From The Desk Of The Publisher

We’ve listened to input by our readers and are making a few changes to our format. First, we’re changing from a daily fuels analysis to a more in-depth and nuanced weekly publishing schedule. We will still offer the exclusive analysis of the entire downstream fuel industry by Dr. Nancy Yamaguchi that you’ve come to trust and as you can see, we’ve actually expanded the analysis.

If you would like to subscribe to our free Friday newsletter, please click here!

Sincerely,

Gary Bevers, Publisher

MARKET SNAPSHOT

Oil prices sagged this week under the weight of ample supplies, though markets may strengthen this morning based on just-released data showing unexpectedly strong employment growth. WTI crude prices this morning were $3.50/b below last Friday’s level. Last week’s news that the U.S. would end waivers on Iranian crude purchases set off a price surge, with WTI crude hitting highs above $66.50/b. The surge was quelled by rising inventories, a new record-high U.S. crude production number, and plans among OPEC and partners to raise output. Our weekly price review covers hourly forward prices from 9AM EST Friday April 29th through 9AM EST Friday May 3rd. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

GASOLINE PRICES

Gasoline opened on the NYMEX at $2.1298/gallon on Friday April 26th and opened on Friday May 3rd at $2.0116, down by 8.59 cents (4.1%.) Last Tuesday April 23rd brought the highest opening price ($2.1389/gallon) since July 2nd, 2018. The price runup ended, as U.S. supplies showed an unexpected increase. Gasoline forward prices currently are recovering after a downward correction, with trades occurring mainly in the range of $2.01-$2.03/gallon. The latest price is $2.0270/gallon.

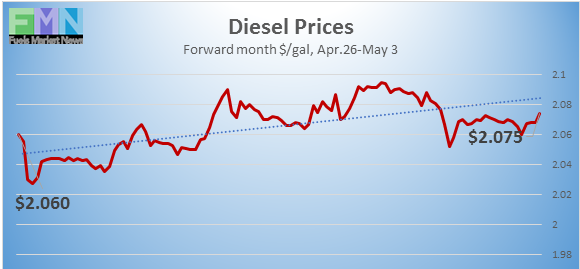

DIESEL PRICES

Diesel opened on the NYMEX at $2.0947/gallon on Friday April 26th and opened on Friday May 3rd at $2.0675, down by 2.72 cents (1.3%.) Last week’s price surge brought a peak opening price on Wednesday of $2.1125/gallon, the highest price since December 24th, 2014. As crude prices ebbed, diesel prices followed. Diesel prices currently are creeping back up after a downturn today, trading mainly in the $2.06-$2.08/gallon range. The latest price is $2.0759/gallon.

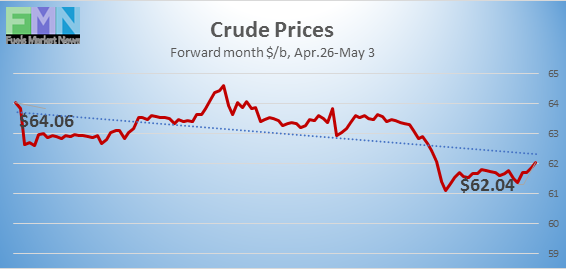

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX at $65.13/barrel on Friday April 26th and opened on Friday May 3rd at $61.55/barrel, down by $3.58/b (5.5%.) Last Wednesday’s market opening brought a price peak of $66.17/b, the highest price since October 24th. Prices surged upon news that the U.S. would not extend waivers on purchases of Iranian crude. Yet supplies quickly were deemed sufficient, and prices retreated below $62/b. Prices currently are stabilizing, and they may creep back up above $62/b based on strong employment data. WTI is trading mainly in the range of $61.50/b-$62.25/b. The latest price is $61.74/b.

PRICE MOVERS THIS WEEK : BRIEFING

Prices were in retreat this week, as markets appeared more than ready to cope with the end of waivers on purchases of Iranian crude. Six-month waivers had been granted to China, India, Taiwan, Japan, South Korea, Italy, Greece, and Turkey. Apparently, there had been some hope among these importers that waivers might be extended, since the White House had been slow to make an unequivocal announcement. Turkey stated that it could not find substitute sources of oil “quickly.” India asked if the U.S. would be flexible in allowing some imports to continue. China reportedly has quantities of Iranian crude in port, stuck in customs. Iranian crude exports are likely to continue at 400,000-500,000 bpd despite U.S. actions.

Prices weakened further midweek when the American Petroleum Institute (API) reported that U.S. crude oil inventories rose by 6.8 million barrels (mmbbls.) This was partly offset by drawdowns of 1.1 mmbbls from gasoline inventories and 2.1 mmbbls from diesel inventories. The API net addition to inventories was 3.6 mmbbls. The API report was followed by a more bearish set of official statistics from U.S. Energy Information Administration (EIA.) The EIA reported an addition of 9.934 mmbbls to crude oil inventories, plus an addition of 0.917 mmbbls to gasoline inventories and a 1.307-mmbbls drawdown from diesel inventories. The net addition to oil inventories was a hefty 9.544 mmbbls.

The EIA also reported that U.S. crude production hit a new record-high of 12.3 million bpd during the week ended April 26th. Based on these preliminary production numbers, U.S. oil production has climbed by 600,000 bpd so far in 2019, and output is forecast to continue to grow.

Countering the downward pressure on oil prices, markets may strengthen today, based on just-released data from the Bureau of Labor Statistics (BLS.) The BLS Jobs Report showed that non-farm employment rose by an unexpectedly strong 263,000 jobs in April, and the unemployment rate shrank to just 3.6%. According to the BLS, “Notable job gains occurred in professional and business services, construction, health care, and social assistance.”