MARKET SNAPSHOT

Friday, June 28, 2019

By Dr. Nancy Yamaguchi

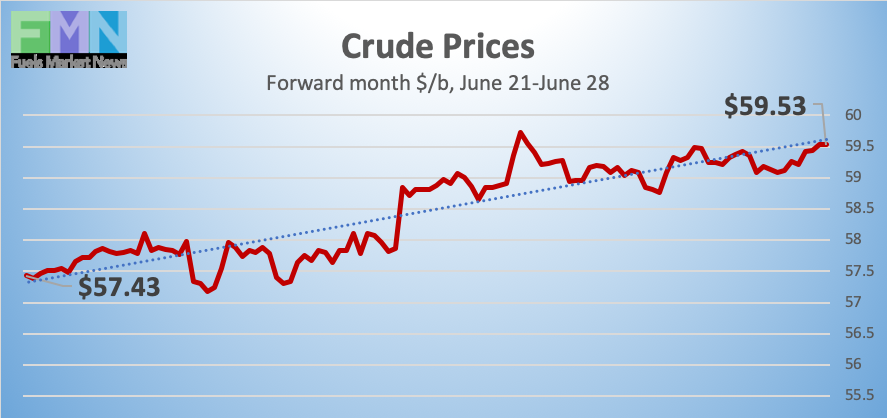

Oil prices continued to climb this week for the second week in a row, as geopolitical forces, global economics, and supply-demand factors worked together to stimulate prices. U.S. production declined, and oil inventories fell sharply. World leaders are in Japan today for the G20 meeting, which will include a meeting between the U.S. and China. OPEC will meet after the weekend, and the group is expected to extend the production cut agreement. The Philadelphia Energy Solutions (PES) refinery is now headed for closure, after the owners decided not to repair the fire- and explosion-ravaged facility. WTI crude prices opened this morning $5.08/b (9.7%) above last Friday’s level. Crude prices have reclaimed the territory above $59/b. Our weekly price review covers hourly forward prices from 9AM EST Friday June 21st through 9AM EST Friday June 28th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

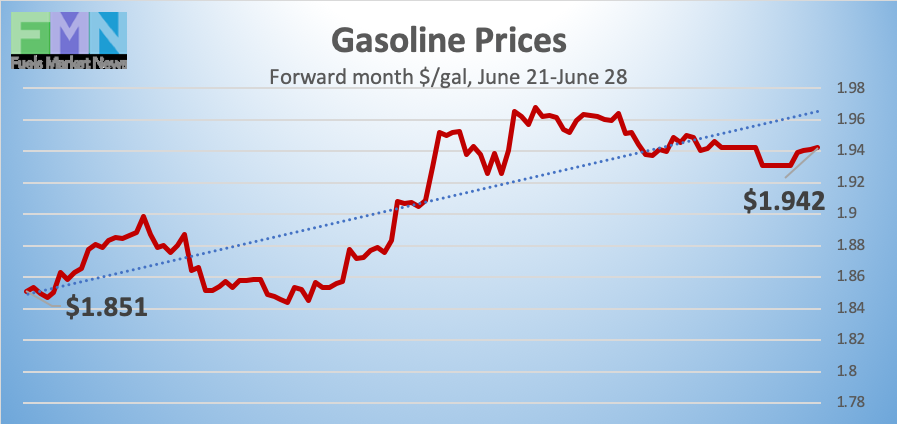

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.7887/gallon on Friday June 21st, and prices surged to an open of $1.946/gallon on Friday June 28th, a significant increase of 15.73 cents (8.8%.) Until the past two weeks, gasoline forward prices been on a downward trend, shedding nearly 35 cents/gallon. Gasoline prices had been at their lowest levels since February. The devastating explosion and fire at the PES refinery in Philadelphia started a gasoline price rally that stacked atop the already strengthening crude prices. PES announced this week that it would not rebuild the refinery. Gasoline trades are occurring mainly in the range of $1.93-$1.94/gallon. The latest price is $1.9378/gallon. Today is the last day for July forward contracts.

DIESEL PRICES

Diesel opened on the NYMEX at $1.8942/gallon on Friday June 21st and opened on Friday June 28th at $1.9497/gallon, a significant weekly increase of 5.55 cents (2.9%.) Diesel prices have surged with the renewed combativeness between the U.S. and Iran and the generally tighter outlook for supply-demand balance. The past two weeks brought a price rally that restored 14.1 cents/gallon to diesel prices, recouping a portion of the prior four week’s downward spiral that slashed diesel forward prices by 31.81 cents/gallon. Diesel contracts currently are trading in the $1.94-$1.96/gallon range. The latest price is $1.9534/gallon. Today is the last day for July forward contracts.

WEST TEXAS INTERMEDIATE PRICES

PRICE MOVERS THIS WEEK : BRIEFING

Oil prices are in their second rallying week, potentially heading back to the $60/b mark. WTI crude prices jumped by nearly $2/b this week, building upon the $5/b surge seen last week prompted by the downing of a U.S. drone by Iran and an ordered-then-cancelled military response by U.S. President Trump. The President this week placed additional sanctions on Iran’s leader, Ayatollah Ali-Khameini, though the move was not seen as having a major impact on Iran’s already struggling economy. Iran responded that any diplomatic path was permanently closed. The $7/b oil price surge of the past two weeks has gone far to erase the price slump of the previous four weeks, which slashed $10.94/barrel from WTI prices.

Prices were also propelled upward by tightening supply. The U.S. Energy Information Administration (EIA) reported that U.S. crude oil production fell to 12.1 million barrels per day (mmbpd) during the week ended June 21st. This was down from the record-high 12.4 mmbpd reported for the week ended May 31st. The Dallas Fed reported that the January-April period brought an estimated decline of 3650 jobs in Texas support activities for mining (mostly oilfield service.) The decline may be temporary, given the strong increase in oil prices over the past two weeks. Pipeline expansions are scheduled for completion in the second half of 2019, which is expected to bring a recovery in output and employment.

The week also brought a massive drawdown from oil inventories. On Tuesday, the American Petroleum Institute (API) reported a drawdown of 7.6 million barrels (mmbbls) from crude oil inventories plus a draw of 3.2 mmbbls from gasoline inventories. Diesel inventories rose slightly by 0.2 mmbbls. Official statistics were more bullish. EIA reported across-the board inventory drawdowns of 12.788 mmbbls of crude oil, 0.996 mmbbls of gasoline, and 2.441-mmbbls from diesel inventories. The net drawdown was 16.225 mmbbls. Much of the drawdown stemmed from a sharp drop in U.S. crude imports coupled with an increase in crude exports. Refinery input increased only modestly.

The world is focused on international markets today, as the G20 meetings begin in Japan. Tomorrow, President Donald Trump will meet with China’s Head of State Xi Jinping. Asian stock markets have been cautious so far, recognizing that the two countries remain far apart on key trade issues.

OPEC will be meeting in Vienna on July 1-2, and the group will by then have some results from the G20 meeting. An extension of the current production cut agreement is factored into the market. A deeper cut, however, would likely cause prices to jump into a new, higher bandwidth.

In the U.S., a catastrophic explosion and fire at the Philadelphia Energy Solutions (PES) refinery is now expected to create permanent change in the area’s fuel production and delivery. The company, which had struggled to turn the refinery around, decided to close the facility. The PES refinery had a nameplate capacity of 335,000 bpd, with a full range of gasoline-maximizing technologies: catalytic cracking, alkylation, catalytic reforming, isomerization, aromatics, and desulfurization. The EIA earlier had reported that U.S. crude distillation capacity as of January 1st hit a 38-year high of 18.8 mmbpd.