEX today at $1.5983/gallon, down slightly by 0.3 cents, or 0.2%, from last Friday’s open of $1.6013/gallon. Until last week, diesel futures prices had risen for five consecutive weeks. After last week’s downturn, prices are picking up today. U.S. average retail prices for diesel rose by 2.0 cents per gallon during the week ended January 25 to reach an average of $2.716/gallon. Diesel prices had been weakening this year until November and December brought a price rebound, with most of the gains being held in January. Currently, diesel futures prices are rising. The week appears to be headed for a finish in the black. Contracts are trading in the range of $1.5951-$1.6357/gallon. Contracts are moving to the next forward month. The latest price is $1.6226/gallon.

WTI Crude Prices

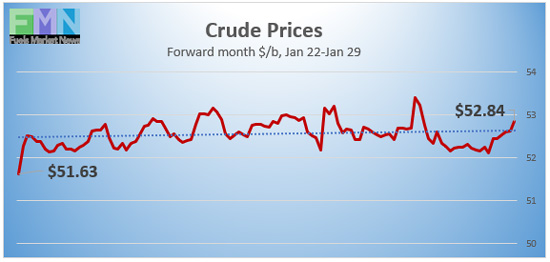

WTI crude futures prices opened at $52.15 a barrel today, down by $0.95 a barrel (1.8%) from last Friday’s open of $53.10 a barrel. This is the second week that prices fell relative to the prior week, handing back some gains after five weeks of strong upward momentum. However, WTI futures rose this morning, and prices may regain the $53 a barrel level. Recently, prices have been propelled by market optimism that seem overweighted, given bearish fundamentals and the long road ahead toward beating the pandemic and restoring the economy. Still, progress is being made. Nearly all states are showing improvement in battling the pandemic, and a new one-dose vaccine is on the way. The economy shrank by 3.5% in 2020, but it is forecast to grow in 2021. Futures contracts are trading in the range of $51.93-$53.25 a barrel currently. Crude prices are creeping back up after stagnating all week. The week may finish slightly in the red. The latest price is $52.91 a barrel.

PRICE MOVERS THIS WEEK: FULL BRIEFING

Oil prices eased early this week, unable to recoup last week’s losses, but buying interest is picking up today. Gasoline and diesel prices are rising faster than crude prices, and they appear to be heading for a finish in the black, while crude prices may finish flat. Markets doggedly have retained an unusually high level of optimism that drove oil prices up for five consecutive weeks until last week’s downturn. This came despite continued bearish fundamentals. Perhaps it is a good sign that, for each piece of bearish news, a bright side can be found. For example, three new variants of coronavirus have made their way to the U.S., yet the vaccine rollout is forging ahead, and nearly every state has reported reduced rates of infections and hospitalizations. U.S. GDP in 2020 dropped by the largest amount since 1946, yet the year 2021 is expected to bring back growth. Fuel demand collapsed, especially for jet fuel, yet diesel and gasoline are climbing back up. Unemployment remains severe, but initial jobless claims last week were lower than forecast. Today, stock markets may be volatile as concerns grow over the new coronavirus variants and as the GameStop (etc.) stock rollercoaster continues. Even with last week’s price decline and the flat performance this week, WTI crude prices remain close to $53 a barrel, a price level not seen since last February.

As January draws to a close, more information is becoming available concerning last year’s economic malaise. Yesterday, the U.S. Bureau of Economic Analysis (BEA) released advance estimate data on GDP for the fourth quarter and full-year 2020. The BEA calculates that real GDP in 2020 decreased 3.5% relative to its level in 2019. This was the first time the economy shrank since the year 2009, when GDP dropped by 2.5% during the Great Recession. It was the worst year for the economy since 1946, when wartime demobilization caused the economy to shrink by 11.6%. In 2019, real GDP increased modestly by 2.2%, falling short of the government’s 3% goal. The fourth quarter showed a 4% increase, equating to 1% growth when annualized. Fourth-quarter GDP growth rate was disappointing, but it helped build upon the third-quarter bounce-back of 33.4%. The amount of economic growth in the second half of the year was not sufficient to overcome the drop suffered in the first half of the year. According to the BEA: “The decrease in real GDP in 2020 reflected decreases in PCE, exports, private inventory investment, nonresidential fixed investment, and state and local government that were partly offset by increases in federal government spending and residential fixed investment. Imports decreased.”

The unemployment situation remains severe, but initial jobless claims are heading down. According to data collected by the Department of Labor, 847,000 people filed initial unemployment claims during the week ended January 23, down significantly by 67,000 from the prior week’s revised level of 914,000. Initial weekly claims had finally subsided below the one-million mark at the end of August, but it took until mid-October before claims finally fell below 800,000. By November, COVID-19 infections began to surge again, and initial unemployment claims rose. Prior to the pandemic, initial claims were typically 200,000–220,000 each week. During the 44 weeks since U.S. states began to issue shelter-in-place orders, nearly 75.7 million Americans have filed initial jobless claims.

Federal Reserve Chair Jerome Powell said this week: “There’s nothing more important to the economy right now than people getting vaccinated.” The Fed met this week, leaving interest rates unchanged and renewing commitment to supporting economic recovery. Chairman Powell continued, “That is really the main thing about the economy, is getting the pandemic under control, getting everyone vaccinated, getting people wearing masks and all that. That’s the single most important economic growth policy that we can have.”

The U.S. continues to battle the COVID-19 pandemic, but outbreaks at last are easing. According to the COVID Tracking Project, nearly every state is making progress, and last week’s data showed a 17% drop in in new cases and a 10% drop in hospitalizations. The Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 crossed the 100-million mark, standing at 101,582,467, with 2,193,844 deaths. The U.S. continues to lead the world with 25,769,183 cases and 433,223 deaths. The Centers for Disease Control (CDC) reports that, as of January 28, 48,386,275 doses of vaccine have been distributed, with 26,193,682 doses administered.

U.S. crude oil inventories were drawn down significantly this week, lending support to oil prices. The Energy Information Administration (EIA) reported a drawdown of 9.91 million barrels (mmbbls) from crude oil inventories, plus a small draw of 0.815 mmbbls from distillate inventories. Gasoline stocks rose by 2.469 mmbbls. The net drawdown was 8.256 mmbbls. The American Petroleum Institute (API) earlier had reported a crude stock draw of 5.272 mmbbls, a gasoline stock build of 3.058 mmbbls and a distillate stock build of 1.398 mmbbls.

U.S. crude oil production declined slightly last week, falling from 11.0 million bpd to 10.9 million bpd. For the first four weeks of January 2021, production averaged 10.975 mmbpd, 2 mmbpd lower than the 12.975 achieved during the first four weeks of January in 2020. Apparent demand this month to date is 0.888 mmbpd below its level of one year ago.