MARKET SNAPSHOT

By Dr. Nancy Yamaguchi

January 24, 2020: Oil prices continued to fall this week, with lows dipping to levels not seen frequently since October. Prices have been tamped down by the outbreak of the SARS-like coronavirus in China, which already has taken 25 lives. Today, China widened travel restrictions to 40 million people. As of this morning, the situation has not been declared a global emergency, though fuel prices are expected to weaken because of drops in demand. Even a full shut-in of Libyan crude exports failed to bolster prices this week. There are two large-scale political matters in the news this week: President Donald Trump’s impeachment hearing in the U.S. Senate, and the 50th World Economic Forum (WEF) meeting at Davos, Switzerland. So far, these events are having a mild depressing impact on fuels markets. Crude prices are a far cry from the $65/b heights hit during the week of uncertainty when the world wondered whether the U.S.-Iran conflict would escalate. WTI crude futures prices are below $55/b this morning. Prices currently are in the $54.50-$55.75/b range. The week appears to be headed for a finish in the red.

WTI futures crude prices opened on Friday, January 17, at $58.59/b, and prices slid to an open of $55.69/b today, down by $2.90/b. WTI futures prices dipped below $55/b midweek, and they are falling below $55/b today. Gasoline and diesel prices also weakened noticeably, following crude down, and dipping to midweek API data showing a significant addition to stockpiles. Our weekly price review covers hourly forward prices from Friday, January 17th, through Friday, January 24th. Three summary charts are followed by the Price Movers This Week briefing for a more thorough review.

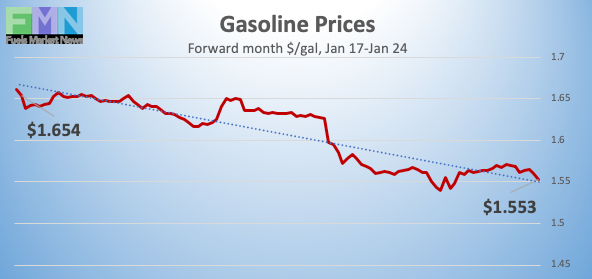

GASOLINE PRICES

Gasoline opened on the NYMEX at $1.6644/gallon on Friday, January 17, and prices slid to open at $1.5636/gallon on Friday, January 24. This was a drop of 10.08 cents (6.1%.) Gasoline futures prices ranged this week from a low of $1.5346/gallon on Thursday to a high of $1.6711/gallon on Tuesday, a large range of 13.65 cents. U.S. average retail prices fell by 3.3 cents/gallon during the week ended January 20th. Gasoline prices currently are trending down. Trades are occurring mainly in the range of $1.53-$1.57/gallon. The latest price is $1.5350/gallon.

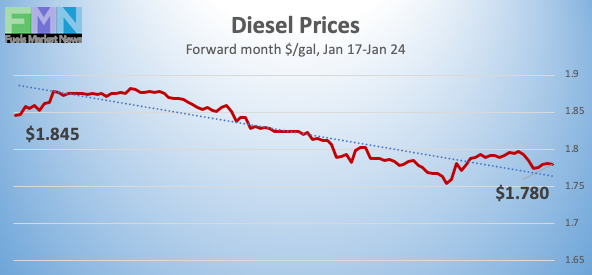

DIESEL PRICES

Diesel opened on the NYMEX at $1.8618/gallon on Friday, January 17, and opened on Friday, January 24, at $1.7933/gallon, down significantly by 6.85 cents (3.7%.) U.S. average retail prices for diesel fell by 2.7 cents/gallon during the week ended January 20th. Diesel futures prices spanned a wide range this week, ranging from a high of $1.8859/gallon on Tuesday to a low of $1.7506/gallon on Thursday, a range of 13.53 cents. The week is heading for a finish in the red—the fourth downward weekly movement in a row. Prices are currently trending down, with contracts trading in the $1.76-$1.79/gallon range. The latest price is $1.7647/gallon.

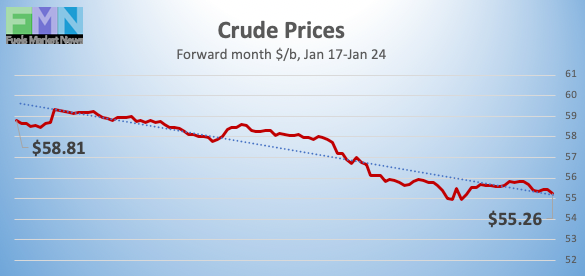

WEST TEXAS INTERMEDIATE PRICES

WTI (West Texas Intermediate) crude forward prices opened on the NYMEX on Friday, January 17, at $58.59/b. Prices opened at $55.69/b today, a drop of $2.90 (4.9%.) WTI futures prices ranged from a high of $59.77/b on Tuesday to a low of $54.77/b on Thursday, a range of $5.00/b. The full range of daily prices was not reported on Monday in observance of Martin Luther King Day. Prices fell Wednesday, Thursday and Friday this week. The low point of $54.77/b was the lowest price since November 1st. During the week, oil markets were pressured by the coronavirus outbreak in China, additions to oil inventories, and political disarray on the U.S. and abroad. The week is heading for a finish in the red. WTI futures prices currently are trading mainly in the range of $54.50-$55.50/b. The latest price is $54.66/b.

PRICE MOVERS THIS WEEK : BRIEFING

Oil prices continued to retreat this week, falling to lows not seen regularly since October. WTI crude prices have been dipping below $54.50/b this morning and could potentially drop below $54/b. The breakout of a coronavirus in China has essentially quarantined the city of Wuhan, the center of the outbreak. A coronavirus can attack birds and mammals, and if one crosses from animal to human, it can then be transmitted from human to human. The SARS (Severe Acute Respiratory Syndrome) outbreak in 2003 was a coronavirus, which infected over 8000 people and had a 10% fatality rate. The travel ban is cutting into traditional Lunar New Year holiday travel in China. It will discourage travel to China and within Asia, reducing oil demand and widening the supply-demand gap.

The coronavirus situation has not been labeled a global emergency. However, comparisons already are being made to the SARS outbreak, which caused a drop in crude prices. For example, Brent crude spot prices averaged $32.77/b in February 2003, and prices dropped to an average of $25/b in April 2003. This was the month that the World Health Organization issued a global health alert about SARS. Chinese officials are taking a much swifter and stricter approach to this coronavirus, hoping to stave off the spread of contagion.

There are two large-scale political matters in the news this week: President Donald Trump’s impeachment hearing in the U.S. Senate, and the 50th World Economic Forum (WEF) meeting at Davos, Switzerland. There may be a depressing impact on fuels markets: In the United States, party-line divisiveness makes the U.S. less effective in coping with any long-term issues, and in the global financial markets, there are few bright spots capable of strengthening economic growth. Concern over climate change is rising, and it will be a key topic at Davos today. Australia continues to reel from deadly, devastating, bushfires. Smoke from the fires has traveled over 6800 miles already and has reached South America. The environmental toll is shocking.

Geopolitical risk factors appear to have faded from market mentality. Even a full shut-in of Libyan crude exports failed to bolster prices this week.

Oil prices already were flagging when the American Petroleum Institute (API) reported across-the-board additions to U.S. oil inventories: 1.6-million barrels (mmbbls) of crude oil, 4.5 mmbbls of gasoline, and 3.5 mmbbls of diesel. Industry experts had anticipated a modest crude stock drawdown more than counterbalanced by drawdowns from gasoline and diesel stockpiles. The API’s net inventory build was a significant 9.6 mmbbls.

The U.S. Energy Information Administration (EIA) released a much less bearish set of official statistics: a small drawdown from crude stocks of 0.405 mmbbls, and addition of 1.745 mmbbls to gasoline stockpiles, and a drawdown from distillate stockpiles of 1.185 mmbbls. The official data came as a relief after the past weeks of major inventory additions. The EIA net result was a minor inventory build of 0.155 mmbbls.

The EIA also reported that U.S. crude production remained at its new record-high:13.0 mmbpd during the week ended January 17th. Approximately 1.2 mmbpd was added to U.S. crude oil output in 2019.