MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

October 18, 2019: Crude prices rose in early morning trades, largely in response to market optimism surrounding strong earnings reports in the U.S., a Brexit deal, and a pause in the Turkish advance into Syria. Prices fell midweek, based on increased supply, rising inventories, and additional cuts in forecast global economic growth. WTI futures crude prices opened on Friday, October 11 at $53.88/b, and prices rose to an open of $54.09/b today. Currently, the upward trend in prices is flattening, though WTI is holding above $54/b. The week may be heading for a finish in the black. Our weekly price review covers hourly forward prices from Friday, October 11 through Friday, October 18. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

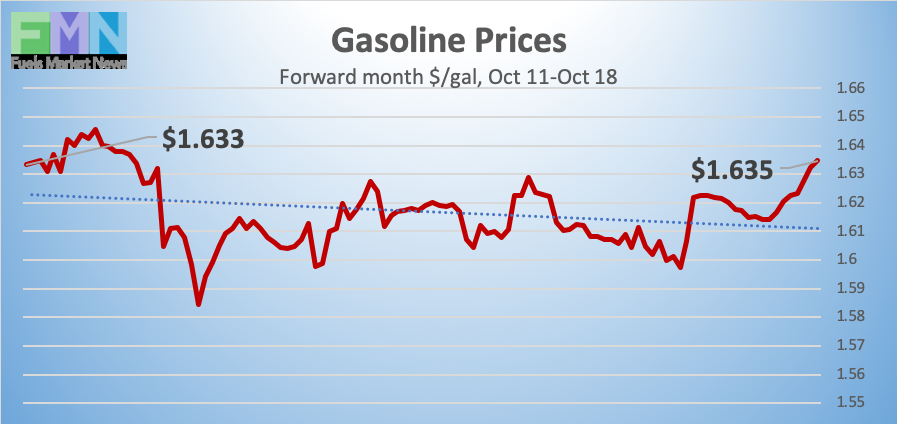

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.6202/gallon on Friday, October 11, and prices opened at $1.622/gallon on Friday, October 18. This was a slight increase of 0.18 cents (0.1%,) holding steady after last week’s recovery of 7.25 cents. U.S. average retail prices fell by 1.6 cents/gallon during the week ended October 14th. Futures prices for gasoline rose this morning, but the upward momentum is now faltering. If the week finishes in the black, the gains may be small. Trades are occurring mainly in the range of $1.61-$1.64/gallon. The latest price is $1.6276/gallon.

DIESEL PRICES

Diesel opened on the NYMEX at $1.9344/gallon on Friday, October 11 and opened on Friday, October 18 at $1.9534/gallon, up by 1.9 cents (1.0%.) This builds upon last week’s bounce-back of 5.83 cents. Diesel forward prices had surged in the aftermath of the attacks on Saudi oil facilities, dropped as production capacity was restored, then surged again after news of the attack on an Iranian-owned oil tanker. Diesel prices rose in early morning trades and are stabilizing currently. The week appears to be heading for a finish in the black. Contracts currently are trading in the $1.94-$1.96/gallon range. The latest price is $1.9542/gallon.

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday, October 11 at $53.88/barrel and rose to an open of $54.09/barrel on Friday, October 18, a modest increase of $0.21/b (0.4%.) Prices climbed in early morning trades, but the upward momentum is currently flattening. WTI prices are maintaining the $54/b level, and the week may be heading for a finish in the black if prices hold. WTI crude is trading mainly in the range of $53.75/b-$54.75/b. The latest price is $54.24/b.

PRICE MOVERS THIS WEEK : BRIEFING

It was an eventful week both nationally and internationally, but events worked at cross purposes with respect to oil prices, and the week may end up with little change. Prices were pulled down by rising inventories, high production, U.S.-China stress, and forecasts of slowing economic growth. Oil prices were supported by geopolitical concerns, strong corporate earnings in the U.S., and a Brexit deal between the UK and the European Union. Geopolitical concerns have been elevated by the attack on an Iranian oil tanker in the Red Sea, and the Turkish invasion of northern Syria. Yesterday, Turkey agreed to a five-day pause to allow Kurdish forces to withdraw from a “safe zone.” Occupying this zone was a key objective of the Turkish invasion, and the withdrawal of U.S. and Kurdish forces will make it possible. While the U.S. is hopeful that this will be a cease fire, Turkey has agreed only to a “pause.”

U.S.-China trade talks made little progress, and relations may be strained by protests in Hong Kong. China has threatened retaliation if the U.S. backs pro-democracy protesters in Hong Kong. The trade war is taking a toll on both countries. China’s economic growth reportedly slowed to 6.0% year-on-year in the third quarter, following growth of 6.2% in the second quarter. This was the slowest rate of growth since the early 1990s.

The International Monetary Fund (IMF) cut for the fifth time its forecast of global growth. The current IMF World Economic Outlook now foresees global growth of 3.0% in 2019. Last year, the IMF had forecast global growth of 3.9% in 2019.

U.S. stocks climbed based on strong earnings reports in the U.S. The Dow Jones Industrial Average is back above 27,000. International markets regained optimism when at long last a new Brexit deal was reached between the U.K. and the European Union. While the EU endorsed it, it still needs approval by the UK Parliament, where it faces a difficult battle.

Fuel prices sagged midweek when the American Petroleum Institute (API) reported a massive addition of 10.5 million barrels (mmbbls) to U.S. crude stockpiles. The API reported a drawdown of 0.934 mmbbls from gasoline inventories plus 2.9 mmbbls from diesel inventories. The API’s net inventory build was 6.666 mmbbls.

The EIA released official statistics on Thursday, (data was delayed one day because of Columbus Day,) agreeing with the pattern of crude build and product draw, but with a smaller crude build and more significant product draws. The EIA reported a major addition of 9.281 mmbbls to crude inventories, partially offset by drawdowns of 2.562 mmbbls of gasoline and 3.823 mmbbls of diesel. The net result was an inventory build of 2.229 mmbbls.