Oil prices are trailing down today, a downward correction after a four-week period of price recovery. Over the previous four weeks, crude prices regained around $17 a barrel—essentially doubling in value from approximately $17 a barrel to $34 a barrel. The prospect of a phased lifting of shelter-in-place rules inspired market bulls. Currently, however, prices are being pressured by increased tension between the U.S. and China, and international markets are awaiting new actions. China is citing national security as the rationale for moving forward with legislative control over Hong Kong, which is setting off new protests. The U.S. immediately opposed the plan, stating that increased Chinese control would eliminate Hong Kong’s special trade status with the U.S.

Today, West Texas Intermediate (WTI) crude prices are hovering around $33 a barrel. U.S. President Donald Trump is scheduled to hold a press conference on China today, and markets are wary that the U.S. may impose sanctions on China. This would further complicate negotiations in the ongoing U.S.-China trade war. Both countries are under considerable stress because of the COVID-19 pandemic, for which President Trump holds China largely responsible.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have risen to 5,840,369, with 361,066 deaths. Confirmed cases in the U.S. rose to 1,721,926. U.S. deaths attributed to the virus have reached 101,621. This grim total now surpasses the number of U.S. casualties in the Vietnam War and the Korean War combined.

The U.S. economic recovery will take time, particularly with unemployment at such staggering levels. U.S. Department of Labor weekly data show 2.123 million initial jobless claims for the week ended May 23. There have been nearly 43.2 million unemployment claims over the past ten weeks.

WTI crude futures prices opened at $33.68 a barrel today, a decline of 0.8% from last Friday’s open of $33.95 a barrel. The week may finish in the red, after a four-week upward trend. Nonetheless, prices of over $30 a barrel may be considered strong, given that just a month ago, oil prices were dipping below $10 a barrel, and there were concerns about negative oil prices reappearing. Our weekly price review covers hourly forward prices from Friday, May 22 through Friday, May 29. This includes the Memorial Day holiday, for which markets were closed. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

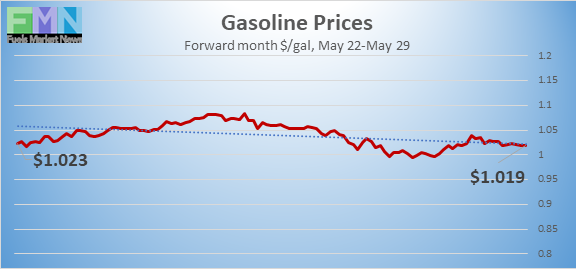

Gasoline Prices

Gasoline prices retreated to open at $0.991/gallon today on the NYMEX, compared with $1.045/gallon on May 22. This was a decline of 5.4 cents (5.2%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April. U.S. average retail prices for gasoline increased by 8.2 cents/gallon during the week ended May 25, averaging $1.960/gallon at the national level. Until this week’s downward correction, gasoline futures prices had risen for four consecutive weeks. Futures contracts are moving to July delivery, where prices are stronger in anticipation of additional economic recovery. Gasoline futures prices are trading in the range of $0.99/gallon to $1.03/gallon. The latest price is $1.016/gallon.

Gasoline prices retreated to open at $0.991/gallon today on the NYMEX, compared with $1.045/gallon on May 22. This was a decline of 5.4 cents (5.2%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April. U.S. average retail prices for gasoline increased by 8.2 cents/gallon during the week ended May 25, averaging $1.960/gallon at the national level. Until this week’s downward correction, gasoline futures prices had risen for four consecutive weeks. Futures contracts are moving to July delivery, where prices are stronger in anticipation of additional economic recovery. Gasoline futures prices are trading in the range of $0.99/gallon to $1.03/gallon. The latest price is $1.016/gallon.

Source: Prices as reported by DTN Instant Market

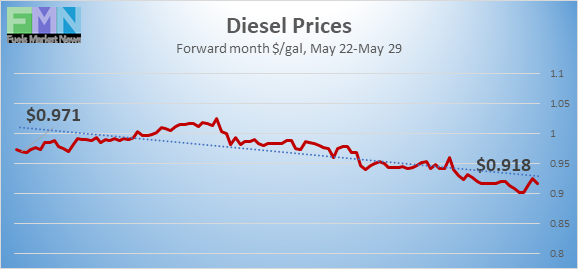

Diesel Prices

Diesel opened on the NYMEX today at $0.9313/gallon, down by 5.6 cents, or 5.7%, from last Friday’s open of $0.9873/gallon. U.S. average retail prices for diesel rose by 0.4 cents/gallon during the week ended May 25 to average $2.390/gallon. Although this was only a fraction of a cent, it was significant because it broke a 19-week downward price trend. Diesel futures prices started the week strong, but the overall market pullback and a large addition to diesel stockpiles drove prices back down on Thursday and Friday. Diesel prices currently are trending down, and it is likely that the week will finish in the red. Currently, diesel is trading in the range of $0.90-$0.94/gallon. The latest price is $0.9215/gallon.

Diesel opened on the NYMEX today at $0.9313/gallon, down by 5.6 cents, or 5.7%, from last Friday’s open of $0.9873/gallon. U.S. average retail prices for diesel rose by 0.4 cents/gallon during the week ended May 25 to average $2.390/gallon. Although this was only a fraction of a cent, it was significant because it broke a 19-week downward price trend. Diesel futures prices started the week strong, but the overall market pullback and a large addition to diesel stockpiles drove prices back down on Thursday and Friday. Diesel prices currently are trending down, and it is likely that the week will finish in the red. Currently, diesel is trading in the range of $0.90-$0.94/gallon. The latest price is $0.9215/gallon.

Source: Prices as reported by DTN Instant Market

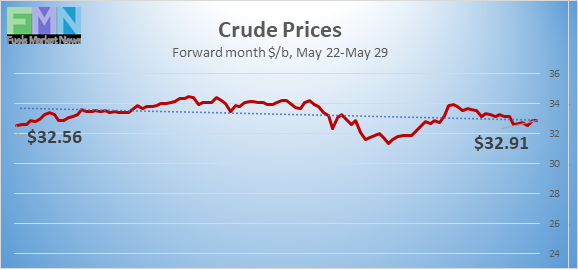

WTI Crude Prices

WTI crude forward prices opened on the NYMEX today at $33.68 a barrel, compared with $33.95 a barrel last Friday. This was a decline of $0.27 a barrel (0.8%.) Although a modest decline, it broke a four-week upward price trend. The week ended April 24, brought a major collapse of $9.64 a barrel (36.5%.) Prices were strengthening as markets looked forward to economic reopening, but sagged upon reports of a large addition to crude inventories. Global markets are in a cautious mood as tensions rise between the U.S. and China concerning China’s moves toward reducing Hong Kong autonomy, in the name of promoting security. Futures crude prices are weakening today, and it is likely that prices will finish in the red. WTI prices are trading in the $32.00-$34.00 a barrel range currently. The latest price is $33.30 a barrel.

WTI crude forward prices opened on the NYMEX today at $33.68 a barrel, compared with $33.95 a barrel last Friday. This was a decline of $0.27 a barrel (0.8%.) Although a modest decline, it broke a four-week upward price trend. The week ended April 24, brought a major collapse of $9.64 a barrel (36.5%.) Prices were strengthening as markets looked forward to economic reopening, but sagged upon reports of a large addition to crude inventories. Global markets are in a cautious mood as tensions rise between the U.S. and China concerning China’s moves toward reducing Hong Kong autonomy, in the name of promoting security. Futures crude prices are weakening today, and it is likely that prices will finish in the red. WTI prices are trading in the $32.00-$34.00 a barrel range currently. The latest price is $33.30 a barrel.

Source: Prices as reported by DTN Instant Market

PRICE MOVERS THIS WEEK: BRIEFING

Oil prices are trailing down today, a downward correction after a four-week period of price recovery. Over the previous four weeks, crude prices had regained around $17 a barrek—essentially doubling in value from approximately $17 a barrel to $34 a barrel. The prospect of a phased lifting of shelter-in-place rules inspired market bulls. Currently, prices are being pressured by increased tension between the U.S. and China, and international markets are opening lower. China is citing national security as the rationale for moving forward with legislative control over Hong Kong. The U.S. immediately opposed the plan, stating that increased Chinese control would eliminate Hong Kong’s special trade status with the U.S.

Today, West Texas Intermediate (WTI) crude prices are hovering around $33 a barrel. U.S. President Donald Trump is scheduled to hold a press conference on China today, and markets are wary that the U.S. may impose sanctions on China. This would further complicate negotiations in the ongoing U.S.-China trade war. Both countries are under considerable stress because of the COVID-19 pandemic, for which President Trump holds China largely responsible. The COVID-19 pandemic has caused such catastrophic damage that it has forced the ongoing U.S.-China trade war to the back pages. This trade war has been ongoing for over two years (since January 2018) and prior to the coronavirus outbreak, positive steps had been taken to reach the U.S.-China Phase One Trade Deal. In March 2020, the U.S. granted exemptions to tariffs on Chinese medical equipment because of the pandemic. Future actions are on hold.

U.S. markets also are shaken by the spread of violent protests over the death of George Floyd while in Minneapolis police custody. The demonstrations cast a pall on the recent optimism over economic reopening. As of the time of this writing, Johns Hopkins University reported that the U.S. five-day moving average in new COVID-19 cases is trending down. These data are cyclical, and it is possible that the moving average will rise based on new infections traced to increased social outings over the Memorial Day weekend. The Johns Hopkins Coronavirus Resource Center reports that global cases have risen to 5,840,369, with 361,066 deaths. Confirmed cases in the U.S. rose to 1,721,926. Deaths attributed to the disease have reached 101,621. This grim total now surpasses the number of U.S. casualties in the Vietnam War and the Korean War combined.

The economic recovery will take time, particularly with unemployment at such staggering levels. U.S. Department of Labor weekly data show 2.123 million initial jobless claims for the week ended May 23rd. There have been nearly 43.2 million unemployment claims over the past ten weeks. In January and February, initial claims averaged 0.212 million per week. In the ten weeks since the week ended March 14, however, the average has catapulted to nearly 4.077 million per week. The number of new weekly claims is heading down, but it remains to be seen how many permanent jobs return, and how quickly.

Oil prices retreated when American Petroleum Institute (API) released information on Wednesday showing another significant crude inventory build, amounting to 8.73 mmbbls. The API also reported additions to inventory of 1.12 mmbbls of gasoline and a large addition of 6.907 mmbbls of diesel. The API’s net inventory build was 16.757 mmbbls. Market analysts had predicted drawdown of approximately 1.6 mmbbls from crude inventories, plus a small drawdown from gasoline inventories and an addition to diesel inventories.

Prices remained weak on Thursday when the U.S. Energy Information Administration (EIA) official statistics reported a sizeable addition of 7.928 mmbbls to crude oil inventories. The EIA also reported an addition to diesel inventories of 5.495 mmbbls. Gasoline stocks were drawn down modestly by 0.724 mmbbls. The EIA net result was an inventory build of 12.699 mmbbls. Crude oil inventories have expanded in 16 of the 20 weeks since the first week of January, sending a total of 107.46 mmbbls of crude oil into storage.

The EIA reports that crude oil in storage at Cushing rose from 35,501 thousand barrels during the week ended January 3, 2020, to 65,446 thousand barrels during the week ended May 1, 2020, an increase of 29,124 thousand barrels, before finally easing to 62,444 mmbbls during the week ended May 8 and 53,462 mmbbls during the week ended May 22. Some surplus crude is being stored in the National Strategic Petroleum Reserve (SPR.) The U.S. government announced plans to take advantage of low prices and support the oil industry by purchasing up to 11.3 mmbbls of sweet crude and up to 18.7 mmbbls of sour crude for the SPR. This is not necessarily domestic crude. The delivery date is between May 1 and June 30. The EIA reports that SPR additions were made in the weeks ended April 24 (1.150 mmbbls), May 1 (1.716 mmbbls), May 8 (1.933 mmbbls,) May 15 (1.882 mmbbls,) and May 22 (2.111 mmbbls.) Current SPR stocks are 643.759 mmbbls.

U.S. crude production continues to decline. The EIA reported that U.S. crude production during the week ended May 22 fell to 11.4 mmbpd, down 0.1 mmbpd from 11.5 mmbpd the prior week. According to the EIA’s weekly data series, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd during the first four weeks of April and 11.6 mmbpd during the first four weeks of May.