MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

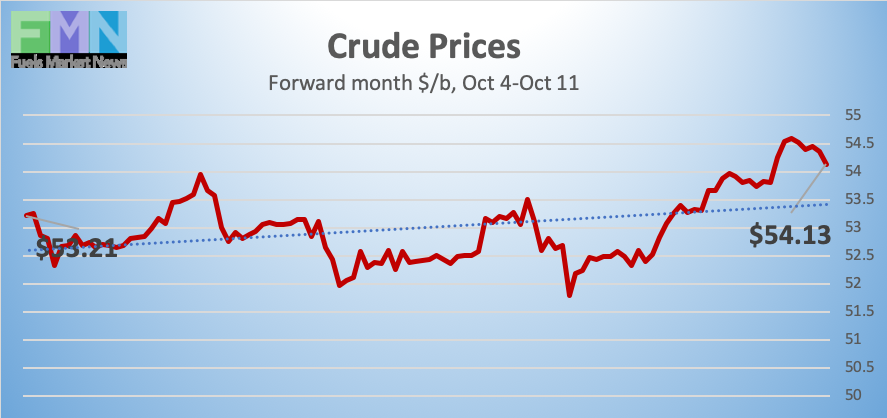

October 11, 2019: Crude prices rose this morning in response to an attack on an Iranian tanker off Jeddah today. Prices already had been recovering this week, climbing by approximately $1.60/b after the prior two weeks of decline. WTI futures crude prices opened on Friday October 4th at $52.29/b, and prices rose to an open of $53.88/b today. The attack caused prices to rise, with WTI prices hitting highs above $54.50/b in early trading. Prices are easing once again, with markets possibly undervaluing geopolitical risk. The overall trend is up, however, and the week appears to be heading for a finish in the black. Our weekly price review covers hourly forward prices from Friday October 4th through Friday October 11th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.5477/gallon on Friday, October 4, and prices opened at $1.6202/gallon on Friday, October 11. This was a significant recovery of 7.25 cents (4.7%) after the prior week’s collapse of 10.98 cents. U.S. average retail prices edged back up only slightly, by 0.3 cents/gallon, during the week ended October 7th. Futures prices for gasoline are rising this morning, and the week appears to be heading for a finish in the black. Trades are occurring mainly in the range of $1.62-$1.65/gallon. The latest price is $1.6388/gallon.

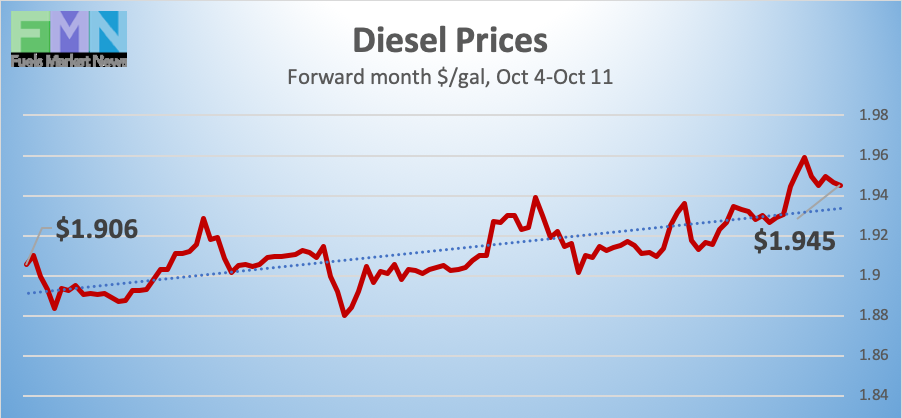

DIESEL PRICES

Diesel opened on the NYMEX at $1.8761/gallon on Friday, October 4, and opened on Friday, October 11, at $1.9344/gallon, a rebound of 5.83 cents (3.1%) after last week’s drop of 8.02 cents. Diesel forward prices had fallen by 13.68 cents over the past two weeks, normalizing after the price runup caused by the attacks on Saudi oil facilities. Prices this morning spiked alongside crude prices, after news of the attack on an Iranian-owned oil tanker near Jeddah. Yet crude prices trended back down. Diesel prices gave back only a portion of the gain, however, and the week appears to be heading for a finish in the black. Contracts currently are trading in the $1.93-$1.97/gallon range. The latest price is $1.9571/gallon.

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday, October 4, at $52.29/barrel and rose to an open of $53.88/barrel on Friday, October 11, a recovery of $1.59/b (3.0%.) This morning, prices rose on the news of an attack on an Iranian-owned tanker near Jeddah. WTI prices hit highs above $54.50/b. But the price runup hit a peak, and prices then slid back essentially to their starting point. WTI prices are hovering around $54/b, and the week appears to be heading for a finish in the black. This week’s price recovery follows two weeks of decline. WTI crude is trading mainly in the range of $53.75/b-$54.75/b. The latest price is $54.17/b.

PRICE MOVERS THIS WEEK : BRIEFING

This morning’s attack on an Iranian-owned oil tanker caused a surge in oil prices, though some price gains were handed back within a few hours. The tanker was identified as the Suezmax Sabiti, reportedly struck by two missiles in the hull, suffering a fire, and leaking crude oil around 60 miles from Jeddah on the Red Sea.

Geopolitical concerns already had been elevated by the Turkish invasion of northern Syria, though the price impact had been muted by market oversupply. Turkey invaded northern Syria just days after the U.S. withdrew troops. The U.S. now reportedly will attempt to broker a cease fire. Oil prices did not spike, indicating that traders considered the market well-supplied. Geopolitical risks did not have the impact that otherwise they might have had. The attack on the Sabiti changed that today, but it is not clear whether the price increase will stick.

At least some level of geopolitical risk is considered the norm, and price impacts may be short-term. Most oil price forecasts foresee little upward movement this year. The Energy Information Administration (EIA) released its latest Short-Term Energy Outlook, cutting once again its forecast of oil prices. The EIA now forecasts a price of $57/b for West Texas Intermediate (WTI) crude in the second quarter of 2020. Previous forecasts were based on $62/b WTI.

The resumption of U.S.-China trade talks is causing on-again off-again market optimism. The trade war is viewed as a key factor slowing global demand growth. OPEC has reduced its forecast of oil demand for 2019, and the group announced that “all options are open” in terms of deepening production cuts in 2020. In the meantime, Nigeria was granted a higher production allowance of 1.774 million barrels per day (mmbpd,) versus 1.685 mmbpd. Initially, Nigeria was granted an exemption from participating in the cuts because of chronic internal unrest and attacks on oil infrastructure. However, Nigerian output has risen, and OPEC reported it at 1.866 mmbpd in August. Nigeria made the case that OPEC had not factored in new output from the Egina ultra deepwater field, and that its production ceiling should be raised. The field started producing this year, and it is expected to produce 200,000 bpd at its peak.

Fuel prices strengthened on Tuesday when the American Petroleum Institute (API) reported significant drawdowns from gasoline and diesel inventories, 5.9 million barrels (mmbbls) and 4.0 mmbbls respectively. These inventory deletions more than offset a 4.1-mmbbl addition to crude inventories. The API’s net inventory draw was 5.8 mmbbls.

The EIA released official statistics on Wednesday, agreeing with the pattern of crude build and product draw, but with lesser volumes. The EIA reported an addition of 2.927 mmbbls to crude inventories, more than offset by drawdowns of 1.213 mmbbls of gasoline and 3.943 mmbbls of diesel. The net result was an inventory draw of 2.229 mmbbls.

The EIA also reported that during the week ended October 4th, U.S. crude oil production hit a new record of 12.6 million barrels per day (mmbpd.) Baker Hughes reported on Friday that the U.S. active oil and gas rig count fell by 5 during the week ended October 4th. This was the seventh consecutive week that the rig count has fallen.