Exclusive Analysis by Dr. Nancy Yamaguchi

Oil prices are back on an upward path today, building on gains during the week that brought crude prices back to the $37 a barrel level and now are moving on to $39 a barrel and possibly beyond. Prices surged this morning when data were released showing a significant drop in U.S. unemployment, falling to 13.3% in May after spiking to 14.7% in April. This is allaying fears that the job destruction caused by COVID-19 would continue in May. The phased lifting of shelter-in-place rules is stimulating markets, and the major stock indices are pointing up this morning. The Dow Jones Industrial Average rose above 26,000 this week for the first time in three months. Traders expect a Wall Street rally today.

West Texas Intermediate (WTI) crude prices are hitting the $39 a barrel level and are striving to solidify these gains. Not only was U.S. employment data better than expected but oil prices also strengthened when reports emerged this morning that the OPEC+ group had resolved differences over production cut compliance. A hastily arranged and hastily canceled meeting this week first caused price volatility, but it is now back on for Saturday. Saudi Arabia and Russia were in apparent accord over an extension of oil production cuts, but they could not bring other members into agreement until they threatened to phase out their own cuts. Some countries, including Iraq, Nigeria and Kazakhstan, had not adhered to their production ceilings. Reportedly, assurances have been given about compliance, a new meeting is scheduled for tomorrow and the regular OPEC meeting is scheduled for June 9 and 10. This may reassure markets, but a new twist has emerged that could add to global oil supplies: The long-running civil war in Libya may be at an end, as the U.N.-backed Government of National Accord has captured the capital’s airport and regained full control of Tripoli.

The U.S. Bureau of Labor Statistics this morning released the Employment Situation May 2020 report, also known as the Jobs Report. The COVID-19 pandemic caused unemployment to spike up to 14.7% in April, but as shelter-in-place rules began to be relaxed, the unemployment rate declined to 13.3% in May. U.S. Department of Labor weekly data show 1.877 million initial jobless claims for the week ended May 30. This figure was higher than economists had predicted, but nonetheless it was an improvement. It was the first week since the week of March 13 that claims had receded below two million. There have been approximately 45 million unemployment claims so far this year, more than 42.6 million of them in the 11 weeks since COVID-19 shelter-in-place orders were launched.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have risen to 6,664,908, with 391,686 deaths. Confirmed cases in the U.S. rose to 1,874,411. U.S. deaths attributed to the disease have reached 108,211.

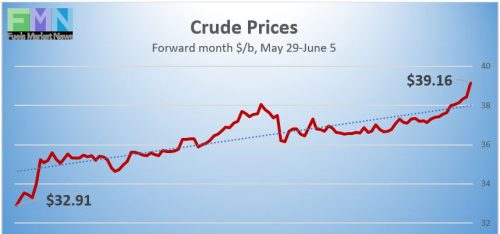

WTI crude futures prices opened at $37.33 a barrel today, an increase of 10.8% from last Friday’s open of $33.68 a barrel. The week is heading for a finish in the black. Our weekly price review covers hourly forward prices from Friday, May 29 through Friday, June 5. Three summary charts are followed by the Price Movers This Week briefing, which provides a more thorough review.

Gasoline Prices

Gasoline prices rose strongly to open at $1.1428 a gallon today on the NYMEX, compared with $1.028 a gallon on May 29. This was a gain of 11.48 cents (11.2%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April. U.S. average retail prices for gasoline rose by 1.4 cents a gallon during the week ended June 1, averaging $1.974a gallon at the national level. Gasoline futures prices are rising today, trading in the range of $1.142 a gallon to $1.21 a gallon. The latest price is $1.2019 a gallon.

Gasoline prices rose strongly to open at $1.1428 a gallon today on the NYMEX, compared with $1.028 a gallon on May 29. This was a gain of 11.48 cents (11.2%.) March brought a crippling collapse of nearly 87 cents per gallon, but prices gradually crept back up in April. U.S. average retail prices for gasoline rose by 1.4 cents a gallon during the week ended June 1, averaging $1.974a gallon at the national level. Gasoline futures prices are rising today, trading in the range of $1.142 a gallon to $1.21 a gallon. The latest price is $1.2019 a gallon.

Source: Prices as reported by DTN Instant Market

Diesel Prices

Diesel opened on the NYMEX today at $1.0716 a gallon, up by 8.69 cents, or 8.8%, from last Friday’s open of $0.9847 a gallon. U.S. average retail prices for diesel fell by 0.4 cents a gallon during the week ended June 1 to average $2.386 a gallon. This gave back the 0.4 cent a gallon gain achieved the prior week. Diesel prices have weakened more or less steadily this year, but they may be on the path to recovery. Diesel futures prices today are rising, and the week is headed for a finish in the black. Currently, diesel is trading in the range of $1.08-$1.15 a gallon. The latest price is $1.1468 a gallon.

Diesel opened on the NYMEX today at $1.0716 a gallon, up by 8.69 cents, or 8.8%, from last Friday’s open of $0.9847 a gallon. U.S. average retail prices for diesel fell by 0.4 cents a gallon during the week ended June 1 to average $2.386 a gallon. This gave back the 0.4 cent a gallon gain achieved the prior week. Diesel prices have weakened more or less steadily this year, but they may be on the path to recovery. Diesel futures prices today are rising, and the week is headed for a finish in the black. Currently, diesel is trading in the range of $1.08-$1.15 a gallon. The latest price is $1.1468 a gallon.

Source: Prices as reported by DTN Instant Market

WTI Crude Prices

WTI crude forward prices opened on the NYMEX today at $37.33 a barrel, compared with $33.68 a barrel last Friday. This was a strong gain of $3.65 a barrel (10.8%.) Last week brought a modest decline, breaking a four-week upward price trend, but prices are back on an upward path. Futures crude prices surged this morning when the U.S. Jobs Report showed an impressive rebound in May. Oil prices are headed for a finish in the black. WTI prices are trading in the $37.00-$39.50 a barrel range currently. The latest price is $39.06 a barrel.

WTI crude forward prices opened on the NYMEX today at $37.33 a barrel, compared with $33.68 a barrel last Friday. This was a strong gain of $3.65 a barrel (10.8%.) Last week brought a modest decline, breaking a four-week upward price trend, but prices are back on an upward path. Futures crude prices surged this morning when the U.S. Jobs Report showed an impressive rebound in May. Oil prices are headed for a finish in the black. WTI prices are trading in the $37.00-$39.50 a barrel range currently. The latest price is $39.06 a barrel.

Source: Prices as reported by DTN Instant Market

PRICE MOVERS THIS WEEK: BRIEFING

Oil prices are back on an upward path today, building on gains during the week that brought crude prices back to the $37 a barrel level. Prices today are moving on to $39 a barrel and possibly beyond. Prices surged this morning when data were released showing a significant drop in U.S. unemployment, falling to 13.3% in May after spiking to 14.7% in April. This is allaying fears that the job destruction caused by COVID-19 would continue in May. The phased lifting of shelter-in-place rules is stimulating markets, and the major stock indices are pointing up this morning. The Dow Jones Industrial Average rose above 26,000 this week for the first time in three months. Traders expect a Wall Street rally today.

Today, West Texas Intermediate (WTI) crude prices are hovering around $39 a barrel and striving to solidify gains. The hastily called and hastily cancelled OPEC+ meeting on Thursday caused price volatility this week, but this morning’s news is that the group is back in accord and will meet tomorrow in advance of the regularly scheduled OPEC meetings June 9 and 10. Saudi Arabia and Russia were pressing for an extension of production cuts, but several OPEC+ countries, including Iraq, Nigeria and Kazakhstan, have a history of exceeding their production ceilings. Saudi Arabia and Russia threatened to phase out their own production cuts unless other members promised to come into compliance, and this pressure appears to be working.

While the OPEC+ group works to reduce global oversupply, a new twist has emerged: The long-running civil war in Libya finally may be at an end. The U.N.-backed Government of National Accord has captured the capital’s airport and regained full control of Tripoli. Libyan output has been crippled by war, falling to a mere 82,000 barrels per day in April, according to OPEC. Libyan output was 1.163 million barrels per day in the fourth quarter of 2019. A rapid return of this supply could undermine the efforts of other OPEC countries.

Some of these international developments have been overlooked this week in the U.S., because of the intense inward focus on domestic turmoil. Protests over the death of George Floyd and the larger issue of racial inequality have occurred or are occurring in all 50 states. As domestic peace returns, it is worth looking outward again, since key events are marching on in the global oil market that will influence U.S. markets.

As of the time of this writing, the Johns Hopkins Coronavirus Resource Center reports that global cases of COVID-19 have risen to 6,664,908, with 391,686 deaths. Confirmed cases in the U.S. rose to 1,874,411. U.S. deaths attributed to the disease have reached 108,211.

The Bureau of Labor Statistics (BLS) this morning released the Employment Situation May 2020 report, also known as the Jobs Report. The COVID-19 pandemic caused unemployment to spike up to 14.7% in April. As shelter-in-place rules began to be relaxed, the unemployment rate declined to 13.3% in May. According to the BLS, “These improvements in the labor market reflected a limited resumption of economic activity that had been curtailed in March and April due to the coronavirus (COVID-19) pandemic and efforts to contain it. In May, employment rose sharply in leisure and hospitality, construction, education and health services, and retail trade. By contrast, employment in government continued to decline sharply.”

U.S. Department of Labor weekly data show 1.877 million initial jobless claims for the week ended May 30. This figure was higher than economists had predicted, but nonetheless was an improvement—it was the first week since the week of March 13 that claims had receded below two million. There have been approximately 45 million unemployment claims so far this year, more than 42.6 million of them in the 11 weeks since COVID-19 shelter-in-place orders were launched.

Oil prices strengthened midweek when American Petroleum Institute (API) released information on Tuesday showing a small drawdown of 0.483 from crude stockpiles. This was more than countered by builds of 1.706 million barrels (mmbbls) of gasoline and 5.917 mmbbls of diesel, but the crude draw appeared to boost confidence. The API’s net inventory build was 7.14 mmbbls. Market analysts had predicted across-the-board additions totaling approximately 6.2 mmbbls of crude plus products.

Prices received reinforcement on Wednesday when U.S. Energy Information Administration (EIA) official statistics reported a larger drawdown of 2.077 mmbbls from crude oil inventories. Prices remained strong, even though the impact of this was more than counteracted by significant additions of 2.795 mmbbls to gasoline inventories and 9.934 mmbbls to diesel inventories. The EIA net result was another sizeable inventory build amounting to 10.652 mmbbls. Crude oil inventories have expanded in 16 of the 21 weeks since the first week of January, sending a total of 105.38 mmbbls of crude oil into storage.

During the worst of the oversupply, the EIA reported that crude oil in storage at Cushing rose from 35,501 thousand barrels during the week ended January 3, 2020, to 65,446 thousand barrels during the week ended May 1, 2020, an increase of 29,124 thousand barrels. Cushing stocks began to subside over the next four weeks of May, falling to 51,723 mmbbls during the week ended May 29. Some surplus crude is being stored in the National Strategic Petroleum Reserve (SPR.) The U.S. government announced plans to take advantage of low prices and support the oil industry by purchasing up to 11.3 mmbbls of sweet crude and up to 18.7 mmbbls of sour crude for the SPR. This is not necessarily domestic crude. The delivery date is between May 1 and June 30. The EIA reports that SPR additions were made in the weeks ended April 24 (1.150 mmbbls), May 1 (1.716 mmbbls), May 8 (1.933 mmbbls,) May 15 (1.882 mmbbls,) May 22 (2.111 mmbbls) and May 29 (4.02 mmbbls). Current SPR stocks are 647.779 mmbbls.

U.S. crude production continues to decline. The EIA reported that U.S. crude production during the week ended May 29 fell to 11.2 mmbpd, down 0.2 mmbpd from 11.4 mmbpd the prior week. According to the EIA’s weekly data series, U.S. crude production averaged 13.025 mmbpd in February, the highest total ever. Production fell to 12.25 mmbpd in April and 11.52 mmbpd in May.